This reliable powerhouse offers a convenient way to track the global economic recovery

Despite the noise in recent years around fears of deglobalization, countries and economies around the world remain as interconnected as ever.

With secular trends such as aging populations bound to rearrange the world economy, businesses with a global presence will stand to benefit from diversification. While as-reported metrics have shown weakness in one name poised to ride these tailwinds, UAFRS shows it differently.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Tuesday Tearsheets

Powered by Valens Research

For years, people have talked about using Berkshire Hathaway (BRK.A) as a proxy for tracking the success of the U.S. economy.

The company’s businesses are so well diversified that it has exposure to almost every facet of American life—from insurance and real estate to energy and manufacturing.

And that is quite deliberate, as Warren Buffett is a firm believer in betting on the U.S. economy.

In fact, he has built his investment empire by doing just that—finding companies with strong economic moats that benefit from a vibrant, growing economy.

While this strategy has proven to be fantastically successful for Berkshire Hathaway and Mr. Buffett, there is an entire global economy poised for growth in the 21st century that many investors want exposure to.

To find a similar proxy that can track this global expansion in a fully diversified manner, look no further than the multinational conglomerate 3M Company (MMM).

Last year, we talked about 3M and its ability to supply N-95 masks during the early days of the pandemic—a result of its significant buildup of spare capacity over the past decade.

This enabled the company to weather lockdowns and other COVID restrictions relatively well while many other manufacturers were struggling.

Today, thanks to its broad-based exposure to the global economy (U.S.-based revenue accounts for less than half of its total revenue) across a variety of industries and sectors—including consumer products, healthcare, transportation services, electronics, and safety and industrial—3M has exposure to all corners of the global reopening.

With most of these businesses growing at close to double-digit rates, investors focused on the pace of the global economic recovery should be excited.

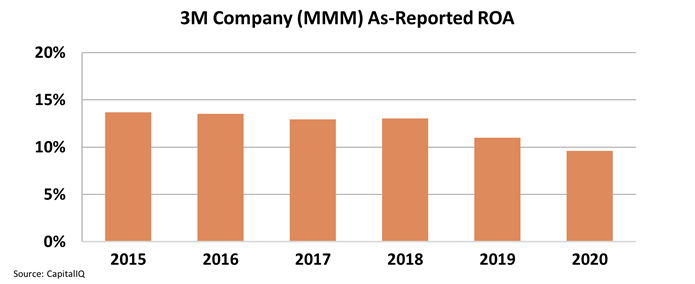

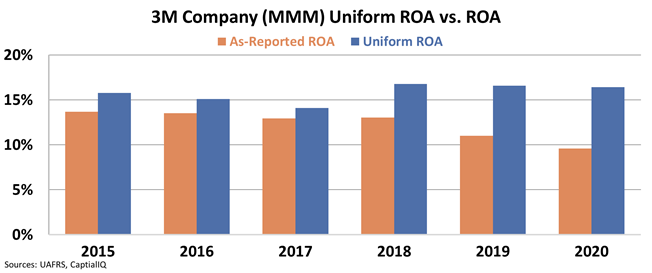

Yet, looking at as-reported metrics such as ROA, which has been declining over the past five years, investors may be worried that the company, and hence the global economy, are under pressure.

In reality, looking at Uniform metrics, which account for distortions inherent to as-reported financial data, we can see not only the resilience of 3M’s diversified business model, but that of the global economy.

While as-reported metrics would have led you to believe the pandemic had a big impact on 3M’s profitability, in truth it wasn’t even a hiccup.

The company has strong, stable returns that position it to keep on being the Berkshire Hathaway of the global economy.

For investors looking to diversify investments outside of the U.S., this is reassuring news the recovery will continue to be global.

SUMMARY and 3M Company Tearsheet

As the Uniform Accounting tearsheet for 3M Company (MMM:USA) highlights, the Uniform P/E trades at 21.5x, which is below the global corporate average of 23.7x, but around its historical average of 21.2x.

Low P/Es require low EPS growth to sustain them. In the case of 3M, the company has recently shown a 2% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, 3M’s Wall Street analyst-driven forecast is an EPS growth of 8% and 7% in 2021 and 2022, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify 3M’s $200 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow 2% annually over the next three years. What Wall Street analysts expect for 3M’s earnings growth is well above what the current stock market valuation requires through 2022.

Furthermore, the company’s earning power is 3x the corporate average. Also, cash flows and cash on hand are about 2x above its total obligations—including debt maturities, capex maintenance, and dividends. This signals a low credit and dividend risk.

To conclude, 3M’s Uniform earnings growth is below its peer averages and is also trading below its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research