ON Semiconductor may be worth a second look through the Uniform Accounting lens

The pandemic has ushered in a new wave of mass technological adoption, one which may only just be getting started.

One industry in particular is perhaps most important to supplying the components that will power this economy of the future, from the Internet of Things (“IoT”) to self-driving cars. Yet, as-reported metrics paint the picture of a space filled with cyclical, low-return businesses.

Today, we use Uniform Accounting to dive into one of the industry’s main players and discover whether or not this narrative holds true.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

We recently met with a long-term client of ours, a portfolio manager for one of the largest asset management firms in the world, to review their portfolio.

We noticed that one of their largest “risk” positions, i.e., a position with a much larger investment in an individual company than the relevant benchmark index, is a semiconductor firm.

If the stock performs well, it will have an outsized positive impact on performance relative to the benchmark, and inversely, an outsized negative impact if the name struggles.

It’s worth noting that market expectations for the firm were for significant return on asset (“ROA”) expansion, leading us into a discussion on how semiconductors are perpetually priced for an expansion cycle.

Thinking about where we are now, in the midst of a semiconductor cycle peak, we mentioned that increasing semiconductor capex could send the whole market lower.

Analysts with experience in the semiconductor space know that it’s typically a commodity industry, where the names generally exhibit long-term ROA trends around cost-of-capital levels. Looking at where we are in this particular cycle, the cratering only seems destined to happen for many companies…or so it appears when using as-reported metrics.

ON Semiconductor (ON), which makes semiconductor products that help manage power allocation and efficiency, may be an exception.

As more and more everyday items become integrated into the Internet of Things (“IoT”), they will require smarter management of power allocation and more capable sensors to derive insights.

These megatrends, which are just beginning in earnest, feed directly into impressive demand for well-positioned companies like ON Semiconductor. Yet, a glance at as-reported financial metrics appears to show the company not benefiting at all.

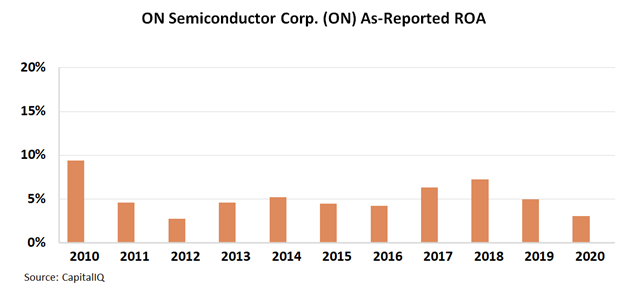

As the chart below makes clear, as-reported ROA peaked at 7% over the past decade and has regularly been at or below cost of capital levels, which average around 6%.

It looks like those excited about semiconductor companies at the heart of the IoT are bound to be disappointed…

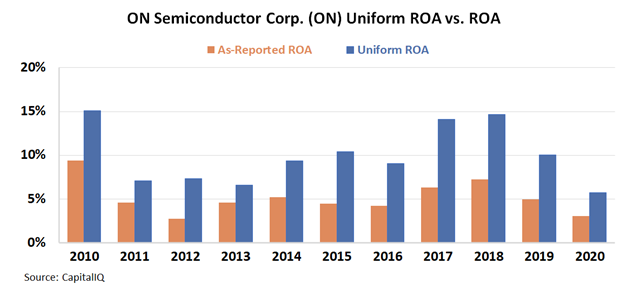

However, a closer look at economic reality with Uniform Accounting illustrates that ON Semiconductor’s Uniform ROA has actually been at or above 7% over the past 10 years regularly, even during parts of the cycle that were not especially great for the company’s end markets.

See for yourself below.

ON Semiconductor’s resilience, even during times of wild market swings in supply and demand, highlights that even names in a cyclical space can generate higher sustained returns if they deliver an advantage, an insight totally lost with GAAP metrics.

To be fair, ON Semiconductor isn’t the only semiconductor company that has been able to sustain such strong returns. There are many others, which should perhaps give pause to the perception that today’s semiconductor space is filled with cyclical, low return businesses.

If you want to take a look at some of ON Semiconductor’s competitors, such as Texas Instruments (TXN) and many others, click here if you are a subscriber, or here to sign up for a free trial today.

SUMMARY and ON Semiconductor Corp Tearsheet

As the Uniform Accounting tearsheet for ON Semiconductor Corp (ON:USA) highlights, the Uniform P/E trades at 20.8x, which is below the global corporate average of 24.3x but around ON Semiconductor’s historical P/E of 20.1x.

Low P/Es require low EPS growth to sustain them. In the case of ON Semiconductor, the company has recently shown a 52% Uniform EPS decline.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, ON Semiconductor’s Wall Street analyst-driven forecast is a 218% and a 19% EPS growth in 2021 and 2022, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify ON Semiconductor’s $49 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow 21% annually over the next three years. What Wall Street analysts expect for ON Semiconductor’s earnings growth is above what the current stock market valuation requires in 2021, but below that requirement in 2022.

Furthermore, ON Semiconductor’s earning power in 2020 is in line with the long-run corporate average. Moreover, Cash flows and cash on hand are at 180% of total obligations—including debt maturities and capex maintenance. All in all, this signals a moderate credit risk.

To conclude, the company’s Uniform earnings growth is above its peer averages. However, the company is trading below its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research