Gas stations like Murphy USA don’t make money the way you would believe

Equity investors are always looking at long-term trends, as the power of owning stock is being entitled to the cash flows into perpetuity. This means it’s easy for long-term trends to be priced into stocks.

However, investors looking at the transition to electric vehicles as the death of gas stations may be getting ahead of themselves. Furthermore, credit investors should be taking a different approach to risk entirely.

Today, we’ll use Uniform Accounting to get to the heart of Murphy’’s true credit risk and decide whether Wall Street has gotten it wrong yet again.

Also below, a detailed Uniform Accounting tearsheet of the company.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

While leveraging long term “themes” to inform investment decisions can lead to uncovering alpha, it can also mean investors write off whole industries they should be paying more attention to.

This often happens when analysts study gas station businesses, and assume that the profit must be coming from the gas they are storing and pumping out every day.

In fact, the business of pumping gas itself is capital intensive and low margin, as gasoline is a commodity that is indistinguishable from the gasoline at any other station. In reality, the highest margin transactions in gas stations are all of the products being sold in the convenience store.

This means if the food and beverages inside of the gas station are the businesses bread and butter, the transition to electric vehicles might not be a death knell for gas stations, as paradoxical as it seems. Through changing out gas pumps for charging stations, the industry may continue on with “business as usual.”

However, the ratings agencies are currently viewing the theme of the emergence of EVs as the end of the line for businesses like Murphy USA, a chain of gas stations across the United States. By specializing even more in the convenience store side of the business, Murphy USA should be even better positioned to thrive under this brave new world.

And yet, all three of the large ratings agencies are rating the name as one in distress with the equivalent of a BB+ rating. This translates to a chance of defaulting over 10%.

We see things differently here at Valens.

Using our Credit Cash Flow Prime (“CCFP”) framework, we can get to the heart of Ryder’s true fundamental credit risk.

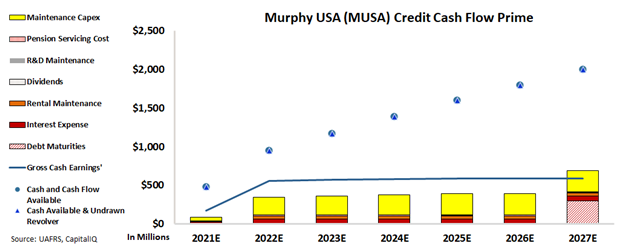

In the chart below, the stacked bars represent the firm’s obligations each year for the next seven years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand available at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

As you can see, Murphy USA is able to cover all of its operating obligations with its cash flows alone for the next 7 years. Furthermore, it is building a sizable amount of cash on its balance sheet, which means it should have no issue whatsoever with paying off its small debt obligation of $300 million in 2027.

Not only is Murphy USA not anywhere close to financial troubles, but it also has plenty of capital to invest in new EV infrastructure and get ahead of its competitors over the next decade.

S&P’s BB+ high-yield rating for Murphy USA does not reflect reality. Instead it highlights Wall Street’s blindness to true credit risk.

That’s why we rate the company as having a much lower risk with an investment-grade rating of IG4+, which corresponds to a default rate of less than 2%.

Using Uniform Accounting, we can see through the distortions of as-reported numbers to get to the true fundamental credit picture for companies in transition such as Murphy USA.

To see Credit Cash Flow Prime ratings for thousands of other companies we cover, click here to learn more about the various subscription options now available for the full Valens Database.

SUMMARY and Murphy USA Inc.Tearsheet

As the Uniform Accounting tearsheet for Murphy USA Inc. (MUSA:USA) highlights, the Uniform P/E trades at 19.9x, which is below the global corporate average of 24.0x, but above its historical P/E of 15.5x.

Low P/Es require low EPS growth to sustain them. That said, in the case of Murphy, the company has recently shown a 157% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Murphy’s Wall Street analyst-driven forecast is for a 3% for 2021 EPS Growth and 30% EPS shrinkage in 2022.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Murphy’s $190 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink by 10% over the next three years. What Wall Street analysts expect for Murphy’s earnings growth is above what the current stock market valuation requires in 2021 but below 2022.

Furthermore, the company’s earning power in 2020 is 3x the long-run corporate average. Moreover, cash flows and cash on hand are above its total obligations—including debt maturities, capex maintenance, and dividends. Additionally, intrinsic credit risk is 80bps above the risk-free rate. All in all, this signals a low credit and dividend risk.

Lastly, Murphy’s Uniform earnings growth is below peer averages, but the company is trading above average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research