Sometimes, government regulations can work in a company’s favor

Heavy regulation is often associated with inefficiency, limited profits, and less attractive industries. Sometimes, government regulation has the opposite effect.

Today’s firm has phenomenal returns thanks to government regulation, not in spite of it.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Tuesday Tearsheets

Powered by Valens Research

When investors think of heavily regulated industries, mostly bad pictures come to mind. The utilities industry for example is plagued with complicated levels of regulation, which has led to earnings caps and limited interest from investors.

Without these regulations, utilities would have geographic monopolies and could potentially charge whatever they wanted. There’s a reason to have some regulations in place, but investors typically see it as a negative for related stocks.

There are examples, though, of companies who benefit from government regulation.

Credit rating agencies are a great example. Much like every American has a personal credit score, the SEC mandates that companies maintain a corporate credit rating. These ratings are used to price debt and often help investors better evaluate companies.

This government requirement helps the credit rating agencies make massive returns.

To dive deeper into this example, we will take a look at Moody’s Corporation (MCO). Moody’s is one of the “Big 3” rating agencies, and its returns are often misunderstood.

In this case, regulation should mean Moody’s is able to mint cash. That said, its as-reported returns make it look like regulation is hurting its business.

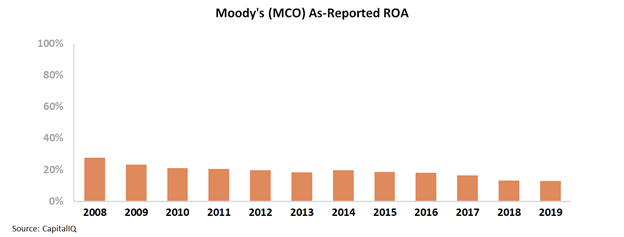

Moody’s as-reported ROA levels have slowly declined since the Great Recession in 2008. Specifically, ROA has faded from 28% levels in 2008 to 13% in 2019.

By looking at as-reported metrics, investors might assume that since the Great Recession, the rating agencies have struggled to maintain their economic moat.

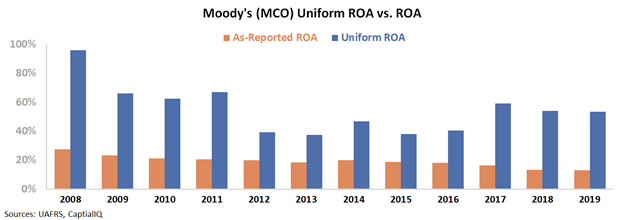

In reality, this is not an accurate picture of Moody’s performance. The firm is able to generate returns much higher than what is shown.

When looking through a Uniform Accounting lens, it becomes clear that the firm’s business is better than it seems.

Despite Uniform ROA declining from 96% levels in 2008 to 38% levels in 2015, it recovered to 54% levels in 2019. Using Uniform Accounting, investors can conclude that Moody’s has been able to generate returns of at least 2.5x its required rate of return.

As you can see, Moody’s Uniform ROA levels are trending better than as-reported metrics, which portrays how easily as-reported metrics can misrepresent reality.

When viewing the company using Uniform data, investors can see that the regulatory environment still works in Moody’s favor.

Without Uniform Accounting, investors may get the wrong idea about government regulation.

Before any investor can develop a thesis of how to beat the market, they have to know the underlying performance of the companies they are studying. Using as-reported accounting would be no better than guesswork.

SUMMARY and Moody’s Corporation Tearsheet

As the Uniform Accounting tearsheet for Moody’s Corporation (MCO:USA) highlights, the Uniform P/E trades at 25.1x, which is around the global corporate average of 25.2x, but above its own historical average of 21.7x.

Average P/Es require average EPS growth to sustain them. That said, in the case of Moody’s, the company has recently shown a 12% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Moody’s Wall Street analyst-driven forecast is a 23% and 10% EPS growth in 2020 and 2021, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Moody’s $280 stock price. These are often referred to as market embedded expectations.

The company needs to have Uniform earnings grow by 8% per year over the next three years in order to justify current stock prices. What Wall Street analysts expect for Moody’s earnings growth is above what the current stock market valuation requires in 2020 and 2021.

Furthermore, the company’s earning power is 9x the long-run corporate average. Also, intrinsic credit risk is 60bps above the risk-free rate and cash flows and cash on hand are 3x of its total obligations—including debt maturities, capex maintenance, and dividends. All in all, this signals a low credit and dividend risk.

To conclude, Moody’s Uniform earnings growth is above its peer averages, but the company is trading below its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research