Paper product firms are thriving during the pandemic, but credit rating agencies have missed the memo

Some industries have thrived during the pandemic. One of the less surprising ones has been the paper and packaging industry. Increased demand for e-commerce and shipped goods, coupled with hoarding of paper products, has been a boon for the industry.

Today’s company is a paper products firm that has the credit markets concerned

Below, we show how Uniform Accounting restates financials for a clear credit profile. We also provide the equity tearsheet showing Uniform Accounting-based Performance and Valuation analysis of the company.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

As we talked about back in an April IED about the Manitowoc Company (MTW), people believe credit investors are smarter than equity investors.

However, credit investors would tell you the perception is not always accurate. They are smarter during a downturn, while equity investors thrive in upswings.

Credit investors are more risk-focused, so they fare better when the market is struggling. Bondholders are able to rely on a steady stream of interest payments and are first in line in the case of a bankruptcy.

Equity holders benefit from upswings because of tailwinds from increased spending, better earnings, and market sentiment. Stocks have unlimited upside whereas credit investors look for smaller and more stable cash flows.

This pandemic has been unique as investors have seen a downturn and market recovery all within 6 months. Both equity and credit investors have had the chance to thrive.

Toilet paper and tissue businesses as well have been thriving with constant demand during the pandemic. At the beginning of the quarantine, it was difficult to even find these items in stores.

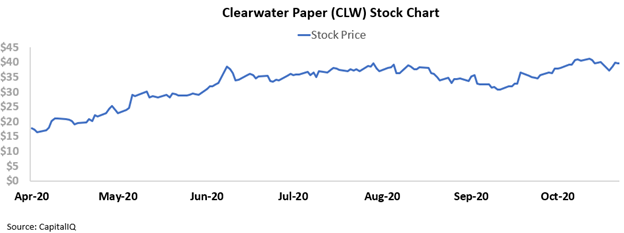

As such, Clearwater Paper (CLW) is having a field day from increased demand. Clearwater supplies private label tissue products to the big retail grocery chains.

Equity investors have caught onto the firm’s essential nature. The stock has risen from around $20 in late March to $40 levels currently.

However, Moody’s remains panicked about the firm’s credit, thinking it is a basic materials company. Basic materials are a cyclical business and are thus higher credit risks.

Moody’s rates the company with a high yield Ba2 rating but the firm had recently raised cash with a debt issuance, fortifying its liquidity.

Looking at the firm’s Credit Cash Flow Prime (CCFP) highlights the safety of the firm’s credit.

The firm’s cash flows should roughly match obligations until 2023. In addition, Clearwater has a sizable cash build and revolver capacity to meet obligations until 2025.

Clearwater’s robust 175% recovery rate and long runway should give the firm ample time to refinance.

Moody’s rates the firm as a speculative Ba2 investment. This would imply the firm is at a high risk of bankruptcy despite its strong liquidity position.

Factoring in its strong liquidity position and fundamental tailwinds, Valens rates Clearwater as a much safer crossover XO (Baa3) credit.

Ultimately, Clearwater is seen as a credit risk because rating agencies are looking at traditional metrics and misunderstanding the firm’s cash flows.

However, when looking at Clearwater’s CCFP from a Uniform Accounting perspective, the firm’s minimal credit risk can be seen. Additionally, the firm was able to weather the lockdowns in April and emerge with stronger liquidity.

Thus, the company is a safer credit risk than what Moody’s gives it credit for.

CLW’s Credit Merit a Ratings Upgrade Given the Firm’s Capex Flexibility

Credit markets are accurately stating credit risk with a YTW of 4.222% relative to an Intrinsic YTW of 4.052%, and an Intrinsic CDS of 371bps. Meanwhile, Moody’s is overstating risk, with its non-investment grade Ba2 rating two notches below Valens’ XO (equivalent to Baa3) rating.

Fundamental analysis highlights that CLW’s cash flows should fall short of servicing operating obligations in 2020-2021 due to coronavirus headwinds, before roughly matching them in each year going forward.

That said, the firm has significant liquidity after its recent debt issuance, which should allow it to service all obligations until it faces material debt headwalls in 2023 and beyond, giving it ample time to improve operations.

Additionally, CLW’s robust 175% recovery rate on unsecured debt should allow access to credit markets to refinance, albeit at potentially unfavorable rates given its poor market capitalization.

Incentives Dictate Behavior™ analysis highlights mostly positive signals for creditors. CLW’s management compensation framework should drive them to focus on improving all three value drivers: margins, top-line growth, and asset utilization, which should lead to Uniform ROA improvement and higher cash flows available for servicing obligations.

In addition, management members are not well-compensated in a change-in-control, indicating that they are unlikely to pursue a sale or accept a buyout of the firm, limiting event risk.

However, most management members are not material holders of CLW equity relative to their annual compensation, indicating that they may not be well-aligned with shareholders for long-term value creation.

Earnings Call Forensics™ of the firm’s Q2 2020 earnings call (8/4) highlights that management may lack confidence in their ReMagine brand of SBS folding card, their ability to deliver benefit through their Shelby investment, and the sustainability of the tissue business.

CLW’s capex flexibility and robust recovery rate indicate Moody’s is overstating the firm’s fundamental credit risk. As such, a ratings upgrade is likely going forward.

SUMMARY and Clearwater Paper Corporation Tearsheet

As the Uniform Accounting tearsheet for Clearwater Paper Corporation (CLW:USA) highlights, the company trades at a 25.0x Uniform P/E, which is around global corporate average valuation levels, but below its own historical average valuations.

Moderate P/Es require moderate growth to sustain them. That said, in the case of Clearwater, the company has recently shown a 218% Uniform EPS decline.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Clearwater’s Wall Street analyst-driven forecast projects a 340% and 85% EPS decline in 2020 and 2021, respectively.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Clearwater’s $39.68 stock price. These are often referred to as market embedded expectations.

The company needs to grow its Uniform earnings by 30% each year over the next three years to justify current prices. What Wall Street analysts expect for Clearwater’s earnings growth is far below what the current stock market valuation requires in 2020 and 2021.

Furthermore, the company’s earning power is below the corporate average, and cash flows and cash on hand are slightly below its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals moderate credit risk.

To conclude, Clearwater Paper Corporation’s Uniform earnings growth is well below peer averages, but the company is trading above its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research