Clean energy companies are listening to Elon Musk on cryptocurrency mining

With the collapse in value of many cryptocurrencies due to Elon Musk’s tweets, there has been a significant opportunity for clean energy companies to save the day.

The reason these cryptos have slid is because of the concern around the environmental impacts associated with mining. This is why clean energy solutions could mitigate these challenges.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

The recent sell-off in the whole cryptocurrency market, including bitcoin, can largely be traced back to the weekend Elon Musk made an appearance on Saturday Night Live.

On the show, when asked what exactly Dogecoin was, Elon agreed that the coin was essentially “a hustle”.

However, the other cryptos that fell were not due to Elon’s comment, but a tweet he put out as the work week was starting up.

The tweet revolved around Tesla (TSLA) making an abrupt change, announcing it would no longer be accepting bitcoin to buy their electric vehicles. While the company recently started accepting bitcoin as payment, Elon changed the policy again because of the environment impact bitcoin mining creates.

As a clean energy advocate, and after more studying of the economics of bitcoin, Elon came to believe that bitcoin and other cryptocurrency mining and transaction processes are increasing greenhouse gas emissions.

Elon did not see any convincing evidence the mining of these cryptos were actually using green energy as they claimed to be.

After all, cryptocurrencies are energy intensive.

Perhaps, energy companies such as NextEra Energy (NEE) took note of this. These kinds of companies can actually be a main part of the solution.

NextEra Energy has been focused on becoming one of the leaders in clean energy in the U.S. And thanks to that, the company has grown to have the largest market cap in the utility industry, at almost $150 billion.

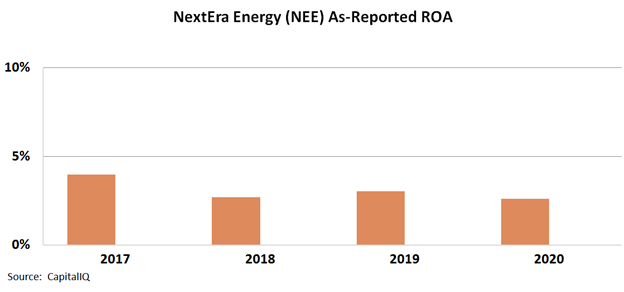

On an as-reported basis, NextEra Energy’s major investments in clean energy have not warranted its rising valuations.

This is because the company’s return on assets (ROA) have faded from already weak 4% levels in 2017 to weaker 3% levels in 2020.

The company is barely generating returns above its cost-of-capital. Perhaps investors assume like the wide utility sector it generates some of the weaker returns of the market.

See for yourself below.

In reality, this is not an accurate picture of NextEra Energy’s profitability levels.

The company is not generating weak returns–it is actually posting solid returns within the industry.

Specifically, since 2017, NextEra Energy has been able to maintain Uniform ROA levels of around 5%.

The average Uniform ROA in the industry is around 4%, so the company is posting higher returns than the average.

These discrepancies are material, and the company is actually expected to keep improving on its ROA trends.

This highlights the fundamental acceleration within the business, especially as its investments in clean energy begins to scale.

SUMMARY and NextEra Energy, Inc. Tearsheet

As the Uniform Accounting tearsheet for NextEra Energy, Inc. (NEE:USA) highlights, the Uniform P/E trades at 30.2x, which is above the global corporate average of 23.7x, but below its own historical average of 33.2x.

High P/Es require high EPS growth to sustain them. That said, in the case of NextEra, the company has recently shown a 6% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, NextEra’s Wall Street analyst-driven forecast is a 111% and 6% EPS growth in 2020 and 2021, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify NextEra’s $73 stock price. These are often referred to as market embedded expectations.

The company needs to have Uniform earnings grow by 20% per year over the next three years in order to justify current stock prices. What Wall Street analysts expect for NextEra’s earnings growth is above what the current stock market valuation requires in 2021, but below that requirement in 2022.

Furthermore, the company’s earning power is below the long-run corporate average. Also, cash flows and cash on hand are below its total obligations—including debt maturities, capex maintenance, and dividends. All in all, this signals a high credit and dividend risk.

To conclude, NextEra’s Uniform earnings growth is well above its peer averages while the company is trading in line with its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research