At-home healthcare is here to stay, and this company is leading the charge

As America continues aging, healthcare is becoming a bigger, and more important, industry.

The pandemic helped to highlight how much demand Americans have for at-home care, especially for the older generations.

Today’s company is set up to succeed as at-home care becomes a standard for late life care, and the credit rating agencies seem to be missing the bigger picture.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

As the American population continues aging, healthcare continues to be a high-growth industry.

While healthcare has always been a staple of American industry, the pandemic helped accelerate several trends within the healthcare market.

Specifically, various forms of at-home care gained a lot of traction in the last year. At-home care, which includes everything from telemedicine to at-home infusions, is often cheaper, faster, and it can be a more comfortable option for older folks.

At-home care makes healthcare far more flexible than it has ever been, and Americans are unlikely to give up that flexibility.

As a result, healthcare companies with at-home services like Option Care Health (OPCH) are going to see surging demand going forward.

Option’s infusion therapies help treat a lot of chronic conditions like immune deficiencies, psoriasis, and arthritis, making the company’s revenues fairly sticky. The pandemic opened Option up to an entirely new population of customers, meaning it’s likely to have higher cash flows going forward.

Despite this surge in demand for the company, rating agencies are still skittish when rating Option Care Health’s debt.

Specifically, S&P gives Option Care Health a highly speculative B rating, with the implied assumption of a 25%+ risk of default over the next five years.

Major rating agencies, including Moody’s, believe Option Care Health has a high chance of default over the next five years.

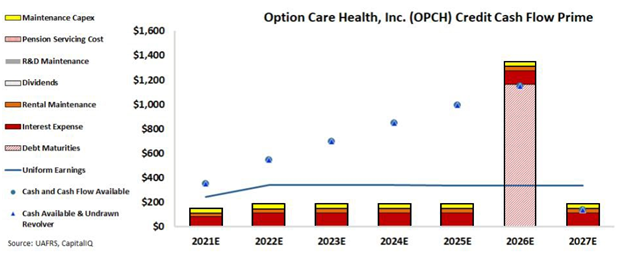

Our Credit Cash Flow Prime (CCFP) analysis is able to get to the heart of the firm’s true credit risk.

In the chart below, the stacked bars represent the firm’s obligations each year for the next five years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

As depicted, Option Care Health has massive cash liquidity and therefore should have no issues handling its obligations going forward. On top of this, even if the firm did not have access to this capital, cash flows alone exceed all obligations by a wide margin every year up until 2026, when the firm has material debt maturities.

Rather than a name in distress, Option Care Health is printing robust cash flows. This is why Moody’s B2 highly speculative rating, with a 25%+ risk of default expectation does not make sense.

Using the CCFP analysis, Valens rates Option Care Health as an investment grade IG3- rating. This rating corresponds with a default rate below 1% within the next five years, a more realistic projection once a holistic understanding of the company’s risk is taken into account.

Ultimately, Uniform Accounting and the Credit Cash Flow Prime analysis highlights how Option Care Health’s credit risk profile is much safer than what rating agencies believe.

SUMMARY and Option Care Health, Inc. Tearsheet

As the Uniform Accounting tearsheet for Option Care Health, Inc. (OPCH:USA) highlights, the Uniform P/E trades at 25.6x, which is around the global corporate average of 23.7x, but above its historical P/E of 20.8x.

Average P/Es require average EPS growth to sustain them. In the case of Option Care Health, the company has recently shown a 335% Uniform EPS shrinkage.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Option Care Health’s Wall Street analyst-driven forecast is a 64% and 43% EPS growth in 2021 and 2022, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Option Care Health’s $21.89 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow by 9% annually over the next three years. What Wall Street analysts expect for Option Care Health’s earnings growth is above what the current stock market valuation requires in 2021 and 2022.

Furthermore, the company’s earning power is 5x the corporate average. Also, cash flows and cash on hand are 2x above its total obligations—including debt maturities and capex maintenance. Together, this signals a low credit risk.

To conclude, Option Care Health’s Uniform earnings growth is above its peer averages, and the company is also trading above average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research