The rating agencies slammed the HMO market in 2008, and are making the same mistake with today’s company

With the market meltdown in 2008, smart credit investors were able to make profitable trades that went against the rating agencies’ intuition. Some bonds were yielding equity-like returns due to massive dislocations.

Today, the ratings agencies are showing the same lack of understanding, marking this HMO name as high-yield, when it is anything but.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

One of my favorite investments of all time took place during the Great Recession. Back when I worked at The Abernathy Group in 2008, we took to the credit market. The credit market essentially froze in 2008, which created massive dislocations and opportunities for gigantic yields.

These market conditions meant some bonds could generate equity-like returns. We ended up trading bonds for an HMO called Coventry Health, a smaller player in the HMO space.

While not as large as companies like Aetna, UnitedHealth (UNH), or Wellpoint (now Anthem), Coventry was large enough and its bonds were liquid.

We investigated the HMO space because insurance companies abide by some of the strictest regulations of any industry including robust capital-on-hand requirements.

Interestingly, Coventry’s bonds were trading at 60 cents on the dollar with yields in excess of 25% while its balance sheet reassured that it had one of the safest profiles we could find. Its capital-on-hand was much higher than was required by regulation, and was comfortably enough to cover its bond obligations.

By reaching across the corporate structure to the bond market, we were able to take advantage of how rating agencies misunderstood corporate financials.

Today, it looks like rating agencies are making the same mistake with Molina Healthcare (MOH). Not only are Coventry and Molina both HMOs competing with the larger players such as Aetna, UNH, or Anthem, they both share the similar bias from rating agencies.

Despite the surge in Molina’s stock since March lows, the major rating agencies are still skittish when rating Molina Healthcare’s debt. Specifically, Moody’s gives Molina a high-yield Ba3 rating, with the implied assumption of a 25%+ risk of default over the next five years.

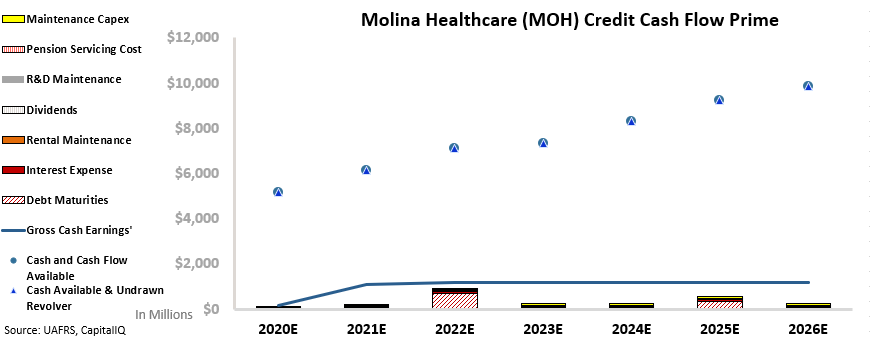

Our Credit Cash Flow Prime (CCFP) analysis is able to get to the heart of the firm’s true credit risk.

In the below chart, the stacked bars represent the firm’s obligations each year for the next five years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

As depicted, Molina Healthcare has massive cash liquidity and therefore should have no issues handling its obligations going forward. On top of this, even if the firm did not have access to this capital, cash flows alone exceed all obligations by a wide margin every year including 2022 and 2025, when the firm has debt maturities.

Rather than a name in distress, Molina Healthcare is actually a cash flow machine. This is why Moody’s Ba3 high yield rating, with a 25%+ risk of default expectation does not make sense.

Using the CCFP analysis, Valens rates Molina Healthcare as an investment grade IG4+ rating. This rating corresponds with a default rate below 2% within the next five years, a more realistic projection once a holistic understanding of the company’s risk is taken into account.

Ultimately, Uniform Accounting and the Credit Cash Flow Prime analysis highlights how Molina’s credit risk profile is much safer than what rating agencies believe. By using Uniform Accounting, investors have the proper context to understand whether market yields for bonds really make sense, or provide opportunities for investment.

SUMMARY and Molina Healthcare, Inc. Tearsheet

As the Uniform Accounting tearsheet for Molina Healthcare, Inc. (MOH:USA) highlights, the Uniform P/E trades at 23.4x, which is around the global corporate average valuation levels, but above its historical average valuations.

Moderate P/Es require moderate EPS growth to sustain them. That said, in the case of Molina, the company has recently shown a 9% Uniform EPS decline.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Molina’s Wall Street analyst-driven forecast is a 3% EPS decline in 2020 and 11% EPS growth in 2021.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Molina’s $220.74 stock price. These are often referred to as market embedded expectations.

The company can have Uniform earnings shrink by 1% per year over the next three years and still justify current stock prices. What Wall Street analysts expect for Molina’s earnings growth is around what the current stock market valuation requires in 2020, but above that requirement in 2021.

Furthermore, the company’s earning power is 3x the corporate average. However, intrinsic credit risk is 140bps above the risk-free rate. Together, this signals a moderate credit risk.

To conclude, Molina’s Uniform earnings growth in line with peer averages and the company is trading in line with average peer valuations.

Best regards,

Rob Spivey

Director of Research

at Valens Research