Sometimes neither bond or stock investors are smarter, Uniform Accounting cash flow analysis highlights that for this company both are wrong

Credit investors look smart in bear markets, and equity investors look smart in bull markets, but sometimes both can look as if they’re completely ignoring economic reality

This firm’s struggles following the oil price glut called into question its future prospects and cash flow generation, but even following a recovery and despite investment-grade fundamentals, credit markets, stock markets, and ratings agencies all seem to still be penalizing the firm.

Below, we show how Uniform Accounting restates financials for a clear credit profile.

We also provide the equity tearsheet showing Uniform Accounting-based Performance and Valuation analysis of the company.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

There’s an old adage on Wall Street that goes “credit investors are smarter than equity investors.”

Although fixed income investors would love for that to always be the case, even they would acknowledge that that is only sometimes accurate.

In a downturn, credit investors often fare much better than equity investors because they are, first and foremost, risk-focused. Even when the economy struggles, prudent bondholders can rely on consistent interest payments and their legal seniority thanks to the contracts the debt is based on to help them weather corporate profit declines.

However, in an upswing, equity investors reign supreme, riding the tailwinds of increased spending, better earnings, and more confident market sentiment.

This offsetting relationship can be used to simplify risk-reward trade-offs. Credit investors are more inherently risk-averse, and they should be.

The nature of fixed income securities offers limited upside relative to stocks, as they consist largely of regular payments, and less so on security appreciation. However, the downside is still very real as credit investors, like shareholders, still risk losing nearly all of their investment in the case of a bankruptcy.

However, although one can argue endlessly whether credit investors or equity investors are smarter, there appear to be times when both are wrong.

Both credit and equity markets lagged economic reality for The Manitowoc Company (MTW).

From 2014-2018, Manitowoc faced intense pressures, as the oil price glut and the strength of the US dollar crippled crane market demand. Over this time period, returns hovered below cost-of-capital levels, and the firm even had grossly negative EBIT in 2016.

Although its end-markets have since largely recovered, the markets have yet to feel comfortable with the future prospects of the firm. As such Manitowoc’s market capitalization has fallen from $4 billion in early 2014 to below $500 million today.

However, when looking at the firm through a Uniform Accounting lens, it becomes evident that current market sentiment, particularly among credit investors, may be unwarranted.

For any creditor, the core question for credit risk lies in a company’s ability to pay off its debts. If a company can pay off its debts with no issues, then it should be an investment grade.

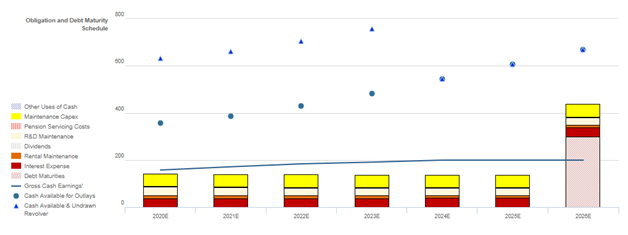

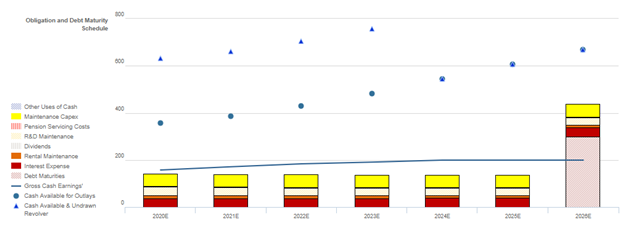

As demonstrated in the chart below, it seems like Manitowoc should fit the bill as an investment grade name.

The company’s operations have recovered since its struggles from a couple years ago. In fact, cash flows alone are expected to be about 1.33x operating obligations in each year over the next seven years, providing a fairly substantial buffer, even if end-market conditions do deteriorate in the near-term.

This cash flow strength should help build enough excess cash to service all of its debt maturities going forward. Since its $300 million of debt maturities in 2026 are its only real existing debt concerns, Manitowoc should have no issues repaying its creditholders, and has significant time before debt maturities become an issue.

In fact, the firm already has $200 million in cash on hand, highlighting its success in building up a creditor’s most coveted asset—cash—even when it struggled.

Only using a UAFRS framework can investors see how wildly overstated credit risk is for the firm. Perhaps following a record-long bull market, credit investors have started to think too much like stock investors.

By analyzing the cash flows and debt obligations of Manitowoc, we can see that it is not a highly speculative credit name, as its Moody’s B2 Rating suggests. Rather, with strong cash flows and plentiful cash on hand, Manitowoc looks to us much more like an investment-grade name.

Cash Bond Markets Overstate MTW’s Credit Risk Even With Strong Cash Flows

Credit markets are grossly overstating MTW’s credit risk with a cash bond YTW of 11.080%, relative to an Intrinsic YTW of 5.440% and an Intrinsic CDS of 495bps.

Furthermore, Moody’s is materially overstating the firm’s fundamental credit risk, with their highly speculative B2 credit rating seven notches lower than Valens’ IG4+ (Baa1) credit rating.

Fundamental analysis highlights that MTW’s cash flows should comfortably exceed operating obligations in each year going forward. In addition, the combination of the firm’s cash flows and expected cash build should be sufficient to service all obligations, including a material $300mn debt maturity in 2026.

Furthermore, MTW boasts a robust 135% recovery rate on unsecured debt, indicating the firm should be able to access credit markets to refinance, if necessary.

Incentives Dictate Behavior™ analysis highlights mostly positive signals for credit holders. MTW’s compensation framework should drive management to focus on all three value drivers: sales, margins, and asset utilization, leading to Uniform ROA expansion and increased cash flows available for servicing obligations.

In addition, most management members are not well compensated in a change-in-control, indicating they are not incentivized to pursue a sale or accept a buyout of the firm, reducing event risk.

However, management is not penalized for overleveraging the balance sheet in order to finance growth, and management members are not material holders of MTW equity, indicating that they may not be well-aligned with shareholders for long-term value creation.

Earnings Call Forensics™ of the firm’s Q4 2019 earnings call (2/7) highlights that management generated an excitement marker when saying their aftermarket revenue grew by 2%, with overall margin improvement.

In addition, they are confident their Q4 adjusted operating cash flow performance was outstanding and that their competitors have a lot of stored inventory.

However, management may be concerned about their new crane launches, their aftermarket facility in Lyon, France, and a potential decline in their backlog. Moreover, they may be exaggerating the flexibility of their cost structure, their ability to service mobile and tower crane customers, and the potential of plant rationalization in Europe.

MTW’s strong cash flows, expected cash build, and robust recovery rate indicate that credit markets and Moody’s are overstating credit risk.

As such, a tightening of credit spreads and ratings improvement are likely going forward.

SUMMARY and The Manitowoc Company, Inc. Tearsheet

As the Uniform Accounting tearsheet for The Manitowoc Company, Inc. (MTW) highlights, the company trades at a 14.9x Uniform P/E, which is below both global corporate average valuation levels and its historical average valuations.

Low P/E’s only require low EPS growth to sustain them. That said, in the case of MTW, the company has recently shown a 2,000%+ Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, MTW’s Wall Street analyst-driven forecast projects a 46% decline in earnings in 2019 and rebound growth of 74% growth in 2020.

Based on current stock market valuations, we can back into the required earnings growth rate that would justify $9 per share. These are often referred to as market embedded expectations. In order to meet the current market valuation levels for MTW, the company would just have to have Uniform earnings shrink by 10% each year over the next three years.

Wall Street analysts’ expectations for MTW’s earnings growth are far above what the current stock market valuation requires.

However, MTW’s Uniform earnings growth is below peer average levels, while the company is trading above peer valuations.

Furthermore, the company’s earnings power is only 1x corporate averages. But with total obligations, including debt maturities, maintenance capex, and dividends, that are above total cash flows, this signals a low risk to its dividend or operations.

To summarize, MTW is expected to see below average Uniform earnings growth in 2019, which is expected to rebound in 2020. However, the company is trading above average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research