This railroad operator is silently riding a surge in demand to new heights

With demand surging across the U.S. on the heels of strong economic growth, businesses need to quickly restock dwindling inventories to keep up.

Throughout the pandemic, the U.S. railroad industry has demonstrated both its resilience and determination to help usher in supply to meet this demand. Yet, for one of the industry’s biggest names, as-reported metrics fail to show the results of recent efforts to enhance efficiency.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Tuesday Tearsheets

Powered by Valens Research

According to the Association of American railroads, which reports rail traffic volumes on a weekly basis, the back half of 2020 and beginning of 2021 have seen a historic recovery in volumes from the depths of the pandemic.

After dropping from around 525,000 carloads a week in the spring of 2019 to around 400,000 over the same period in 2020, volumes shot higher in the latter half of the year thanks to an impressive recovery in demand and companies struggling to keep up with orders.

This surge has now continued into 2021, with volumes largely tracking pre-pandemic levels for most of the past six months.

Yet, as supply chains remain disrupted, creating mismatches of supply and demand in many markets, railroads appear to be doing their part to keep inventory flowing.

A big reason for this resilience is the transformation of the U.S. railroad industry over the past ten years.

Due to consolidation and improvements in operational efficiency, the major players have become much leaner, with “operating ratios,” an industry-specific profitability gauge, improving materially as both fixed and variable costs come down.

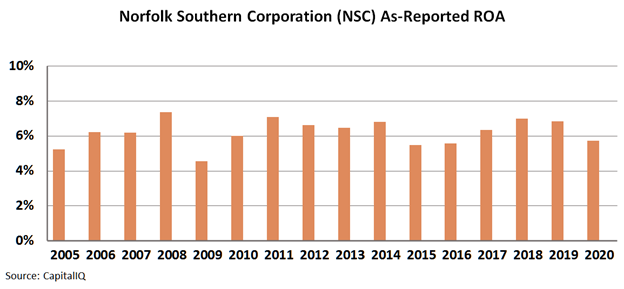

However, even with the recovery in demand and this relentless operational focus post-consolidation, as-reported ROA for Norfolk Southern Corporation (NSC), one of the industry’s biggest remaining players, does not appear to have improved at all over the past 15 years.

In fact, it appears the company’s profitability peaks and troughs remain exactly where they have always been, yielding zero discernable benefits from management’s efforts to improve the business.

In reality, this is only because as-reported metrics are woefully inaccurate and completely unreliable.

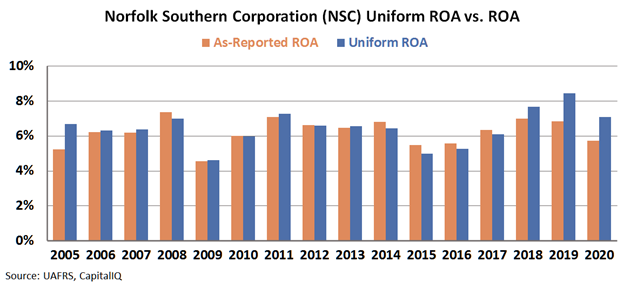

Looking at Uniform Accounting metrics, we can see that Norfolk Southern’s acceleration of operational efficiency initiatives has actually led ROA to reach new all-time highs.

For example, while as-reported metrics show a decline in profitability over the past 3 years, Uniform ROA actually increased from 8% in 2018 to 9% in 2019, and was really around 7% during the pandemic year of 2020, not 6%.

This illustrates how as-reported metrics often distort perceptions of a company’s profitability trends, leading to poor investment outcomes.

Even in the midst of a pandemic, Norfolk Southern has been able to leverage its increased efficiency to help keep the U.S. economy open. This is the kind of information investment theses are built on.

Investors should know the real story, not the fiction portrayed by GAAP.

SUMMARY and Norfolk Southern Corporation

As the Uniform Accounting tearsheet for Norfolk Southern Corporation (NSC:USA) highlights, the Uniform P/E trades at 23.0x, which is around the global corporate average of 23.7x and its historical average of 22.0x.

Moderate P/Es require moderate EPS growth to sustain them. That said, in the case of Norfolk Southern, the company has recently shown a 17% Uniform EPS decline.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Norfolk Southern’s Wall Street analyst-driven forecast is an EPS growth of 37% and 8% in 2021 and 2022, respectively..

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Norfolk Southern’s $258 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow 7% annually over the next three years. What Wall Street analysts expect for Norfolk Southern’s earnings growth is well above what the current stock market valuation requires through 2022.

Furthermore, the company’s earning power is 1x the corporate average. Also, cash flows and cash on hand are almost 2x above its total obligations—including debt maturities, capex maintenance, and dividends. This signals a low credit and dividend risk.

To conclude, Norfolk Southern’s Uniform earnings growth is in line with its peer averages and the company is also trading around its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research