Our ‘management sentiment’ indicator gives pause to the market’s outlook

With the Q1 earnings season well underway, investors can see a widening gap between the earnings being reported and the movement of the stock prices.

This tells us how the market may already be pricing in a vision of perfection. To compare this to what management thinks, we can leverage our Earnings Call Forensics on an aggregate level.

Today, we will analyze what our Earnings Call Forensics data is telling us about the short-term volatility of the market

Investor Essentials Daily:

The Monday Macro Report

Powered by Valens Research

Analysts are getting a better handle on Q1 earnings and their outlook for the rest of the year with so much of the S&P 500 having reported results in the last few weeks.

While some analysts feared a sluggish recovery, the first quarter is shaping up to be a stellar one, especially for cyclical industries pressured last year.

Across industries like finance, healthcare, and consumer discretionary, management teams are delivering bullish surprises relative to analyst forecasts. Analysts were already pricing in a significant recovery for these sectors, so these “beats” go to highlight how much stronger earnings have been.

And yet, while all the earnings data and macroeconomic signals appear to be showing positive signals, the stock market itself doesn’t appear to be moving on this good news.

To see an example of this, we can zoom into the banking industry. Wall Street’s big banks all saw huge earnings beats, with Morgan Stanley (MS) shrugging off a $911 million overhang from the Archegos loss.

Despite these wins, the KBW bank index, which tracks these large financial institutions, fell during the week these earnings calls were going on.

At first, this seeming mismatch between earnings and stock price should leave investors scratching their heads. With a disconnect between a stock and the underlying cash flows anchoring its value, could pure fear or excitement be driving the market?

The reality is more complex. Stock prices change based on how the market’s expectations for a stock change. It is these forward-looking expectations that drive stock prices up or down.

Over the past few months, the market has seen a huge run up on the back of strong expectations. In other words, these robust earnings calls were already priced into the stock before the call itself, and investors are now focused on other issues that could pressure returns.

With a market already ready for a recovery, investors must make sure management teams are confident they can continue to deliver.

This means to invest in this market, investors need to know what management teams are thinking…

After the recent rally, investors are now dialing onto earnings calls expecting good news, not reacting to it. And aren’t going to be happy hearing anything that changes that narrative.

The way we get insight into what management teams across the market are really thinking is by leveraging our Earnings Call Forensics framework and tracking aggregate management confidence and concerns.

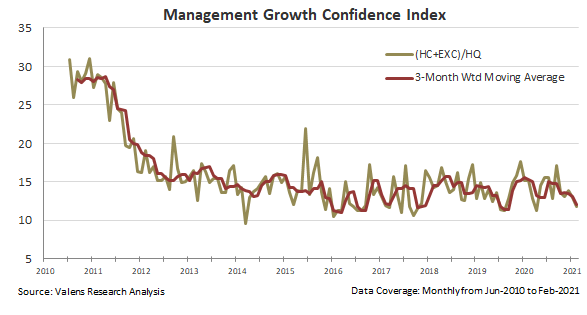

By gauging confident and concerned statements against each other, we can compile a Management Growth Confidence Index over time. We can track when management teams have confidence, generating Highly Confident (HC) and Excitement (EXC) markers. We can also see when management teams are more concerned and are holding back on their outlook, generating Highly Questionable (HQ) markers.

When management teams are more confident, they are more likely committed to investing in growth and see “fair winds and following seas” in the market. This means they will have more HC and EXC markers compared to HQ markers.

Meanwhile, if management is scared to invest, or sees market expectations exceeding their ability to deliver, more highly questionable markers appear in the earnings calls.

The recent disconnect between strong earnings calls and a weak stock market reaction starts to get explained when we look at what the Management Growth Confidence index has been showing us.

On an aggregate level, management sentiment isn’t nearly as bullish as it was in the back half of 2020, when management teams were flush with stimulus cash and saw multiple avenues for growth.

While markets are still pricing in a large potential for growth in the market, management teams’ confidence to deliver on these expectations is much closer to middle-of-the-road, or even a little more pessimistic than the past few years.

To be clear, this isn’t a reason to panic or short the market. The underlying credit profile of the market is still strong, which is a prerequisite for any protracted crash.

However, with this recent drop in management team confidence, investors shouldn’t expect a bull run such as the one in the back half of 2020 to carry into 2021. While the market is pricing in perfection, the next few months may be a little rockier as management teams push to deliver on these lofty expectations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research