New trends in the battery market left rating agencies in the dark about this battery maker’s credit risk, Uniform Accounting lights the way

During periods of crisis, people tend to stock up on essential goods. We saw this during the pandemic when toilet paper was worth its weight in gold. During natural disasters, people make a similar run on batteries.

Today’s company is one of the world’s largest battery makers, and a few changes over the last few years have had credit markets concerned.

Below, we show how Uniform Accounting clarifies the financials for a clear credit profile. We also provide the equity tearsheet showing Uniform Accounting-based Performance and Valuation analysis of the company.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

As you may remember, grocery stores were like a battlefield in early March. People were concerned about being locked in their houses during the pandemic, so they stockpiled durable goods. At one point, toilet paper and Clorox wipes were the hottest commodities available.

Not only was demand through the roof, but disruptions in the supply chain restricted the amount of these products on the shelf. Some factories were shut down, and distribution companies were constrained. This led to mass shortages and rationing on these everyday items.

This isn’t a totally unusual phenomenon.

During more common disruptive events like hurricanes and snowstorms, people often make runs on water, bread, and even batteries. Batteries are needed to power items like flashlights, radios, backup generators, and more. It’s a consumer staple people will always need during a crisis.

However, the last few years have brought a paradigm shift to the battery industry. Lithium batteries have increased in popularity. These batteries are rechargeable, reducing the need to continuously buy new batteries.

Companies like Energizer Holdings, Inc. (ENR) appear to have been hurt by this trend. Energizer is one of the world’s largest battery manufacturers. While the firm does offer its own rechargeable categories, its bread and butter are still its single-use batteries.

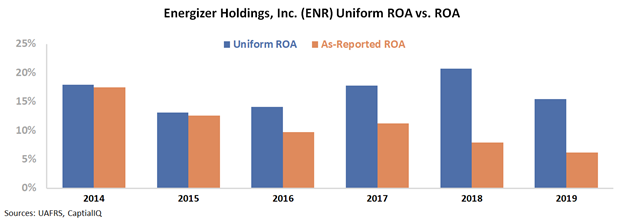

It appears as though the rise of rechargeable batteries has dented Energizer’s sales. Its as-reported return on assets (ROA) has fallen from 18% in 2014 to only 6% in 2019. People appear to be buying fewer batteries, hurting Energizer’s profitability.

The major credit rating agencies have reacted to the above trend. Moody’s rates Energizer a high-yield B1 credit. A B1 rating translates roughly to a 25% probability the firm will be bankrupt within the next five years.

However, looking at Uniform Accounting, we can see the true returns and credit safety of the business. Due to distortions in as-reported accounting, including the treatment of interest expense, everyone from Wall Street to the rating agencies has missed Energizer’s real profitability.

Energizer’s Uniform ROA was actually at 15% in 2019, compared to its 6% as-reported ROA. The emergence of lithium batteries appears to not have materially impacted Energizer’s business.

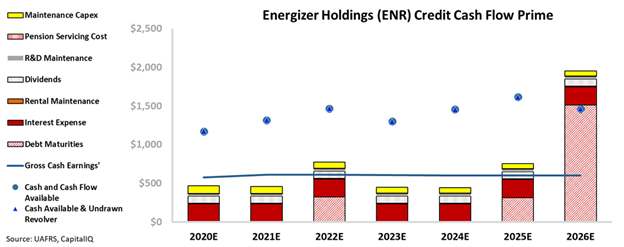

These stronger cash flows show through on the credit side as well. Looking at the firm’s Credit Cash Flow Prime (CCFP), we can see Energizer’s true credit risk.

As the CCFP shows, Energizer is a much stronger credit than what rating agencies give it credit for.

Energizer’s cash flows alone should exceed nearly all operating obligations in each year going forward. Moreover, Energizer’s sizable cash build will enable the firm to meet all obligations until 2026, when it faces a material debt headwall.

Ultimately, Energizer is a much safer credit risk than what rating agencies give it credit for. Thanks to the company’s strong cash flows and sizable cash balance, we rate Energizer as a much safer IG4 (Baa2) credit. This investment grade rating estimates less than a 2% risk of default for Energizer, a far cry from the 25% implied by Moody’s.

It is only when using Uniform Accounting and sorting through the noise can we see the true risk of this battery business.

Credit Markets and Ratings Agencies Overstate ENR’s Credit Risk Despite Strong Cash Flows and Long Debt Runway

Bond markets are materially overstating credit risk, with a bond YTW of 3.977% relative to an Intrinsic YTW of 2.347% and an Intrinsic CDS of 281bps. Furthermore, Moody’s is also materially overstating ENR’s fundamental credit risk, with its B1 rating five notches lower than Valens’ IG4 (Baa2) rating.

Fundamental analysis highlights that ENR’s cash flows alone should exceed operating obligations over the next six years.

Additionally, after the firm’s recent debt issuance, cash flows and cash on hand should be able to service all obligations until the firm faces a $1.5 billion headwall in 2026. This long runway to improve operations is important, as ENR has a lackluster 20% recovery rate and modest market capitalization, which may make it difficult to access credit markets to refinance.

Incentives Dictate Behavior™ analysis highlights positive signals for credit holders. ENR’s compensation framework should drive management to focus on improving margins and expanding revenue, while limiting capex, which should lead to Uniform ROA improvement and growth over time.

Moreover, management’s change-in-control compensation suggests management may not be incentivized to actively pursue a takeover or sale of the company, reducing event risk. Furthermore, management members are material holders of ENR equity, indicating they are well aligned with shareholders for long-term value creation.

Earnings Call Forensics™ of the firm’s Q3 2020 earnings call (8/5) highlights that management is confident in their ability to generate adjusted free cash flow of $300 million+ for the year and rejuvenate the Auto Care business’ innovation pipeline. In addition, they are confident in their e-commerce abilities.

However, management is also confident EPS will decrease. Moreover, they may lack confidence in their ability to sustain battery market share gains, execute their digital conversion tactics, and fully hedge commodity costs.

Furthermore, they may have concerns about airfreight costs increases continuing into 2021, currency and pandemic-related headwinds, and the impact of shelter-in-place orders in their international markets. Additionally, management may be exaggerating their commitment to pay down debt, and the similarities between U.S. battery usage and other developed markets.

Finally, they may lack confidence in their ability to quickly adapt to an evolving operating environment and emerge from the pandemic stronger.

Given ENR’s current cash liquidity and multi-year debt runway, bond markets and Moody’s are overstating the firm’s fundamental credit risk. As such, a tightening of bond spreads and ratings improvement are likely going forward.

SUMMARY and Energizer Holdings, Inc. Tearsheet

As the Uniform Accounting tearsheet for Energizer Holdings, Inc. (ENR:USA) highlights, the company trades at a 14.3x Uniform P/E, which is below global corporate average valuation levels, but around its own historical average valuations.

Low P/Es require low growth to sustain them. That said, in the case of Energizer, the company has recently shown a 9% Uniform EPS contraction.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Energizer’s Wall Street analyst-driven forecast projects a 10% and 24% EPS growth in 2020 and 2021, respectively.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Energizer’s $45 stock price. These are often referred to as market embedded expectations.

The company needs to grow its Uniform earnings by 9% each year over the next three years to justify current prices. What Wall Street analysts expect for Energizer’s earnings growth is above what the current stock market valuation requires in 2020 and 2021.

Furthermore, the company’s earning power is 3x the corporate average. However, cash flows and cash on hand are below its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals high dividend and credit risk.

To conclude, Energizer’s Uniform earnings growth is in line with its peer averages, but the company is trading well below its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research