Newmark Group is the bunker which the “Office Apocalypse” desperately needs

It’s no secret to great investors that as-reported financial metrics are unreliable.

To be successful, they make adjustments to the financial statements to produce a true picture of economic reality, one that is otherwise obscured by arcane accounting principles. This allows them to find companies that exhibit three characteristics: high quality, strong growth potential, and low valuations.

Today, we highlight our QGV 50, which emulates this investment strategy to produce outsized returns in excess of the market over long periods of time.

We’ll take a look at one company in particular on this month’s QGV 50, describing how as-reported metrics distort economic reality and can lead investors to miss significant opportunities.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Tuesday Tearsheets

Powered by Valens Research

Throughout financial market history, many of the world’s most successful investors have been candid in their belief that Generally Accepted Accounting Principles (“GAAP”) distort economic reality.

Warren Buffett, for example, once said investors should “concentrate on the world of companies, not arcane accounting mathematics.”

Investors who neglect the very real issues with as-reported accounting can find themselves caught up investing with the crowd, blindly following hot “themes” without a thorough grasp of how to understand the businesses in question.

The only true way to focus on the “world of companies,” as Buffett suggests investors do, is to present a clear picture of how a business operates, something that can only be done by adjusting financial statements to reflect the arbitrary nature of certain accounting rules that leave much to discretion.

The world’s best investors understand the need to make these adjustments, which allows them to focus not on picking out the most popular companies, but rather looking for great names in sleepy areas that the market isn’t paying much attention to. From there, the goal is to then identify quality companies with significant growth potential at reasonable prices.

That’s exactly what we’ve set out to do with the QGV 50, our monthly list of 50 companies that rank at the top for quality, high growth, and low valuations.

This list has outperformed the market by 300bps per year for over 20 years now, effectively doubling the performance of the market by focusing on the real fundamentals and valuations of companies with our proprietary Uniform Accounting framework.

See for yourself below.

It’s easy to believe that as the pandemic continues to abade, commercial real estate will be doomed.

The hybrid-at-best work environment will mean less demand for commercial real estate and potentially dropping prices. This problem will be even worse for office space, as most companies across the United States will not be renewing their current three to five year leases with a majority of firms downsizing their physical space.

In other words, the next few years as these leases expire could be called the office apocalypse.

With an office apocalypse looming, many investors assume any company supporting commercial real estate is also doomed. However, this may in fact be too hasty an assumption.

In industries under huge pressure, companies often look to outsource the work they can and look to vendors who can help them get out of challenging positions.

That’s where Newmark Group (NMRK) comes into play.

Newmark Group is the company any large owner of commercial real estate will go for serving at every step of the ownership process. Newmark helps owners finance their purchases, has representatives to operate real estate if it is labor intensive, and also works as brokers to help with the sale process.

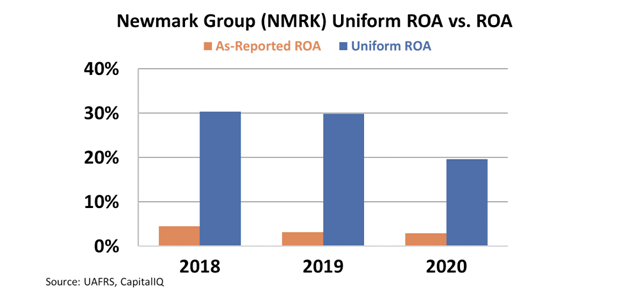

Despite offering all of these services, on an as-reported basis Newmark looks to have been a historically poor performer, with returns right around the cost of capital. Furthermore, returns slid even further during the pandemic to just 3%.

However, the real returns of the company are being thrown off by numerous distortions in GAAP accounting. After we adjust for these discrepancies, a different picture of profitability emerges.

In reality, Newmark Group has been a consistently high performer before the pandemic, with returns around 30%. While returns fell to 20% during the pandemic, they are forecast to reach recent highs of 40% by fiscal year 2021.

The company is so confident in how it’s positioned for the “office apocalypse,” it’s been growing aggressively during the pandemic, with over 90% in the past year alone.

And yet, the market, misunderstanding the company’s position in the real estate market, is valuing it at a cheap Uniform P/E of 10x as though it’s collapsing.

This high-quality market leader in its industry is inexpensively priced and growing aggressively, which is why our QGV 50 Screen discovered the name.

To see the other 49 names on the list, click here.

SUMMARY and Newmark Group, Inc. Tearsheet

As the Uniform Accounting tearsheet for Newmark Group, Inc. (NMRK:USA) highlights, the Uniform P/E trades at 9.9x, which is below the global corporate average of 24.0x, but around its historical P/E of 9.6x.

Low P/Es require low EPS growth to sustain them. In the case of Newmark, the company has recently shown 93% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Newmark’s Wall Street analyst-driven forecast is a 177% EPS growth in 2021 and a 64% EPS decline in 2022.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Newmark’s $18 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow 2% annually over the next three years. What Wall Street analysts expect for Newmark’s earnings growth is above what the current stock market valuation requires in 2021, but below that requirement in 2022.

Furthermore, the company’s earning power in 2020 is 3x above the long-run corporate average. Moreover, cash flows and cash on hand are 2x its total obligations—including debt maturities, capex maintenance, and dividends. All in all, this signals a low credit and dividend risk.

Lastly, Newmark’s Uniform earnings growth is above its peer averages and the company is trading below its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research