Nuts and bolts are here to stay – Uniform Accounting reveals a surprising trend for this fastener giant

Innovation has led to the demise of many industries. From horse drawn carriages to typewriters, technology waits for nobody.

Looking at the as-reported numbers, today’s firm looks like the next victim of innovation and technological advancement. However, Uniform Accounting shows how it has been able to retain its position atop the fastener industry.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

When people think of innovation, they often think of it as being completely disruptive of existing industries. They picture new technologies replacing existing ones, leaving nothing behind.

Examples of this include the car wiping out the horse and buggy. Today, the horse and buggy is almost non-existent, while there are almost 1.5 billion cars globally.

The computer disrupted the typewriter industry in the same way. Computers were more efficient and could save documents virtually, eliminating the need for typewriters. Today, there are over 2 billion computers in the world.

Before Microsoft Excel, record keeping was done on printed spreadsheets. People no longer needed to keep track of data by hand, and instead opted for automated programs such as Excel.

While these inventions have all disrupted existing technology, some have had unintended effects as well. There have been surprise rebound functions, where demand for older products was actually amplified.

A good example of this is with the invention of the PDF. The PDF was invented in 1993 by Adobe (ADBE) to allow users to view and download documents online. It was supposed to wipe out paper from the office industry.

However, it had the opposite effect. The ease of use for PDFs led to it being printed en masse for distribution. Instead of remaining online, PDFs became the dominant file for printing, making it easier to print documents without ruining formatting.

This has led to more paper in the office, the opposite effect as intended.

Now, many people assume innovations in packaging, construction, and manufacturing will disrupt the fastener industry. Fasteners are devices that mechanically join two or more objects together.

Inventions like 3D printing may cause demand for fastener distributors to suffer. One of the largest fastener distributors is Fastenal (FAST). Fastenal is a global distributor of industrial and construction supplies, including fasteners like screws, nuts, and bolts.

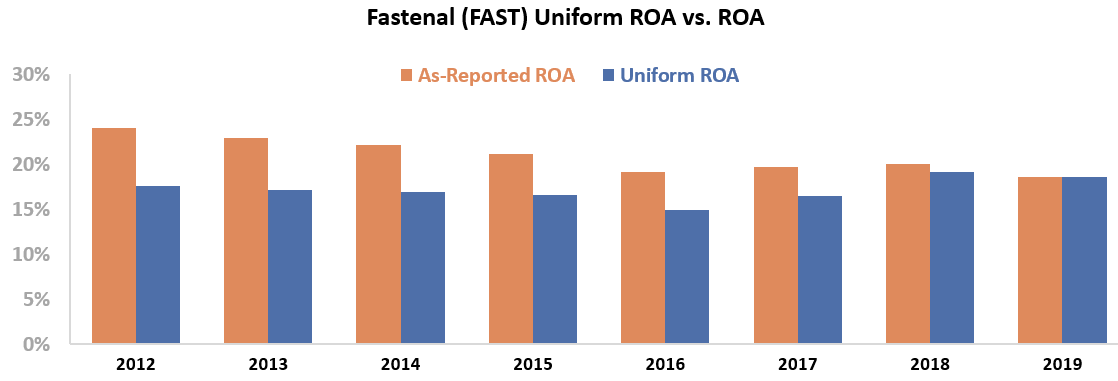

Looking at as-reported return on assets (ROA), Fastenal is a firm with declining returns.

As-reported ROA has fallen from a peak of 24% in 2012 to 19% in 2019. It appears as though the firm’s best days are behind it. New technologies such as 3D printing are entering the market and appear to be disrupting the fastener distribution industry.

However, this picture of Fastenal’s performance is not accurate. This is due to distortions in as-reported accounting, including the treatment of PP&E and other distortions. Wall Street has missed the mark on the strength of Fastenal’s returns.

Fastenal has not seen declines in recent years. Uniform ROA has grown slightly from 18% in 2012 to 19% in 2019.

Fastenal has been able to fend off new challengers and technology in the space to maintain returns.

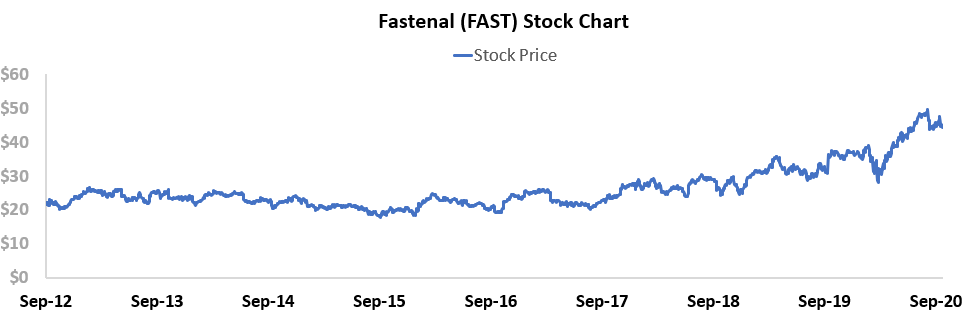

The company’s stock price has reflected the stability of returns as well. After a brief decrease in 2016, the stock price has been on a steady trend up to historical highs, minus the April pandemic crash.

Without Uniform Accounting, investors would be scratching their heads at this steady increase. They might assume the market has missed the rise of 3D printing, while in truth new technologies supplement Fastenal’s offerings.

As new technology has entered the market, Fastenal has been able to maintain its market position. Like many innovations before it, disruption doesn’t always mean existing industries are wiped out, and Uniform Accounting proves that’s the case for Fastenal.

SUMMARY and Fastenal Company Tearsheet

As the Uniform Accounting tearsheet for Fastenal Company (FAST:USA) highlights, the Uniform P/E trades at 30.5x, which is above the global corporate average valuation levels and its historical average valuations.

High P/Es require high EPS growth to sustain them. In the case of FAST, the company has recently shown a 4% growth in Uniform EPS.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, FAST’s Wall Street analyst-driven forecast is an EPS growth of 8% and 4% in 2020 and 2021, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify FAST’s $45 stock price. These are often referred to as market embedded expectations.

In order to justify current stock prices, the company would need to have Uniform earnings grow by 11% per year over the next three years. What Wall Street analysts expect for FAST’s earnings growth is below what the current stock market valuation requires in 2020 and 2021.

Furthermore, the company’s earning power is 3x corporate average. Also, cash flows are significantly higher than its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals low credit and dividend risk.

To conclude, FAST’s Uniform earnings growth is well above peer averages, and the company is trading above its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research