The Military Industrial Complex Fuels This Company’s Tailwinds

Dwight D. Eisenhower was not just a great general, he was a visionary.

In 1919, after World War I came to a close, as a Lieutenant Colonel he was assigned as an observer to the First Transcontinental Motor Convoy. This was a road test, literally, to identify how easy it would be to move troops across the continent spanning the United States.

The goal was to move roughly 300 soldiers from DC to San Francisco, to understand how this would work in a time of need, and the problems.

Eisenhower reported back to the Army that plenty of America’s roads were basically impassable. Bridges were too low for army trucks to drive over. Roads too thin or poorly maintained in the Midwest and the desert west to drive over at any pace. There were challenges finding places to do maintenance.

America would not be prepared for a truly national mobilization if needed unless massive investment was made.

In World War II, as the Allies rolled through Germany after D-Day, he was blown away by the German autobahn and how it facilitated rapid deployment. This resonated even further with him that the US needed a similar system.

And in 1953, when the Soviets detonated their hydrogen bomb, his prior beliefs crystalized, and he committed the US to push forward with what became the interstate highway system. The system that became one of the key pieces to the American economy’s strong growth and diversification over the past 70 years.

But the Eisenhower Interstate Highway system wasn’t the only vision that Eisenhower had that proved to be prescient and transformative to the US.

As Eisenhower left office in 1961, he used a phrase that become infamous, expressing concerns about the military industrial complex. He highlighted that the risks of defense contractors’ scope capturing government was one to be aware of.

In 1960, the US spent $45 billion on defense spending. By 2018, the US spent $648 billion, in one year.

The estimated cost of the F-35 system to the US over the life of the aircraft is forecast to be $1.5 trillion. This is only growing.

Some might debate whether this is a good thing or not, but as the world returns to a more multipolar norm in the late 2010s and into the 2020s, it is unlikely to change.

All the defense contractors, be they Lockheed Martin (LMT), Boeing (BA), General Dynamics (GD), Raytheon (RTN), or the many others, will benefit.

One that is particularly well positioned for the modern defense environment is Northrop Grumman (NOC).

One of the major areas that Northrop specializes in is the technology, software, and equipment that makes the modern army run like a machine. Connecting command, control, communications, computers, intelligence, surveillance, and reconnaissance, and the other core competencies of a modern efficiently run military, what they term as C4ISR, is Northrop’s most profitable segment of their business.

After the acquisition of Orbital ATK, it is also building a greater strength in space initiatives that will likely be the next stage of defense innovation.

And this is before discussing their strength in drones and aerospace systems that are at the forefront of the new military.

The company is well positioned in the military industrial environment that continues to have long-term trends towards growth, both in the US and with allies that Northrop also sells to.

The market appears to be misunderstanding Northrop Grumman, mispricing Northrop Grumman’s growth and opportunities, and strong profitability expansion opportunities. The market is expecting the company to see returns decline going forward. With management growing more confident about growth, their Orbital ATK acquisition and their overall outlook, this looks too pessimistic, pointing to reasons for potential upside.

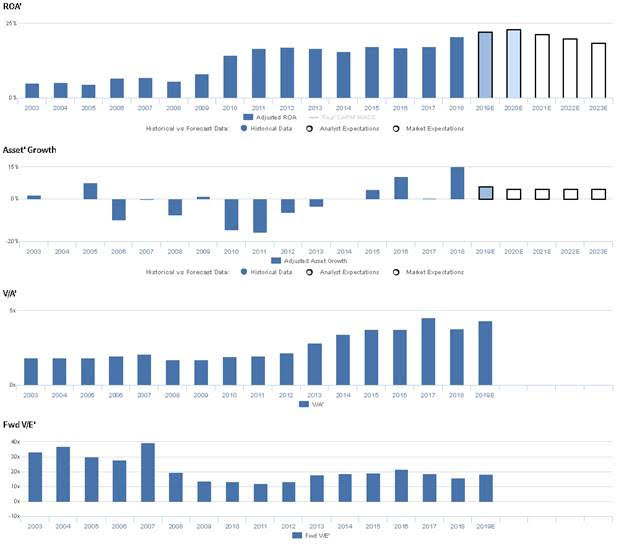

Market expectations are for Uniform ROA to decline, but management is confident about their Orbital ATK transaction and growth

NOC currently trades below corporate averages relative to UAFRS-based (Uniform) Earnings, with an 18.2x Uniform P/E. At these levels, the market is pricing in expectations for Uniform ROA to decline from 21% in 2018 to 19% in 2023, accompanied by 5% Uniform Asset growth going forward.

Meanwhile, analysts have bullish expectations for the firm, projecting Uniform ROA to improve to historical highs of 23% through 2020, accompanied by 6% Uniform Asset growth.

Historically, NOC has seen improving profitability. Uniform ROA ranged from 5%-7% from 2003 through 2008, before jumping to 16%-17% levels from 2011 to 2017, driven by continued divestments of underperforming parts of their business including TASC, Inc. and Huntington Ingalls Industries. Since then, Uniform ROA has expanded to a peak of 21% in 2018. Meanwhile, Uniform Asset growth has been positive in the last five years, ranging from 0%-15%, following a period of significant Uniform Asset shrinkage from 2006-2013.

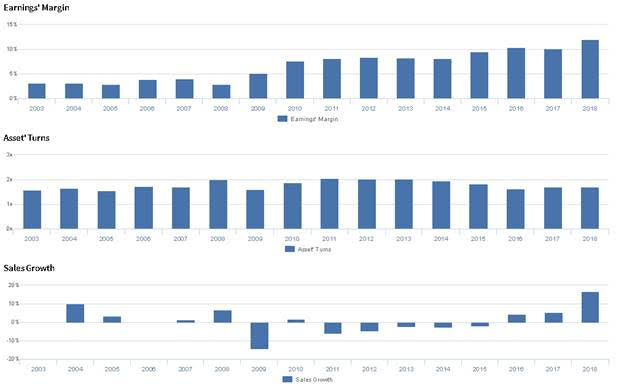

Performance Drivers – Sales, Margins, and Turns

Improvements in Uniform ROA have been driven by improving trends in Uniform Earnings Margin, offset slightly by declines in Uniform Asset Turns. Uniform Margins jumped from 3%-4% levels from 2003-2008 to 8% levels from 2010-2014, and have subsequently expanded to a peak of 12% in 2018. Meanwhile, Uniform Turns improved from 1.6x in 2003 to 1.9x-2.0x levels from 2008-2014, excluding 1.6x underperformance in 2009, before declining to 1.7x levels in 2017-2018. At current valuations, the market is pricing in expectations for Uniform Margins to regress to historical averages, accompanied by continued stability in Uniform Turns.

Earnings Call Forensics

Valens’ qualitative analysis of the firm’s Q3 2019 earnings call highlights that management is confident they are working towards maximizing revenue synergies and improving execution from their acquisition of Orbital ATK, and they are confident they will realize mid-single-digit sales growth in 2020. Furthermore, they are confident they have been working with the FTC to ensure compliance with their Orbital ATK transaction. However, they may lack confidence in their ability to sustain Flight Systems volume.

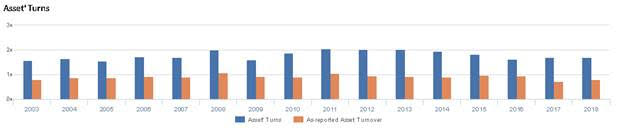

UAFRS VS As-Reported

Uniform Accounting metrics also highlight a significantly different fundamental picture for NOC than as-reported metrics reflect. As-reported metrics can lead investors to view a company to be dramatically stronger or weaker than real operating fundamentals highlight. Understanding where these distortions occur can help explain why market expectations for the company may be divergent.

As-reported metrics significantly understate NOC’s asset turns, one of the primary drivers of profitability. For example, as-reported Asset Turnover for NOC was 0.8x in 2018, less than half Uniform Asset Turns of 1.7x in the same year, making NOC appear to be a much weaker business than real economic metrics highlight. Moreover, as-reported turns have consistently been below Uniform Turns in each year since 2003, significantly distorting the market’s perception of the firm’s historical asset efficiency.

Today’s Tearsheet

Today’s tearsheet is for Honeywell International. Honeywell trades above market average valuations. The company has recently had 7% Uniform EPS growth. EPS growth is forecast to improve to 21% in 2019, and 12% in 2020. At current valuations, the market is pricing the company to see earnings grow by 9% a year going forward.

The company’s earnings growth is forecast to be above peers in 2019, but company is also trading well above peer average valuations. The company has slightly above corporate average returns, and no cash flow risk to their dividend.

Regards,

Joel Litman

Chief Investment Strategist