This semiconductor supplier is primed for success as the market rushes to meet demand

While the major semiconductor chip shortage has created butterfly effects across numerous other industries, this one company views the situation as a major opportunity.

As one of the key suppliers in the industry, the company is primed for success as major customers continue to build out excess capacity.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

Over the past few months, the semiconductor shortage has continued, putting numerous industries such as automotive and computer manufacturers under pressure.

A few weeks ago, we highlighted how Texas Instruments (TXN) was impacted.

We discussed the fact that semiconductor chips are being used today in more products than ever. This can be attributed to the explosion of the Internet of Things (IoT) space and how everyone is carrying around and using electronic devices.

Devices with semiconductors range from a phone to more complex items such as products for car functionality. Semiconductor chips are also being used for smart TVs, house lighting, and traffic lights in smart cities, just to name a few.

However, there is currently a serious issue with supplying all the semiconductor chips the world needs.

While it has many people focusing on chip nationalism and chasing limited capacity due to recent shortages, one group of companies view this situation as a major opportunity.

These firms are the pick axe sellers of the chip industry.

Specifically, the companies that are making the semiconductor chips the world wants are seeing massive market opportunities.

One of the largest companies doing this is MKS Instruments (MKSI). The company essentially produces systems and process control solutions that measure, monitor, and even analyze critical manufacturing processes globally.

Through all of its services and product offerings, the company’s customers are better able to manage their supply chain processes and run them more efficiently.

These services are valuable, especially in today’s environment where things do not always go as expected, just like the industry wide semiconductor chip shortage.

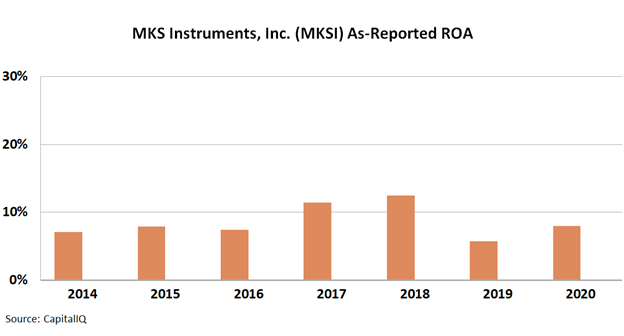

The as-reported metrics of the company highlights modest trends in return on asset (ROA) levels. For example, ROA saw a bump in 2020 from 2019 levels thanks to more demand. This is despite challenges in the midst of the pandemic.

However, the 8% levels in 2020 still remained well below 2017 to 2018 levels at weak single-digit levels.

These numbers may make investors think that even in times of huge demand, the company’s major customers, such as Intel (INTC) and Taiwan Semiconductor (TSM), have serious pricing power over it.

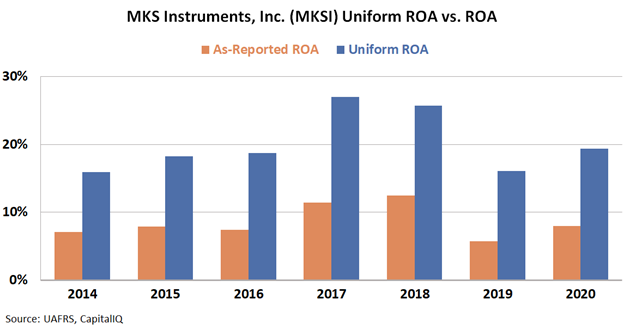

In reality, this is not an accurate picture of MKS Instruments’ profitability levels. Uniform Accounting shows the reality of the prior few years of performance.

In reality, the company’s Uniform ROA levels have not fallen below 16% since 2014. These are robust returns, above the corporate average of around 12%.

See for yourself below.

MKS Instruments is able to generate strong returns by providing vital supplies to all these major customers, letting them make chips.

Even as demand for chips is tight, people want to expand their capacity. In fact, they are forced to, and MKS Instruments is one of the key suppliers they have to rely on.

SUMMARY and MKS Instruments, Inc. Tearsheet

As the Uniform Accounting tearsheet for MKS Instruments, Inc. (MKSI:USA) highlights, the Uniform P/E trades at 17.3x, which is below the global corporate average of 23.7x, but above its own historical average of 14.5x.

Low P/Es require low EPS growth to sustain them. That said, in the case of MKS Instruments, the company has recently shown a 41% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, MKS Instruments’ Wall Street analyst-driven forecast is a 39% and 8% EPS growth in 2021 and 2022, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify MKS Instruments’ $186 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow 2% annually over the next three years.. What Wall Street analysts expect for MKS Instruments’ earnings growth is above what the current stock market valuation requires.

Furthermore, the company’s earning power is 3x the long-run corporate average. Also, intrinsic credit risk is 50bps above the risk-free rate and cash flows and cash on hand are 6x its total obligations—including debt maturities, capex maintenance, and dividends. All in all, this signals low credit and dividend risks.

To conclude, MKS Instruments’ Uniform earnings growth is in line with its peer averages and the company is also trading in line with its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research