Memory shortages are a boon for this data storage firm

The AI boom is causing data storage shortages. As a result, prices have skyrocketed and has enabled storage manufacturers to recover from the brutal boom-and-bust cycle they experienced in 2020 to 2023.

With storage demand up and prices soaring, Seagate (STX) has become a beneficiary of this industry-wide tailwind.

After seeing its revenues decline from 2022 to 2024, the company enjoyed a swift recovery on the top and bottom line over the past year thanks to the latest AI bottleneck.

Most recently, Seagate’s strong second quarter earnings emphasized the company’s growth opportunity, and its potential for lasting momentum.

Investor Essentials Daily:

Friday News-based Update

Powered by Valens Research

The data storage market has dealt with its fair share of whiplash over the past five years.

In 2020, factory shutdowns brought the semiconductor sector to its knees, delaying shipments by several months. This led to a chip shortage which cascaded into a full-blown cycle of panic buying, as companies wanted to secure their own supply.

Amid growing demand, chipmakers expanded their capacity to meet all this demand. And by 2021, semiconductor sales reached a record $556 billion.

Unfortunately, this surge in sales didn’t last as higher interest rates and inflation forced companies to ramp down spending.

The memory market subsequently cratered, leaving manufacturers with a massive supply they couldn’t easily sell. In 2023, data storage manufacturers such as Micron (MU), Seagate (STX), SK Hynix, and Western Digital (WDC) all reported annual operating losses.

And then came the AI boom.

The AI revolution pushed Nvidia (NVDA) to the top due to the high demand for high-performance chips among hyperscalers such as Microsoft (MSFT), Amazon (AMZN), and Alphabet (GOOG).

However, Al data centers don’t just need high-performance chips, they also require access to memory capabilities to process the vast amounts of data AI models create and digest. This led to soaring demand for short-term, high-bandwidth memory (“HBM”), a specialized type of chip needed for data center operations.

However, demand doesn’t just stop at HBM—which SK Hynix, Micron, and Samsung specialize in—because AI data centers also need long-term hard drive storage.

So while companies like Micron and SK Hynix often grab headlines for their rapid, short-term memory RAM chips, traditional hard drives still account for 38% of all data-storage revenue today.

While AI models consume petabytes of data, not all of it has to be accessed at once, making hard drives a reliable and cheaper option for storing “cold data”—data that remains in storage and is not needed for immediate retrieval.

As demand for hard drives continues to build amid the market’s growing memory shortage, Seagate stands as a compelling way to bet on today’s storage market.

Seagate is one of the leaders in mass-capacity storage, having delivered billions of terabytes in capacity over the past 40 years.

The company, just like its peers, fell victim to the boom-and-bust cycle in the data storage market in past years. After generating $11.7 billion in sales, the firm saw its sales figures decline to $7.4 billion in 2023 and just $6.6 billion in 2024.

However, with AI boosting demand, the company has shown clear signs of recovery. During its fiscal year 2025, revenue soared to $9 billion.

And recently, Seagate delivered another strong quarter.

Earlier this week, the company announced results for Q2 of its 2026 fiscal year. The firm delivered revenues of $2.83 billion—a 22% year-over-year improvement—and beat analyst expectations of $2.75 billion.

Seagate also shipped 190 exabytes of storage, a 26% jump over the previous year.

Amid Seagate’s return to growth, investors have already rewarded the company handsomely, with the company’s stock price rising more than 300% over the past year.

And as the company’s profitability has materially improved following cycle lows in 2023 and 2024, the market now expects returns to maintain their ascent to historic highs.

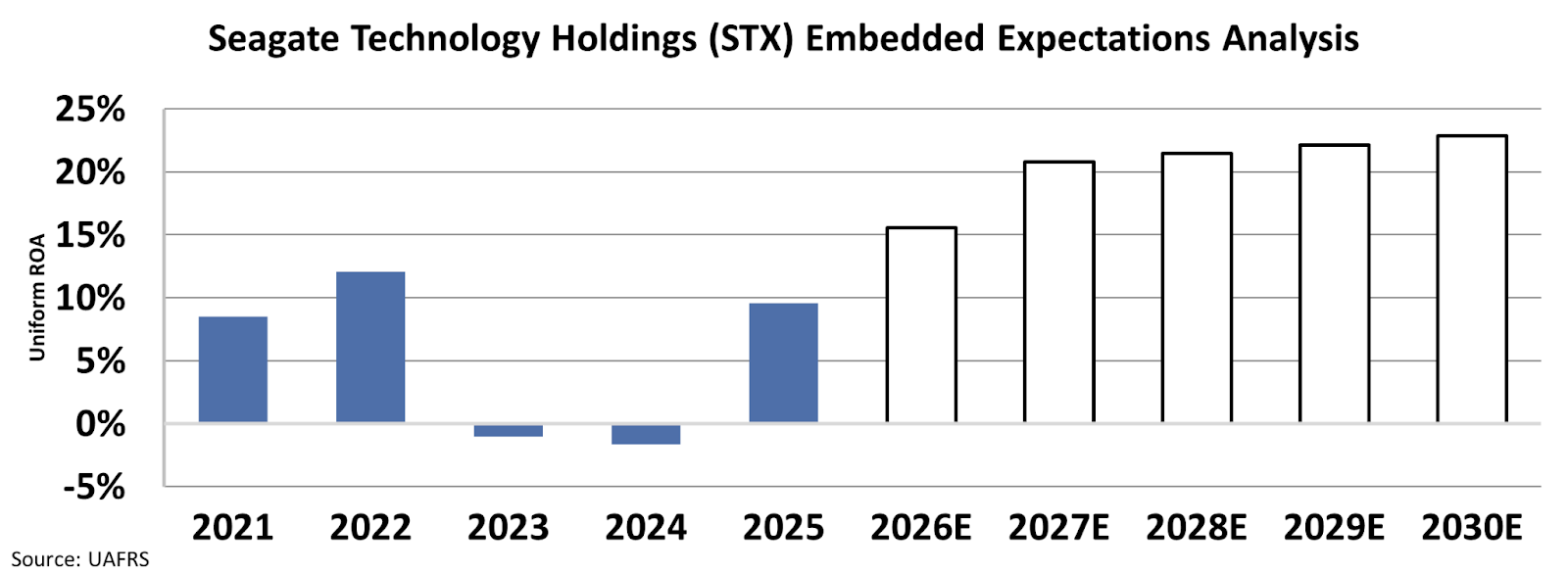

We can see this through Valens’ Embedded Expectations Analysis (“EEA”) framework.

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

At current prices, investors are expecting Seagate’s Uniform return on assets (“ROA”) to rise steeply from 10% in 2025 to 23% by 2030.

<

These expectations may seem lofty, since these are well above the company’s historical performance. But with storage demand soaring, Seagate is becoming an increasingly important player in the world of AI, putting it in a position to meet heightened investor expectations.

As long as memory continues to pose as a bottleneck for the advancement of AI, Seagate could continue to garner the market’s favor.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research