The next recession in the U.S. isn’t going to be as bad as you think. Here’s why

The Federal Reserve had been aggressively raising interest rates for the past year. The federal-funds rate – the interest rate controlled by the Fed – climbed from 0.25% in March 2022 to 5% today.

Sooner or later, the Fed’s actions will likely tip us into a recession. That’s the cost of doing battle with inflation. And lately, most folks seem to be leaning toward “sooner.”

Yet even as interest rates spiked, unemployment has stayed low. It has been below 4% since the beginning of last year.

Consumer spending has also been very healthy. And that’s with 14 months of 6%-plus inflation. Even homebuilders are still recording impressive orders.

The economy is chugging along. Perhaps the mess in regional banks will cool things off. Even so, the question remains. How has the economy stayed so resilient?

As I’ll explain today, it all boils down to consumer balance sheets. There’s a lot of confusion about how healthy consumer finances are today. We’ll share a few thoughts on why many people are more worried than they should be.

Investor Essentials Daily:

The Monday Macro Report

Powered by Valens Research

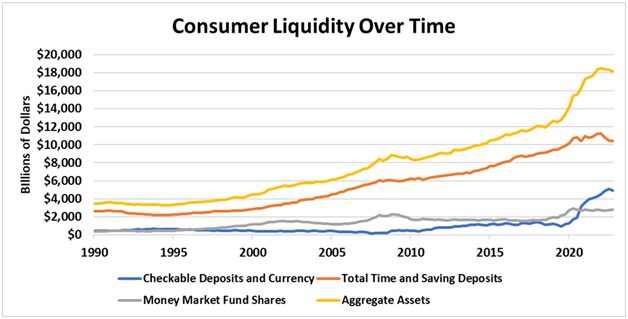

Consumers are swimming in cash.

At the height of the pandemic, a lack of spending and multiple injections of government stimulus meant consumers saved a ton of money. Most folks understand this on some level.

What they might not fully grasp is just how massive this cash balance is. In the past four years, consumer cash balances increased from $1 trillion to $5 trillion in checking accounts alone. That’s a 400% increase.

While savings accounts haven’t risen quite as fast, balances are still rising. Cash in savings accounts is up by $600 million in the same time frame. And money market investments have grown by more than $1.2 trillion since mid-2017.

You can see this in the following chart.

Keep in mind, this data is only available through the third quarter of 2022. Folks have probably started dipping into some of these assets recently.

Regardless, consumers are sitting on massive amounts of liquidity. They really haven’t had to draw on it yet. All this cash padding will keep the American consumer resilient, even as the economy slows down.

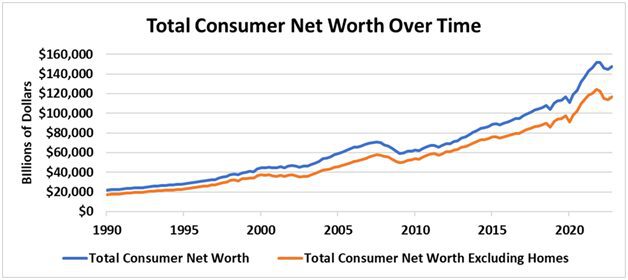

What makes this even more apparent is when you look at consumer net worth.

This metric measures all consumers assets minus liabilities like credit cards and mortgages. Looking at it with or without home equity both tell the same story.

Consumers have added $11 billion in home equity and $37 billion in total equity to their balance sheets since 2020. Said another way, net equity is up more than 30% in the past three years.

Check it out.

As you can see, total consumer net worth is still way higher than it was pre-pandemic. And even as folks draw some of that wealth down this year, we need to remember that it’s starting out from a strong place.

The Fed’s rate hikes will slow spending and cool down the economy. They’ll likely tip us into a modest recession. In short, they’re doing what they’re designed to do.

That doesn’t mean the downturn will be cataclysmic. It’s not going to collapse the economy.

Consumers are comfortable. While recession fears have many folks watching their budgets, they should be able to weather the coming storm.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research