Mortgage Backed Securities: This Time Is Different

Having watched several banks fail in the last week, investors are looking for answers. Folks who were around during the Great Recession may recoil whenever someone mentions that mortgage backed securities are once again involved.

There’s an important distinction though. What’s going on with MBS is different today than it was in 2008, and it’s not nearly as bad.

Today, we’ll take a look at how MBS played a part in bringing down Silicon Valley Bank, and why investors shouldn’t be worried about a repeat of the Great Recession.

Investor Essentials Daily:

The Monday Macro Report

Powered by Valens Research

Banks are blowing up, investors are panicking, and it’s hard not to think back to 2008.

After all, the banking industry was at the heart of the financial crisis 15 years ago. So it’s no surprise that even before the dust has settled, folks are already drawing comparisons between what happened back then and what’s going on today.

One familiar term in particular keeps getting thrown around to discuss the collapses of Silvergate Capital (SI) and Silicon Valley Bank (“SVB”)…

Mortgage-backed securities (“MBS”) brought both of these banks down. And since many people credit MBS for the Great Recession, you might think you should follow the same playbook today that would’ve gotten you through 2008 and 2009.

But as I’ll explain, that’s the exact wrong way to look at it. The current run on banks is nothing like what we saw during the 2008 financial crisis. And you shouldn’t expect the same outcome in the markets, either.

In 2008, banks had a non-performing loan problem.

These institutions were fast and loose with their lending standards. They’d extended a bunch of loans to homebuyers and other consumers that they couldn’t afford.

One of their weapons of choice was the adjustable-rate mortgage (“ARM”). With an ARM, borrowers could lock in a low rate for one, three, or five years. After that, the mortgage would adjust up to market rates.

Investment banks like Bear Stearns took all those loans they originated and bundled them together. Then they chopped that bucket of loans up into securities, selling them as MBS.

For a while, everything went great. At the low introductory rates, borrowers could afford the mortgages for a few years. But when rates suddenly snapped up, folks couldn’t afford their homes anymore. This led to waves of home foreclosures.

MBS were marketed as “safe”… and many banks had tons of them on their balance sheets. The now-infamous Lehman Brothers had $85 billion in mortgage exposure versus only $20 billion in equity. It didn’t survive the financial crisis.

As those loans stopped performing, banks had to write them off. And as they marked down the value of their assets, that ate into bank capital buffers—the money they need to keep on their balance sheets to be considered “safe.”

Once capital buffers got too tiny, banks had to scramble to raise capital. It was the only way to avoid getting in trouble with regulators.

They also stopped making new loans. The fewer loans they made, the less capital they’d need to protect against those loans defaulting, too.

When investors got wind of what was going on, they panicked. That’s what brought the entire system close to collapsing in September 2008.

The 2023 MBS problem is a very different one.

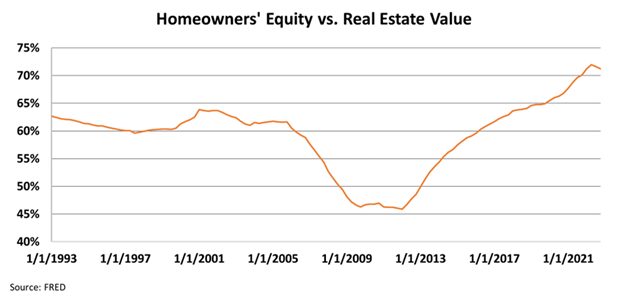

We don’t have an issue with homeowners mailing keys back to the banks. In fact, people own more of their own homes now than at any time in the past 30 years.

The following chart shows homeowner equity as a percentage of the value of all homes on the market. As you can see, equity is at impressive levels today.

Homeowners own more than 70% of their homes. That number fell below 50% during the Great Recession.

And there’s another key difference… Most of these homeowners have locked in their mortgages for 30 years at fixed rates around 3%. There’s no looming reset that will make homes unaffordable.

The risk of defaults on residential MBS is far lower now than it was in 2008. The issue with MBS today has to do with how much they’re worth.

As we mentioned, most of these mortgages pay about 3% to whoever owns them. Right now, if you wanted to lend money to the U.S. government – the safest borrower on the planet – you could get a 3.7% coupon for the next 30 years. That’s 0.7% more interest than you’d get from buying MBS… and it’s risk-free.

Said another way, MBS are worth less today than when these banks bought the securities in the first place.

Eventually, the banks have to reflect the new value of those loans. That means they also have to write down their capital for the “paper losses” they’ve taken on the mortgages they’re carrying.

It’s not that banks think the mortgages will go bad.

If they hold the mortgages until they mature or get refinanced by borrowers, they’re all still good for the money. That’s an important distinction between 2008 and today.

Banks don’t have to mark most MBS for changes in value… because they do plan on holding the securities until they mature. But it’s still hurting their willingness to make new loans.

They want to protect their capital bases so they don’t get in trouble. After all, look at what happened to Silvergate and SVB.

The Federal Reserve’s interest-rate hikes are slowing down lending… which is exactly what the Fed wants. This will help it cool off the economy and slow inflation. It will likely also cause a recession.

That doesn’t mean we’re about to live through another near-collapse of the financial system. You don’t need to batten down the hatches and stock up on canned goods.

The Fed’s actions today are similar to the way it managed the economy in the 1940s. Expect a choppy market for the next year or so, until the central bank feels confident it has a handle on inflation.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research