The market already moved on from vaccine mania

There is opportunity in crisis – something we just saw in action during the pandemic.

Together with the software and infrastructure improvements that allowed us to work from home, one of the biggest developments was the mRNA vaccine.

Moderna (MRNA) recognized huge profitability thanks to the vaccine. However, the market thinks that the company is not profiting from the mRNA technology at all, and as a result is underpricing the company.

That is why MRNA showed up on our FA Alpha Screen. Its strong profitability and low valuations make it an interesting name.

Investor Essentials Daily:

Tuesday FA Alpha 50

Powered by Valens Research

Human history has shown that crisis often leads to progress.

We developed the flu vaccine during World War I and improved computers at a tremendous pace during World War II.

The pandemic has led to many innovations in very little time.

Digital conference software products have improved to support us working from home, robotics entered a new age, and healthcare pushed its limits.

Of course, an undeniable development was the messenger RNA (“mRNA”) technology. With the need to develop a rapid vaccine, it was unlocked far more quickly than it would have been allowed by authorities.

Another thing that improved very quickly was its famous provider, Moderna (MRNA). The biotechnology company has been working on mRNA therapeutics and vaccines before, but the pandemic has been a game changer.

The company saw profitability skyrocket as its COVID-19 vaccines started to be used globally. Governments and companies lined up for its products to get rid of the pandemic as quickly as possible.

Its Uniform return on assets (“ROA”) jumped from -11% in 2019 to an incredible 258% in 2021 with this booming demand.

This is the type of progression every biotech company dreams of. And yet, the market seems to doubt that Moderna can turn its success during the pandemic into a sustainable business.

The company is trading at an extremely low 4.8x Uniform P/E and 4x Uniform P/B, even lower than 2019 levels.

With the slowdown in Covid cases, Moderna will probably not be able to sustain current levels of profitability going forward. However, current expectations look too pessimistic.

That is why this company was an interesting name. Its massive profitability and low valuations meant that Moderna rose to the top to become an FA Alpha company.

Throughout financial market history, many of the world’s most successful investors have been candid in their belief that Generally Accepted Accounting Principles (“GAAP”) distort economic reality.

Warren Buffett, for example, once said investors should “concentrate on the world of companies, not arcane accounting mathematics.”

Investors who neglect the genuine issues with as-reported accounting can find themselves caught up in investing with the crowd, blindly following hot “themes” without a thorough grasp of how to understand the businesses in question.

The only true way to focus on the “world of companies,” as Buffett suggests investors do, is to present a clear picture of how a business operates, something that can only be done by adjusting financial statements to reflect the arbitrary nature of certain accounting rules that leave much to discretion.

That’s exactly what we’ve set out to do with the FA Alpha, our monthly list of 50 companies that rank at the top for quality, high growth, and low valuations.

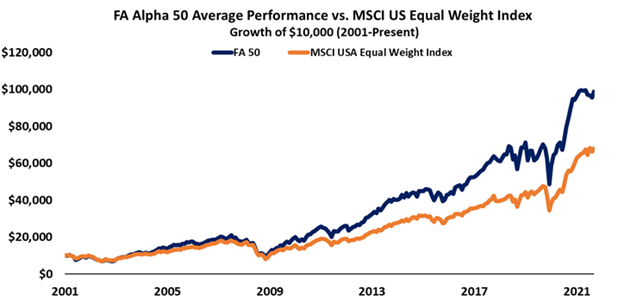

This list has outperformed the market by 300 basis points per year for over 20 years now, effectively doubling the performance of the market by focusing on the real fundamentals and valuations of companies with our proprietary Uniform Accounting framework.

See for yourself below.

To see the other 49 names on the list, click here.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research