Pfizer just made its biggest acquisition in years… let’s understand exactly why

Pfizer, along with the other large pharmaceutical companies, has long justified its sky-high drug prices on expensive R&D processes. Part of this cost is the company doesn’t run its own R&D, instead let small companies do the hard work before acquiring them.

Flush with cash after its successful COVID-19 treatments, combined with a series of expiring patents, Pfizer is on the hunt for its next blockbuster drug.

Today we are going to take a closer look at Biohaven, Pfizer’s largest acquisition since 2016, using our EEA tool to see if the price Pfizer is paying makes sense.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

Large pharmaceutical companies have long opposed legislation being considered by Congress to lower the prices of prescription drugs.

Their argument against such legislation has been based on the contention that reducing their revenues would reduce their investment in drug development and consequently discovering new medicines and treatments.

Congress has thus far resisted implementing such legislation, but it might be time to call into question why exactly drugs are so expensive.

One reason is because Pfizer (PFE) and the other big pharmaceutical companies aren’t good at start-up R&D. Instead, they let others do the hard work, and then acquire the technology for a premium when it is at a more mature stage.

The data backs up this claim as well.

An analysis of Pfizer in 2019 showed that they did not invent most of the drugs in their portfolio.

In fact, when we go back a few years, only 10 of Pfizer’s top 44 products in 2017 had the discovery and early research occur in-house. The other 70%+ of their portfolio was instead acquired from other companies.

With these acquired technologies accounting for 86% of their revenues, their claim that lowered prices would hamper in-house innovation starts making less sense.

As evidenced by its tremendous profitability over the years, it’s clear that Pfizer has done a good job of acquiring the right companies.

Thanks to over $32 billion in cash after its success with COVID-19 treatments and a series of patent cliffs in the portfolio nearing, Pfizer has been on the lookout for its next ticket to strong profitability.

This is why Pfizer just made a move on Biohaven for $11.6 billion, to acquire its blockbuster Remegepant drug.

While it appears that Pfizer paid a massive premium to the tune of a 79% premium over the closing price for the company, let’s use our Embedded Expectations Analysis to see if it’s a smart investment for Pfizer at the price it is paying and if it makes sense.

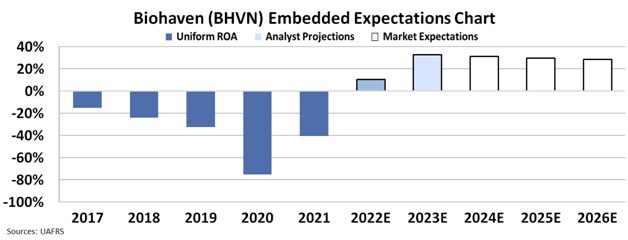

While we can see that Biohaven’s profitability has historically been strongly negative, analysts are predicting strong improvement as its drug moves to market.

If analyst expectations of 33% Uniform ROA in 2023 holds, embedded expectations of 29% at the $11.6 sale price makes it appear that Pfizer paid a reasonable rate for the company.

With Biohaven’s approved Remegepant, a potential migraine treatment blockbuster in the pipeline, Pfizer is on track to remain a massively profitable company by using its flush balance sheet on the right investments.

Investors relying on GAAP metrics to make financial decisions like this are constantly missing out on the true performance of companies across the market, making theme-based investing impossible. To learn more about how to gain access to the real numbers for almost 25,000 companies around the world, click here to read about our Uniform Accounting database.

SUMMARY and Pfizer Inc. Tearsheet

As the Uniform Accounting tearsheet for Pfizer Inc. (PFE:USA) highlights, the Uniform P/E trades at 6.7x, which is below the global corporate average of 20.6x as well as its own historical P/E of 10.3x.

Low P/Es require low EPS growth to sustain them. In the case of Pfizer, the company has recently shown a 149% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Pfizer’s Wall Street analyst-driven forecast is a 53% growth and a 35% EPS decline in 2022 and 2023, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Pfizer’s $54 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink by 15% annually over the next three years. What Wall Street analysts expect for Pfizer’s earnings growth is above what the current stock market valuation requires in 2022, but is below that requirement in 2023.

Furthermore, the company’s earning power in 2021 is 5x the long-run corporate average. Also, cash flows and cash on hand are over 3x its total obligations—including debt maturities, capex maintenance, and dividends. Overall, this signals low credit and dividend risk.

Lastly, Pfizer’s Uniform earnings growth is above its peer averages, but the company is trading below its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research