An overly pessimistic credit market is hiding how safe this retailer’s debt actually is

Department stores have seen a slow, but steady decline in the past few years, due to a combination of strong competition and better pricing from big box retailers and a shift in consumer behavior.

Visits to physical stores have given way to a digitized shopping experience. Meanwhile, big box retailers like Walmart offer everything a department store chain can at better prices.

As a result, operators of brick-and-mortar stores like Macy’s (M) have been forced to undertake store closures and investments in better shopping experiences just to compete with rivals.

Macy’s initiated its turnaround plan in 2024 through a combination of store closures and investments in better shopper experiences. Fast forward to this year, the company is showing some signs that its turnaround is bearing fruit.

However, the market has placed a pessimistic view of its financial standing. But Uniform Accounting reveals a much more financially stable business underneath.

Investor Essentials Daily:

Friday News-based Update

Powered by Valens Research

For many years, department stores served as the backbone of America’s retail activity, with many Americans flocking to these places for products ranging from clothing to appliances and luxury items.

Today, these stores that were once considered as hubs of retail activity are now fading in the face of competition from big box retailers like Walmart and the shift from physical storefronts to online shopping.

As a result, the operators of these brick-and-mortar stores like Macy’s (M) have struggled to remain relevant.

Most of the shopping today can be done through digital storefronts and a few effortless swipes, making the trip to physical locations unnecessary and redundant. Meanwhile, big box retailers don’t just offer everything a department store does, but they’re also providing products to shoppers at significantly lower prices.

To make things worse, the pandemic, which shut down malls and other establishments, only hastened the decline of department store operators. And with post-pandemic inflation only worsening and forcing shoppers to spend less, the industry is facing strong headwinds.

That’s why last year, Macy’s, long-considered as one of America’s biggest and most recognizable department store chains, was forced to restructure and announce the closure of around a third of its stores.

Alongside closures, turnaround plans include the improvement of shopping experience and operations of its remaining stores. This also included attempts at gaining a share of the luxury market through the introduction of products from luxury brands like Prada.

A year later, it seems this turnaround attempt is bringing in some positive results. Moreover, the company has shown some resiliency in the face of the Trump administration’s policies by raising prices and working with suppliers to offset some of the tariff costs.

Macy’s recently announced during the third quarter of 2025 revenues of $4.91 billion, beating estimates by $350 million. The company raised its full-year sales guidance to a range of $21.48 billion to $21.63 billion, up from the previous range of $21.15 billion to $21.45 billion.

Despite beating estimates and raising guidance, the company has indicated a more cautionary outlook for the fourth quarter, stating it expects “a more choiceful” consumer in what’s historically been considered as retail’s best quarter.

This muted and more disciplined outlook reflects limited consumer spending brought about by cost pressures and tariff-induced price hikes.

While Macy’s is showing some signs of recovery, its stock still presents some risk for equity investors. However, this isn’t the case for credit investors who are looking for a compelling opportunity.

S&P has given Macy’s a BB+, or Non-investment Grade Speculative Rating. Said another way, the agency thinks there’s an 11% Macy’s defaults on its loans in the next five years.

While it’s expected that this business will no longer dominate the retail space like it once did, this outlook is too pessimistic.

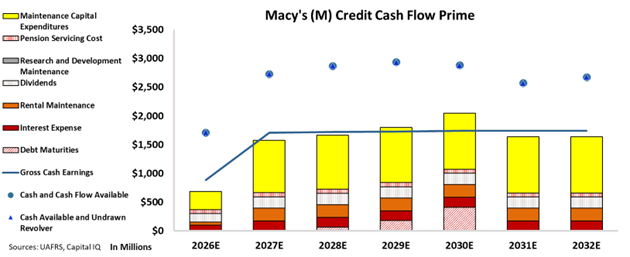

We can figure out if there is a real risk for this company by leveraging the Credit Cash Flow Prime (“CCFP”) to understand how the company’s obligations match against its cash and cash flows.

In the chart below, the stacked bars represent the firm’s obligations each year for the next five years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand available at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

The CCFP chart shows that Macy’s cash flows and available cash on hand are expected to be in excess of its financial obligations in the next five years, indicating it has more than enough to serve all its obligations going forward.

While Macy’s best years may be behind it, the market is placing an overly pessimistic view on its financial standing, positioning credit investors who see through this to take advantage of a stronger-than-expected survival story.

This isn’t a business in serious danger of defaulting on its debt in the coming years. This could be a compelling opportunity for creditors to capitalize on the market’s excessive concerns.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research