Smart investors and auto part makers are getting in early on the electric vehicle megatrend

Electric vehicles are a major disruption to the transportation industry. Not only will EVs change the types of energy we use, they will change the types of parts we need in our cars.

While many parts suppliers will be scrambling to keep up with changing demands, today’s firm benefits from being an early adopter to the EV market, but it still looks cheap on an as-reported basis.

When looking through a Uniform Accounting lens, it looks like smart investors may already understand the connection.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Tuesday Tearsheets

Powered by Valens Research

With President Biden’s proposals and initiatives to achieve clean energy, the electric vehicle industry has been booming.

One of the exciting yet less reported pieces of news from the emergence of electric vehicles is how these cars should actually save customers’ money. The maintenance costs for these vehicles should be lower as these vehicles have less that can go wrong.

More intuitively, electric vehicles have the potential to harness cleaner energy with less need for gas and oil consumption.

With no engine, exhaust, or any other liquid oil components, there are fewer parts to the car that could possibly break down.

By owning electric vehicles, customers only have to worry about replacing simple fixes such as windshield fluid or distinct parts such as brakes.

This is great for customers looking to minimize unexpected expenses. However, it might not be so great for companies that play an integral part in the supply chain for internal combustion cars.

It could mean that as more and more electric vehicles take up additional market share in the space, these aforementioned companies will get wiped out.

As a result, so many of these companies are scrambling to adapt and provide solutions for electric vehicles as well.

One of the large auto suppliers that has successfully done this is Meritor (MTOR).

The company has transitioned its product offering to ensure that it makes power trains for electric heavy vehicles as well as electric cars.

On an as-reported basis, the market is pricing the company to be wiped out. And it has been for quite some time.

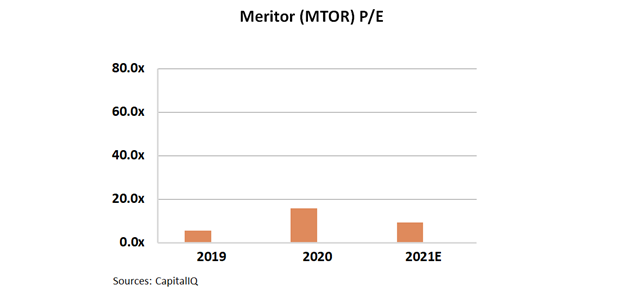

For example, Meritor’s price to earnings ratio (P/E) is trading at a deep discount relative to the market currently.

Its as-reported P/E is currently 9.0x, higher than 6.0x levels in 2019. Even at its current valuation, it is trading below corporate averages around 20.0x.

Investors looking at this picture of Meritor may expect this to be a smart buy into used parts and the future of EVs.

In reality, this is not an accurate picture of Meritor’s valuation.

The company is not trading as cheaply as it seems. The firm is really trading at a 14.0x Uniform P/E multiple, making it more expensive than investors believe.

When looking through a Uniform Accounting lens, it becomes clear the company’s successful transition to offering electric services has paid off.

While investors may not like the reality, it is more reasonable given the immense tailwinds behind the surge in demand for electric cars.

These valuations are more in line with strong auto suppliers, and unfortunately less compelling than the as-reported figures imply.

SUMMARY and Meritor, Inc. Tearsheet

As the Uniform Accounting tearsheet for Meritor, Inc. (MTOR:USA) highlights, the Uniform P/E trades at 14.1x, which is below the 23.7x global corporate average valuation levels and its historical average valuations of 29.5x.

Low P/Es require low EPS growth to sustain them. In the case of Meritor, the company has recently shown a 122% Uniform EPS decline.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Meritor’s Wall Street analyst-driven forecast is a 369% EPS decline in 2021 and a 127% EPS growth in 2022.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Meritor’s $27 stock price. These are often referred to as market embedded expectations.

Meritor is being valued as if Uniform earnings were to grow by 33% per year over the next three years. What Wall Street analysts expect for Meritor’s earnings growth is below what the current stock market valuation requires in 2021, but above that requirement in 2022.

Furthermore, the company’s earning power is below the corporate average. Also, cash flows and cash on hand are above its total obligations—including debt maturities and capex maintenance. Together, this signals a moderate credit risk.

To conclude, Meritor’s Uniform earnings growth is well below peer averages, and the company is also trading below average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research