The war on tobacco is decades old, and the industry is still fighting strong

It’s difficult to find interesting companies in dying industries.

Typically, investors look to find opportunities that are akin to a slice of a fast-growing pie. As the pie grows, so does the slice.

The “pies” representing the Internet of Things (IoT), go-to-space infrastructure, and electric cars, for example, are growing quickly. Investors are scrambling to get in.

The cigarette business, on the other hand, isn’t a growing pie. An ever-growing cultural and regulatory obsession with health presents a headwind for the smoking industry like none other.

But today’s tobacco company seems to be doing just fine—what gives?

In addition, we highlight the company’s Uniform Accounting Performance and Valuation Tearsheet below.

Investor Essentials Daily:

Tuesday Tearsheets

Powered by Valens Research

Governments around the world have been waging a war on cigarettes.

Bans on advertising, menthol cigarettes, and other flavored products, forced health and safety messages on cigarette boxes, sin taxes, and funding for anti-smoking public health measures have been successful in reducing overall cigarette use.

However, the industry impact is not what it may seem.

The regulations have created a barrier-to-entry. Simply put, small brands don’t have the cushion to absorb the extra costs and reduced demand, so the industry has consolidated around a few major players.

Sure, the pie has been shrinking slightly, but the size of Altria’s (MO) slice has been growing as it gobbles up everything in its path.

Today, nearly 50% of all cigarettes sold in the United States are made by Altria.

Cigarettes are among the most inelastic goods out there. Its customers are largely a captive audience with stable demand.

Speaking of demand, the pandemic has served as a tailwind for vices such as tobacco and alcohol. With more stress, time at home, and stimulus money, consumers have tended towards more vices, as is common during most recessions.

Tobacco sales in 2020 were up 5%, coming off of three years of flatness.

Moreover, despite the regulatory pressures, the cigarette business is still an impressive cash printer. Even in states with 50% sin tax markups, Altria can pocket several dollars on each pack sold because packs cost mere cents on the dollar to produce.

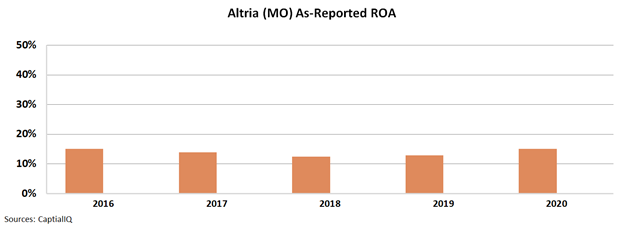

While Altria’s returns have remained stable in the face of increasing taxes, its returns are just slightly above corporate averages in recent years.

However, this is not an accurate picture of Altria’s true economic productivity.

As the industry has consolidated, Altria has increased its monopolistic pricing tendencies. See for yourself.

After adjusting for Altria’s overinflated asset base and other distortions from GAAP accounting, its real profitability trend is revealed. Uniform ROA has expanded from already robust 123% levels in 2016 to 292% in 2020.

This impressive performance comes despite the 88% loss it has taken on its 35% investment into JUUL Labs. If JUUL can engineer a turnaround, Altria will participate in the rally.

The as-reported metrics fail to show just how profitable Altria really is. More importantly, they completely fail to show the company’s underlying profitability trends over the last five years.

Without making the proper adjustments, investors may make directionally wrong decisions about the stocks they’re looking at, leading to less sound analysis.

SUMMARY and Altria Group, Inc. Tearsheet

As the Uniform Accounting tearsheet for Altria Group, Inc. (MO:USA) highlights, the Uniform P/E trades at 12.1x, which is below the global corporate average of 23.7x, but around its own historical P/E of 12.2x.

Low P/Es require low EPS growth to sustain them. In the case of Altria, the company has recently shown a 22% Uniform EPS decline.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Altria’s Wall Street analyst-driven forecast is a 24% and 10% EPS growth in 2021 and 2022, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Altria’s $48 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink by 9% annually over the next three years. What Wall Street analysts expect for Altria’s earnings growth is above what the current stock market valuation requires in 2021 and 2022.

Furthermore, the company’s earning power is 49x the long-run corporate average. Also, cash flows and cash on hand are below its total obligations—including debt maturities, capex maintenance, and dividends. Meanwhile, intrinsic credit risk is 50bps above the risk free rate. All in all, this signals a moderate dividend and low credit risk.

To conclude, Altria’s Uniform earnings growth is significantly above its peer averages. However, the company is trading below average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research