Penske is losing its car dealership battle

Car dealerships are some of the most dynamic small businesses in the American economy. They employ a lot of people, create wealth for their owners, and are amongst the biggest ad spenders on local stations.

However, the biggest automotive manufacturers such as Tesla (TSLA) and Ford (F) seem to be adopting the direct-to-customer channel instead of working with independent dealerships.

Being the second biggest car dealer in the US, Penske Automotive Group (PAG) is refusing to give in to this trend and continues to operate its more than 400 dealerships.

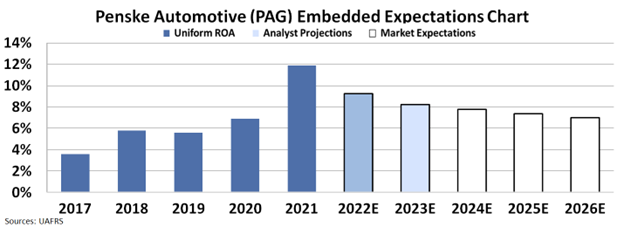

Even though the company enjoyed a short-term profitability surge in 2021, our Embedded Expectations Analysis (“EEA”) shows that the market is not pricing in the risk that the automotive retail model could be disrupted, making Peske a risky name for investors.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

One of the most fascinating parts of the American economy that no one really pays attention to is the local car dealerships.

These dealerships come in all shapes and sizes. You may see multi-story dealerships with hundreds of cars in stock in metropolitan areas or very small ones with only 5 cars available.

They are amongst the biggest ad spenders on local stations, they employ a lot of people in decent blue-collar jobs, and they create tremendous wealth for their owners.

Car dealerships paid a total of $100 billion in salaries to their 2 million employees in 2021 alone.

While these employees earn $50,000 on average per year, owners of the dealerships print money. The median salary of an owner is $91,000, but a tiny proportion earns as high as $495,000 per year.

These industries accelerate the velocity of money and power local American economies.

However, it seems some of the big players in the automotive industry are poking holes in the model and car dealerships are starting to lose their strong position in the market.

One of these players is Tesla (TSLA). The company operates more than 130 stores and sells directly to customers mainly through online stores.

It actually had several disputes with local dealerships as direct manufacturer auto sales are prohibited in many states. Tesla states that it cannot rely on independent dealerships to handle its sales because of the different electric motors its vehicles have.

Now, also Ford (F) is saying it is embracing the same way of sales for its electric vehicles. These might just be the first signs of the entire industry heading that way.

So, what are the companies that operate car dealerships going to do? Should they just pack their stuff and leave?

Penske Automotive Group (PAG) does want to give in. It operates more than 400 automotive and commercial truck dealerships in over 50 locations.

In 2019, the company was the second-biggest car dealer in the US in terms of total new retail vehicles.

Despite the direct-to-customer trend Tesla and Ford lead, Penske does not back away from its automotive retail business. In 2021, this business line generated 92% of its total revenue.

The market has noticed the strength of the dealership business through the car shortage. With the stock flat year-to-date compared to a market that has fallen 20%, it is important to see what future implications this valuation brings.

By utilizing our Embedded Expectations Analysis (“EEA”) framework, we can see what investors expect these companies to do at the current stock price.

The stock is currently priced at around $110, which means that the market is not pricing the company for the risk that its automotive retail model could be disrupted.

The company generated a Uniform ROA of around 5% for an entire decade and enjoyed a recent short-term surge in 2021, reaching 12%.

Now, however, the market is expecting returns over the next five years to be at 7%, higher than any year other than the unique 2021. Even without further pressure to the dealership model, these expectations are pricing in perfection already.

At current valuations, investors of the company might be set up for disappointment. If Penske cannot find a way to oppose the growing direct-to-customer sales trend and maintain current profitability, it looks like a name that investors should stay away from.

Without Uniform Accounting and our Embedded Expectations Analysis, the investors would not be able to see what the market is pricing in, and the recent short-term surge in profitability could have led to incorrect investment decisions.

SUMMARY and Penske Automotive Group, Inc. Tearsheet

As the Uniform Accounting tearsheet for Penske Automotive Group, Inc. (PAG:USA) highlights, the Uniform P/E trades at 15.9x, which is below the global corporate average of 19.7x, but around its own historical P/E of 16.5x.

Low P/Es require low EPS growth to sustain them. In the case of Penske, the company has recently shown a 118% growth in Uniform EPS.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Penske’s Wall Street analyst-driven forecast is a 3% and 11% EPS decline in 2022 and 2023, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Penske’s $110 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink by 8% annually over the next three years. What Wall Street analysts expect for Penske’s earnings growth is above what the current stock market valuation requires in 2022, but below its requirement in 2023.

Furthermore, the company’s earning power in 2021 is 2x the long-run corporate average. Moreover, cash flows and cash on hand are 2x its total obligations—including debt maturities, capex maintenance, and dividends. All in all, this signals low dividend and credit risk.

Lastly, Penske’s Uniform earnings growth is below its peer averages, but the company is trading near its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research