This company is helping evolve the continuum between advertising, consulting, and investment banking

Once upon a time, advertising, consulting, and investment banking all had clearly defined roles in servicing a corporation.

The below roles are overly simplistic, but approximately:

Advertising and marketing were about driving awareness of a brand, and getting customers engaged with brands, crafting customers perception of value of a business and brand, and driving customers to buy products.

Consulting companies worked with management to evolve a company’s strategy, crafting and at times implementing revenue generating and cost savings initiatives to unlock corporate value.

Investment Banking helped companies get access to capital to invest in growth, or to finance acquisitions, and to take a company to the market.

Three key areas that all companies need assistance, and all clearly defined. Realistically, there was limited reason for one to cross over to the others’ spheres. it wouldn’t be within their core competency.

That was true in the idyllic era of the 1950s, when shows like Mad Men painted a picture of the classic ad-man, and investment bankers could enjoy a liquid lunch before heading back to the office.

But over time, all three of these markets have evolved and started to merge. The needs of their business customers naturally evolved, and the lines between them started to gray.

Now, at the high end of the advertising world is brand consulting and consumer analytics to identify new markets a company could develop products into, and to understand consumer needs. This used to be the world solely of the management consultant.

Similarly, there is a massive wave of consolidation in the arena of digital agencies, as both consulting companies and advertising companies buy agencies in the space. These agencies are literally a bridge between advertising and consulting. They help clients with how to brand their company in the digital environment, clearly in the world of advertising. But they also help their clients develop apps, programs, and products and web design–the types of implementation initiatives that used to be the realm of a consulting company only. Now both advertising and consulting companies are building into this space.

The same is true in the space between consulting and investment banking. It used to be the role of a consultant to come in after an acquisition, and help work through synergies targets, and facilitate the integration in a merger, or to identify potential synergies before a merger. It was the role of the investment banker to value a transaction and help to raise the capital in a transaction.

Now consulting companies often are actively recommending to their clients potential transactions to undertake, modelling valuations and potential capital structure of a transaction. They are literally moving into the lower end of investment banking, where they are competing with advisory M&A shops, which are not focused on raising capital, but rather advising companies on their transactions.

As these worlds merge, companies that have not been stagnant, but willing to invest and evolve, are having great success. Consulting firms like Accenture (ACN) have been comfortable working in the gray area around their core business, and significantly outperformed the market while maintaining high returns while doing so.

One firm in the advertising space that has also been comfortable with this market fluidity has been Omnicom (OMC). Omnicom has made hundreds of investments over the past 20 years to help evolve with their market. And many of their acquisitions and investments in recent years have been with companies like Smart Digital, an AI driven digital agency that helps create products and evolve customer experiences with those products, among other initiatives, bluring the line between consulting implementation and advertising’s focus on understanding and motivating the customer. They’ve also acquired companies like MarketStar, a BPO firm that helps manage retail channel operations for companies, or Levo group, a digital transformation consultancy.

Omnicom is living and growing in that gray area and it has led the company to see returns expand massively over the past 5 years.

As an asset light advertising company, Omnicom has always had high Uniform ROA, with Uniform ROA around 75% in 2013-2014. However as they’ve accelerated their investment in these gray areas at the edge of advertising and consulting, and combined them with their core business, they’ve seen a massive inflection in Uniform ROA, with it rising to 420% last year.

The market sees that massive spike, and believes that both other advertising companies and consulting companies are going to start to focus on the same areas Omnicom has, pushing down its profitability.

But there are reasons to think the market may be being too pessimistic, as management is showing confidence about their competitive positioning, acquisition opportunities, and their margins, all areas that could lead to continued return stability, and even expansion.

Market expectations are for Uniform ROA regression, but management is confident about their competitive position, acquisition opportunities, and margins

OMC currently trades below corporate averages relative to UAFRS-based (Uniform) Earnings, with a 13.2x Uniform P/E. At these levels, the market is pricing in expectations for Uniform ROA to fall from 421% in 2018 to 344% levels in 2023, accompanied by 5% Uniform Asset shrinkage going forward.

Meanwhile, analysts have less bearish expectations, projecting Uniform ROA to only fall to 411% by 2020, accompanied by 3% Uniform Asset shrinkage.

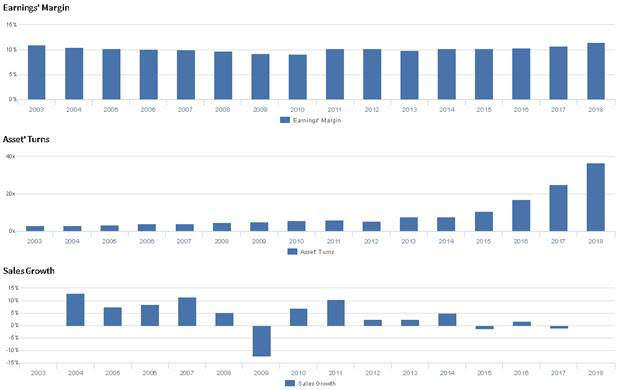

Historically, OMC has seen robust, improving profitability. After maintaining 32%-34% levels from 2003-2005, Uniform ROA steadily improved to 60% in 2011. However, Uniform ROA faded to 55% in 2012, before recovering to 74%-77% levels in 2013-2014, and has since expanded exponentially, to current peaks of 421%. Meanwhile, Uniform Asset growth has been largely negative, positive in just five of the past 16 years, while ranging from -19% to 18%, as the firm has consistently divested underperforming assets, boosting profitability levels.

Performance Drivers – Sales, Margins, and Turns

Uniform ROA expansion has been driven primarily by improvements in Uniform Asset Turns, coupled with stability in Uniform Earnings Margins. Uniform Turns steadily improved from 2.9x in 2003 to 5.9x in 2011, before falling to 5.4x in 2012, and rebounding to 7.5x levels in 2013-2014. Since then, Uniform Turns have expanded rapidly, reaching a peak of 36.5x in 2018, driven by the aforementioned divestitures. Meanwhile, after gradually fading from 11% in 2003 to a low of 9% in 2010, Uniform Margin stabilized at 10% through 2016, before improving to 12% in 2018. At current valuations, markets are pricing in expectations for Uniform Turns to regress from recent peaks, coupled with continued Uniform Margin stability.

Earnings Call Forensics

Valens’ qualitative analysis of the firm’s Q3 2019 earnings call highlights that management is confident they are in a very strong competitive position and that they remain focused on their key strategic objectives. Furthermore, they are confident they will continue to pursue attractive acquisition opportunities and that their capital allocation policy is as consistent as possible. Additionally, they are confident their EBIT for the Q3 2019 was $473mn and their operating margin grew to 13.1%.

However, management may be concerned about the sustainability of recent improvements on a non-GAAP basis, and they may be concerned about the impact of FX on their profitability. Moreover, they may lack confidence in their ability to sustain recent free cash flow generation, stock buybacks, and ROE levels. In addition, they may be concerned about their current debt levels, and they may lack confidence in their ability to deliver on their internal targets for 2019. Finally, they may be concerned about the value of their creative talent, and they may lack confidence in their ability to effectively integrate data into their creative process.

UAFRS VS As-Reported

Uniform Accounting metrics also highlight a significantly different fundamental picture for OMC than as-reported metrics reflect. As-reported metrics can lead investors to view a company to be dramatically stronger or weaker than real operating fundamentals highlight. Understanding where these distortions occur can help explain why market expectations for the company may be divergent.

As-reported metrics significantly understate OMC’s profitability. For example, as-reported ROA for OMC was just 5% in 2018, drastically lower than the historically high Uniform ROA of 421%, making OMC appear to be a much weaker business than real economic metrics highlight. Moreover, as-reported ROA has never exceeded corporate average levels, ranging from 5%-6% levels since 2003, while Uniform ROA has steadily expanded to the aforementioned peaks in 2018, misleading investors to believe the firm has seen muted profitability levels for over a decade.

Today’s Tearsheet

Today’s tearsheet is for Medtronic. Medtronic trades at a slight premium to market average valuations. The company has recently had robust Uniform EPS growth, though EPS growth is forecast to be slower going forward. At current valuations, the market is pricing in the company having slower earnings growth going forward than is forecast. The company’s earnings growth for 2019 is below peer average levels, but the company is trading at peer average valuations. The company has strong returns, with no risk to their dividend.

Regards,

Joel Litman

Chief Investment Strategist