Oil prices have tanked, here’s why that may be a good thing

Oil prices have been falling fast, and many investors are concerned this is yet another factor driving us towards an economic recession.

That said, looking back through history, there’s no strong relationship between oil prices and recessions, and in fact, current oil prices may contribute to a speedy recovery.

Investor Essentials Daily:

The Monday Macro Report

Powered by Valens Research

Within the last two months, oil prices have come under attack on multiple fronts.

First, fears about a global economic slowdown linked to COVID-19 sent prices cratering as investors began predicting significantly lower demand for crude going forward.

In the following weeks, oil prices continued to struggle as major oil producers like OPEC and Russia have been in no rush to reach an agreement on production cuts.

The uncertainty around these factors have investors and oil companies worried. Some Wall Street analysts and American oil execs have expectations for oil to fall as low as $10-$20 before the end of the pandemic.

This in turn has driven investors to be increasingly concerned for the likelihood and scale of a potential recession.

However, our research suggests that this may be more of a logical leap than a logical progression.

Back in 2015, we published a letter touching on the significant drop in oil prices at the time. If you recall, investors thought the oil glut may be the end of the bull market.

In hindsight, that didn’t end up being the case, but it’s worth diving in to understand why.

Inherently, there’s no confirmed relationship between oil prices and recessions. We have seen oil prices drop during each of the last three recessions, but oil prices have also dropped many other times and that had nothing to do with recessions.

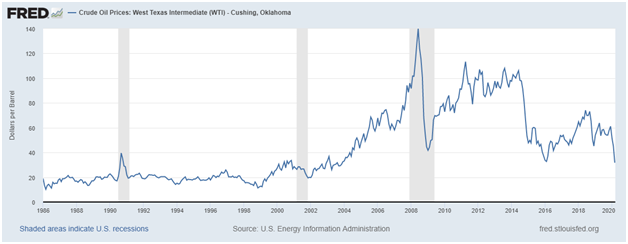

The chart below highlights oil prices over the last 30+ years overlaid with our last three domestic recessions.

As you can see, each recession saw somewhat of a fall in oil prices. That said, the impact was inconsistent.

In fact, despite a temporary surge and subsequent collapse in oil prices during the mild recession in the early 1990s, oil prices actually ended up higher after the recession than before.

Additionally, oil didn’t drop ahead of the dot-com bubble. In fact, it wasn’t until the very end of that recession that oil prices dropped.

Even in 2008, oil prices continued rising through the first half of the recession, meaning oil prices reached an all-time peak in the midst of a major recession.

Furthermore, we’ve seen several “false-positive” relationships between oil and a recession—with the biggest being the oil glut in 2014-2016.

Oil prices also dropped in 1996-1998, in late 2006, 2018, and other times, without a recession.

In 2014-2016, investors saw the massive fall in oil prices as a sign of an impending economic slowdown—lower prices indicated lower future demand, and it meant many oil companies may run into credit trouble if they have to shut off production.

We saw the oil glut differently—we saw it as a sign that oil prices were correcting and supporting a strong bull market.

You see, low oil prices are good for nearly every segment of the market except for the oil industry.

For the remainder, low oil prices have a stimulative effect on the economy. Companies that rely on oil as fuel are able to produce at lower costs, and can therefore spend more on growth.

Consumers, similarly, will have lower energy costs which encourages spending in other parts of the economy.

This time alone, for very unique reasons we’re probably already in a recession, but the drop in oil prices wasn’t a cause of a recession. If anything, it’s a very positive factor that will help fuel a strong economic recovery when the effects of the pandemic begin fading.

All the best, as always,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research