This company may just be the calm within the storm

As we anticipate a surge of investment for infrastructure development in the US, the increasing number of hurricanes and extreme weather makes infrastructure strength very important.

This will create a bigger market for products that can withstand bad weather.

PGT Industries (PGTI), a producer of impact-resistant products such as windows and doors, is well-positioned to capitalize on this trend.

Nonetheless, market sentiment raises doubts about increased competition in this space and expectations point to sales declines for PGT.

Also below, is the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

If you have been reading the Investor Essentials Daily, you might know about the supply chain supercycle. This is when companies improve their businesses by bringing parts of their supply chain closer to home.

It’s clear that spending this money will make businesses work better. But it is also important to spend on strong infrastructure, especially as the US faces more environmental challenges.

Big storms like Hurricane Harvey in 2017 caused $125 billion in damages. Hurricane Maria caused $90 billion in damages in the same year.

With increasingly more hurricanes and other extreme weather events in the last decade, the next decade is expected to be similar at best. That is why the US is now investing in its infrastructure to make it more resilient.

This includes making building parts such as windows and doors that are able to withstand impacts. PGT Industries (PGTI) specializes in this.

The demand for PGT’s products, like impact-resistant glass, is expected to increase a lot. This glass market is projected to grow 9% each year until 2028. The overall market for windows and doors is projected to grow 5% each year during this time.

After Hurricane Ian hit the southern coast in 2022, there was a big increase in orders for PGT in the southeast. The company is strongly positioned in Florida and is using a large network of dealers to capitalize on this growth.

We can already see the results…

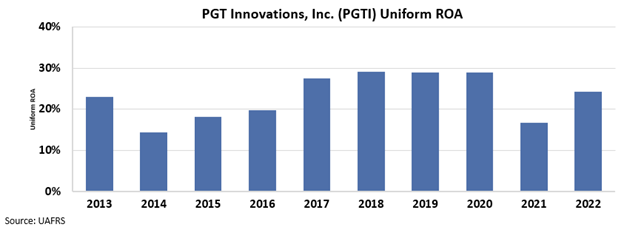

Although PGT had a down year in 2021, the Uniform ROA recovered quickly from 17% to 24% in 2022. This shows their strong sales in the southeast and a return to their usual performance levels.

PGT has proven to be both stable and resilient, but the market seems pessimistic for its future.

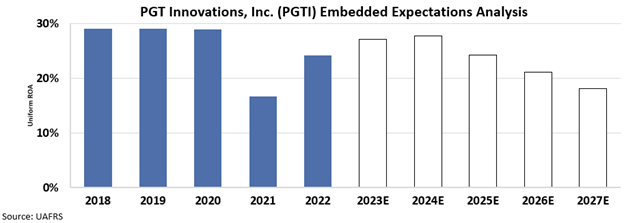

We can see what the market thinks through our Embedded Expectations Analysis (“EEA”) framework.

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

At the current stock price, the market expects the company’s ROA to fall to 11%, its lowest point since 2011.

The market is worried about PGT because of growing competition, especially from Tecnoglass (TGLS), which makes weather-resistant products at a lower cost.

The market thinks that this will make PGT’s sales fall to historic lows.

Overall, while not immune to competitive pressures, overall market growth will fuel growth for both companies.

SUMMARY and PGT Innovations, Inc. Tearsheet

As the Uniform Accounting tearsheet for PGT Innovations, Inc. (PGTI:USA) highlights, the Uniform P/E trades at 16.7x, which is below its global corporate average of 22.4x but above its historical P/E of 14.0x.

Average P/Es require average EPS growth to sustain them. In the case of PGT Innovations, the company has recently shown a 71% growth in Uniform EPS.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, PGT Innovations’ Wall Street analyst-driven forecast is a 19% and 10% EPS growth in 2023 and 2024, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify PGT Innovations’ $41.70 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to have immaterial growth annually over the next three years. What Wall Street analysts expect for PGT Innovations’ earnings growth is above what the current stock market valuation requires through 2024.

Furthermore, the company’s earning power is 4x its long-run corporate average. Moreover, cash flows and cash on hand are 3x its total obligations—including debt maturities, capex maintenance, and dividends. Also, the company’s intrinsic credit risk is 250bps above the risk-free rate.

All in all, this signals moderate credit risk.

Lastly, PGT Innovations’ Uniform earnings growth is above its peer averages but in line with its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research