Near-term bumps haven’t changed the overall picture for the economy and rate cuts

For most of the year, the market treated interest rate cuts as a simple story. However, all of that changed in September when the Fed cut rates.

Once rates were cut, the market took it as a sign that a major rate-cutting cycle was about to begin. And as a result, traders expected rates to drop as low as 2.5% by late 2026.

However, expectations haven’t lined up with reality. And as a result, sentiments have shifted and sell-offs have occurred, despite strong earnings growth and healthy credit conditions.

In other words, the recent sell-offs aren’t due to negative conditions, but simply investors getting ahead of themselves on rate cuts.

Investor Essentials Daily:

The Monday Macro Report

Powered by Valens Research

For most of 2025, investors treated interest rate cuts as a simple story. But all that changed when the Federal Reserve cut rates in September. And when it did, the market took it as a sign that a major rate-cutting cycle was about to begin.

Within a few weeks, traders were expecting rates to drop as low as 2.5% by late 2026. However, monetary policy rarely proceeds at a predictable pace. That’s why over the past month, sentiments have shifted.

It’s not because the underlying economy has weakened. Earnings growth remains strong. Credit conditions are still healthy.

Sentiments changed simply because investors got ahead of the Fed.

Central bank members are no longer speaking with one voice. A December rate cut, which seemed like a done deal in early fall, has become a point of debate.

Fed Chair Jerome Powell even went on the record at the end of October, saying a December cut is “not a foregone conclusion.”

His comments sparked some of the sell-off over the past few weeks. In the wake of the news, the market fell as much as 5%. And it’s still down 2%. Powell also dampened the market’s expectations for future rate cuts.

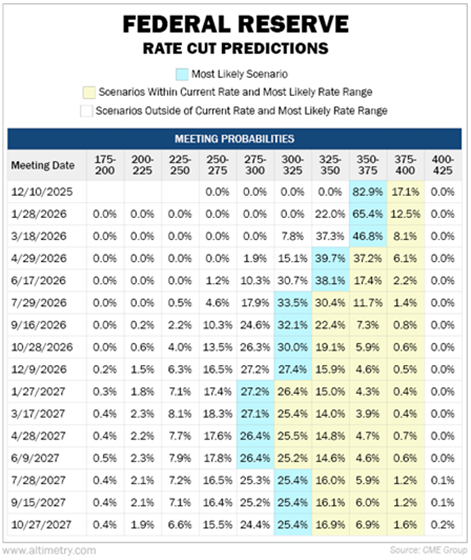

Interest rate expectations and sentiment in the futures market can be tracked through the CME FedWatch tool.

As mentioned above, investors thought they’d get rates as low as 2.5%. But now, they’re not convinced rates will drop below 3% in 2026.

Take a look…

Some Fed officials don’t want to cut rates any further until inflation reaches the 2% target.

Others argue that cooling labor data warrants more cuts. This divide has the market concerned about what’s next.

This reset hasn’t changed the bigger picture, though. It has simply pulled some heat out of a market that got a little too comfortable.

At the same time, investors seem to be forgetting about an important event that’s just around the corner. Powell’s term ends on May 15, 2026. And President Donald Trump has spent the year pushing for much lower rates.

A divided December meeting won’t alter that trajectory. Trump has made it clear he’ll appoint a new Fed chair who favors more rate cuts.

This environment goes far beyond the next six weeks. Near-term bumps haven’t changed the mid-term story. Rate cuts are still the path forward.

Earnings growth remains strong. Expectations are running at or above 9% growth per year over the next two years. As rates keep falling, credit conditions should improve further.

If anything, today’s slightly cooler sentiment makes the overall setup healthier.

Taken together, this adjustment in expectations sets up a favorable backdrop for the end of 2025. and into 2026.

The recent sell-off takes a bit of pressure off sentiment. The economy underneath remains intact.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research