Moody’s is punishing this company for an event from over a decade ago, and Uniform Accounting shows why that’s wrong

In the late 2000s, investors and economists faced a reality check on the strength and resiliency of the housing market. After a few rocky years and significant work to repair the credit for homeowners and home builders, fundamentals for this market have stabilized and recovered well.

Today’s company is a homebuilder with a presence across the United States. The company is being treated as an elevated credit risk like it was in the late 2000s despite its strong liquidity position and industry growth trends today.

Below, we show how Uniform Accounting restates financials for a clear credit profile. We also provide the equity tearsheet showing Uniform Accounting-based Performance and Valuation analysis of the company.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

The mid to late 2000s were exceptionally dark times for the American economy. The popping of the housing bubble sent shockwaves throughout the global financial system, leading to the stock market crumbling and resulting in millions of Americans losing their jobs.

As many of you may know, a primary catalyst for this collapse was the sale of residential mortgage backed securities (RMBS). These securities are bundles of mortgage payments which should pay the investor regular interest payments.

Investors adored RMBSs in the 2000s. This was in large part due to the rating agencies giving the securities investment grade ratings. Since the housing market was rising so steeply, Moody’s (MCO), S&P (SPGI), and Fitch believed home prices would never go back down.

Furthermore, because most RMBSs were investment grade, banks and insurance companies were able to buy them. Even though many RMBSs would go on to default, institutions were able to speculate when the securities should have been left to hedge funds and other investors.

When the bubble burst, the rating agencies began to scramble. They wanted to put distance between themselves and many of the securities they rated. In an effort to act fast, they made sweeping rating cuts on a number of bonds and derivatives.

However, the agencies were so caught up in a short-term fix, they never prepared themselves for the next disaster. Instead, they responded in a common way to a cataclysmic event, by trying to ensure it never happens again. However, this makes little sense as things never go wrong the exact same way twice.

As the rating agencies’ dropped the ball during the housing crisis, this oversight has led them to still be terrified of homebuilders. It makes little sense to equate a group of companies as risky based on an event which happened a dozen years ago. However, this is what continues to drag down credit ratings for many homebuilders.

One company with an especially egregious rating is KB Home (KBH). KB Home is one of the largest homebuilders in the country and delivers over 10,000 homes a year. The firm has had consistent performance that has not slowed down during the coronavirus pandemic.

KB Home delivered a similar number of homes in the second quarter this year as it did last year. Furthermore, demand for houses has skyrocketed recently, with weekly applications for mortgages to buy a home reaching the highest level since the housing bubble.

However, even with strong fundamentals and positive tailwinds, Moody’s rates KB Home as a high yield Ba3 name. To see why this may be wrong, we look at KB Home’s Credit Cash Flow Prime (CCFP).

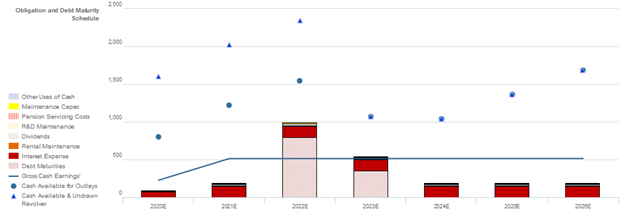

The chart below explains KB Home’s credit risk. The chart compares the company’s obligations (stacked bars) each year for the next seven years against its cash flow (blue line) and cash flow, plus cash on hand at the beginning of each period (blue dots).

The graph shows most of KB Home’s obligations come from debt maturities and interest expenses, which are the hardest to push off. There are also debt maturities in both 2022 and 2023.

KB Home’s cash flows will not be enough to pay off the maturities, which might initially look like a cause for concern. However, the firm’s cash on hand will allow it to pay off all obligations. Furthermore, KB Home has a revolving credit facility to use if cash flows were to lessen in the short run.

Since KB Home is projected to have enough cash flows and cash on hand to cover the next seven years of obligations, Valens rates KB Home as an IG4+ (equivalent to Baa1) credit. This is five notches above Moody’s rating of Ba3 and implies a much smaller chance of bankruptcy.

Moody’s refuses to acknowledge the housing market is much stronger now than in the 2000s. Moody’s and the other rating agencies do not want to make the same mistake twice and it is causing the agencies to be too conservative with the homebuilders sector.

The history of the homebuilders, coupled with two large and near debt maturities, has made Moody’s overstate KB Home’s credit risk.

However, the CCFP has shown KB Home has the cash to pay off these maturities. Without Uniform Accounting, investors would not know KB Home is in reality investment grade quality.

KBH’s Credit Risk Remains Overstated as Operational Sustainability Continues to be Overlooked

Cash bond markets are materially overstating credit risk with a cash bond YTW of 4.241% relative to an Intrinsic YTW of 2.451%, while CDS markets are slightly understating credit risk with a CDS of 129bps relative to an Intrinsic CDS of 182bps. Moreover, Moody’s is materially overstating credit risk with its highly speculative, high-yield Ba3 rating five notches lower than Valens’ IG4+ (Baa1) rating.

Fundamental analysis highlights that KBH’s cash flows should exceed operating obligations in each year going forward. Additionally, although cash flows alone would likely fall short of all obligations in 2022 and 2023 when the firm faces material $797mn and $352mn debt headwalls, respectively, the firm’s expected cash build should allow them to navigate all obligations through 2026. Moreover, the firm’s robust 120% recovery rate on unsecured debt and operational sustainability should allow KBH to access credit markets to refinance, if necessary.

Incentives Dictate Behavior™ analysis highlights positive signals for credit holders. KBH’s management compensation framework should focus management on improving all three value drivers: top-line growth, margins, and asset utilization, which should lead to Uniform ROA expansion and increased cash flows available for servicing obligations.

Additionally, most management members hold significant KBH equity relative to their annual compensation, likely aligning them with shareholders for long-term value creation. That said, CEO Mezger has high change-in-control compensation, indicating he may be inclined to influence other members of management to accept or pursue a sale of the company, increasing event risk.

Earnings Call Forensics™ analysis of the firm’s Q1 2020 earnings call (3/26) highlights that management generated an excitement marker when saying they do not expect to see huge market disruptions in terms of pricing.

However, management may lack confidence in their ability to expand their borrowing capacity and effectively react to changes in the market environment. Moreover, they may be concerned about the sustainability of first-time buyer percentage increases, their Vegas market performance, and their market positioning.

Furthermore, they may be exaggerating their engagement with customers during the pandemic, the openness of studio buyers to make selections online, and their ability to maintain their subcontractor base and business momentum.

KBH’s material debt maturities indicate CDS markets are understating credit risk, while their operating sustainability and robust recovery rate indicate that cash bond markets and Moody’s are overstating credit risk.

As a result, a ratings improvement, tightening of cash bond spreads and a widening of CDS spreads are likely going forward.

SUMMARY and KB Home Tearsheet

As the Uniform Accounting tearsheet for KB Home (KBH:USA) highlights, the company trades at a 15.4x Uniform P/E, which is below global corporate average valuation levels, but around its own historical average valuations.

Low P/Es require low EPS growth to sustain them. That said, in the case of KB Home, the company has recently shown a 78% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, KB Home’s Wall Street analyst-driven forecast projects an 8% EPS decline in 2020, before a 43% growth in 2021.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify KB Home’s $36.40 stock price. These are often referred to as market embedded expectations.

The company can have its Uniform earnings shrink by 1% each year over the next three years and still justify current prices. What Wall Street analysts expect for KB Home’s earnings growth is below what the current stock market valuation requires in 2020, but above its requirement in 2021.

Furthermore, cash flows are above total obligations—including debt maturities, capex maintenance, and dividends. This signals low credit and dividend risk.

To conclude, KB Home’s Uniform earnings growth is below peer averages, and the company is trading in line with average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research