Oil prices have seen a drastic price shock…will the energy sector follow suit?

The past year has seen a rampant growth in inflation rates, with oil prices being hit hardest. Furthermore, the recent invasion of Russia into Ukraine has sent prices even higher. This means oil prices have breached $100 a barrel, hitting seven-year highs.

For those looking to get exposure to the energy sector as it experiences these tailwinds, the Energy Select Sector SPDR Fund (XLE) tracks the most prominent companies in the energy sector.

To better understand the upside and strength in this sector, let’s use Uniform Accounting to analyze the largest holdings in the ETF and answer a simple question—are the companies in the sector benefiting from the tailwinds seen in energy demand?

Also below, a detailed Uniform Accounting tearsheet of the fund’s largest holdings.

Investor Essentials Daily:

Friday Uniform Portfolio Analytics

Powered by Valens Research

In the past year, talk of inflation has filled the headlines.

Inflation shows up practically everywhere, and for many, it’s most tangible at the gas pump. As the price of gas goes up, inflation repeatedly stares people in the face as they fill up their tanks.

For the past half of a decade, oil has been relatively inexpensive. In 2014, the price of oil dropped below $100 per barrel and had remained there…until last week.

There are several reasons why this is happening.

Russia supplies more than 10% of the world’s oil, and with the country’s ongoing conflict with Ukraine, its supply has been impacted by bank sanctions. To make matters worse, OPEC is still refraining from adding capacity for the meantime and the global oil supply chain is beginning to feel the impacts of the oil constraints.

On the other hand, optimism about recovery in air travel, a huge consumer of oil, along with a broad economic recovery means demand for the commodity is rising.

Alongside the rising demand for oil, the energy sector is seeing tailwinds as the world opens up again. While there is merit on both sides of the debate over the long-term potential of the oil sector, the Energy Select Sector SPDR Fund (XLE) aims to track the energy sector.

As we see this surging demand for oil, now is a good opportunity to understand if the sector is a strong investment to make. To do so, let’s examine this fund through our Uniform Accounting lens.

Rather than track an entire benchmark, this fund tracks the energy sector within the S&P 500 index.

With the fund’s investments ranging across the largest oil companies like Exxon Mobil Corporation (XOM) and Chevron Corporation (CVX), it does a good job of covering the majority of the sector.

With so many companies in the fund, it can become difficult to understand which companies are actually poised to succeed compared to their market pricing.

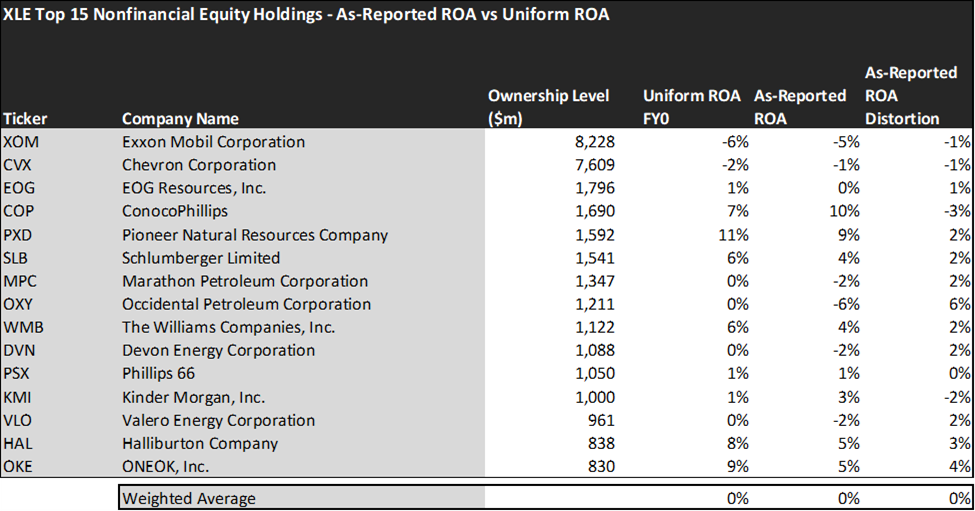

Economic productivity is massively misunderstood on Wall Street. This is reflected by the 130+ distortions in the Generally Accepted Accounting Principles (GAAP) that make as-reported results poor representations of real economic productivity.

These distortions include the poor capitalization of R&D, the use of goodwill and intangibles to inflate a company’s asset base, a poor understanding of one-off expense line items, as well as flawed acquisition accounting.

It is no surprise that once many of these distortions are accounted for, it becomes apparent which companies are in reality robustly profitable and which may not be as strong of an investment.

The average as-reported ROA among XLE’s top 15 names is a poor 0%, which doesn’t even come close to the average cost of capital in the market, and is in line with the Uniform ROA.

Exxon Mobil (XOM), for example, doesn’t return -5%. It actually provides poorer returns, at a -6% Uniform ROA.

Similarly, ConocoPhillips (COP) does not have 10% returns. Despite being a legacy firm with a high level of PP&E product line, it has a 7% Uniform ROA.

These dislocations demonstrate that some of these firms are in a weaker financial position than GAAP may make their books appear. But there is another crucial step in the search for alpha. Investors need to also find companies that are performing better than their valuations imply.

Valens has built a systematic process called Embedded Expectations Analysis to help investors get a sense of the future performance already baked into a company’s current stock price. Take a look:

This chart shows four interesting data points:

- The Uniform ROA FY0 represents the company’s current return on assets, which is a crucial benchmark for contextualizing expectations.

- The analyst-expected Uniform ROA represents what ROA is forecasted to look over the next two years. To get the ROA value, we take consensus Wall Street estimates and we convert them to the Uniform Accounting framework.

- The market-implied Uniform ROA is what the market thinks Uniform ROA is going to be in the three years following the analyst expectations, which for most companies here is 2023, 2024, and 2025. Here, we show the sort of economic productivity a company needs to achieve to justify its current stock price.

- The Uniform P/E is our measure of how expensive a company is relative to its Uniform earnings. For reference, average Uniform P/E across the investing universe is roughly 24x.

Embedded Expectations Analysis of XLE paints a clear picture of the fund. The stocks it tracks are pretty in line with expectations.

Just as analysts expected average ROA to increase from 0% to 7%, the market is pricing these companies to grow their economic profitability to 8%.

However, within this sector, there are companies that could beat the market’s expectations. A company like Pioneer Natural Resources Company (PXD), may be able to outperform expectations of earning barely market average returns.

Companies like ConocoPhillips can also create situations where investors may find themselves pleasantly surprised in the returns they end up achieving. With the market pricing in expectations of 9%, growing to analyst expectations of 10% would mean a slight future upside.

This just goes to show the importance of valuation in the investing process. Finding a strong industry is only half of the process. The other, just as important part, is attaching reasonable valuations to the companies and understanding which are the most fundamentally sound investments.

To see a list of companies that have great performance and stability also at attractive valuations, the Valens Conviction Long Idea List is the place to look. The conviction list is powered by the Valens database, which offers access to full Uniform Accounting metrics for thousands of companies.

Click here to get access.

Read on to see a detailed tearsheet of the largest holding in XLE.

SUMMARY and Exxon Mobil Corp. Tearsheet

As Energy Select Sector SPDR Fund’s largest individual stock holdings, we’re highlighting Exxon Mobil Corp’s (XOM:USA) tearsheet today.

As the Uniform Accounting tearsheet for Exxon Mobil Corp. highlights, its Uniform P/E trades at 19.3x, which is below the global corporate average of 24.0x, but around its historical average of 18.6x.

Low P/Es require low EPS growth to sustain them. In the case of Exxon Mobil, the company has recently shown a Uniform EPS decline of 559%.

Wall Street analysts provide stock and valuation recommendations that, in general, provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Exxon Mobil’s Wall Street analyst-driven forecast is for EPS to decline 177% in 2021 and grow by 13% in 2022.

Meanwhile, the company’s earning power is below the long-run corporate averages. However, cash flows and cash on hand are slightly above total obligations—including debt maturities and capex maintenance. Moreover, Exxon Mobil’s is 30bps above the risk-free rate. Together, these signal low dividend and credit risks.

Lastly, Exxon Mobil’s Uniform earnings growth is below its peer averages, but is trading in line with its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research