This whole industry is cheap, but Uniform Accounting shows us which company is the real future winner

Last week, we talked about how sometimes whole industries are cheap, and that doesn’t make all of the names in it good investments.

This week, we found another cheap industry, but within it, there is a name that investors misunderstand. Combine cheap valuations, misunderstood financials, and management confidence, this is a name poised for a rebound.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Investor Essentials Daily:

Tuesday Tearsheets

Powered by Valens Research

Last week, we talked about the importance of looking for industry bias when screening.

In that note, we talked about how just looking at cheap valuations relative to the whole market can lead to unintentionally overweighting some industries, like auto suppliers.

We talked about how Lear Corporation (LEA) isn’t likely as great a value as it looks at first glance, and how simple valuation screens don’t always tell the full story.

Another industry that looks similarly, is the leisure products market. Companies like Brunswick (BC), Callaway Golf (ELY), and Malibu Boats (MBUU), for example, all look cheap right now.

The market is discounting these names, fearing that this is the end of the current economic cycle. When the economy starts to weaken, people are unlikely to go buy boats or golf as often.

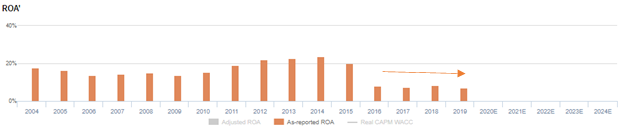

A poster child for this concern is Polaris Inc. (PII). The maker of off-road vehicles and snowmobiles, Polaris has already seen their profitability slip:

Since 2016, Polaris has seen as-reported ROA fall further, after an initial drop from peak levels, fading from already low 8% levels to historically low 7% levels in 2019. As profitability continues to fall, investors are likely concerned that the firm is in historically bad shape, and it is likely to get worse.

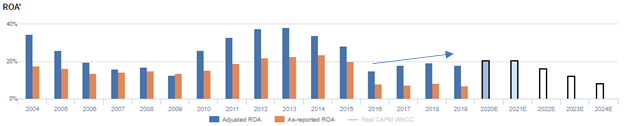

However, once all the adjustments under Uniform Accounting are made, a much less concerning picture is painted:

Rather than continuing to fall, Polaris has seen Uniform return on assets (ROA) actually rebound.

The firm is cyclical, there is no doubt. After seeing peaks in 2012-2013, profitability did compress. But since 2016, Uniform ROA is up from lows of 14%. After reaching cycle lows, Uniform ROA has been on the mend.

It’s possible the firm already went through its negative cycle, and is now recovering. However, the market is worried the business will never recover, a result of bad data.

As we eventually come out of this market cycle (and all of our macro signals say we will), this makes Polaris a potentially interesting name.

In addition, the management team was highly confident during their last earnings call, pointing to a strong foundation for the business coming out of the current market environment.

Specifically, confidence around their operating Cash flows and positioning point to a strong rebound when consumer confidence resumes.

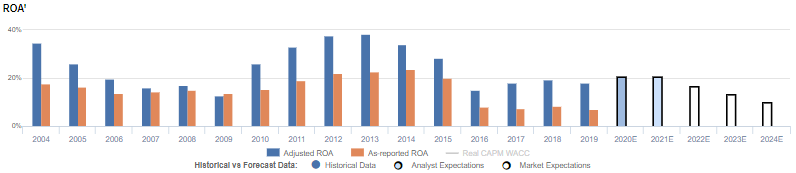

Polaris Inc. Embedded Expectations Analysis – Market expectations are for Uniform ROA to decline, but management is confident about their tariff mitigation, operating Cash flow, and positioning

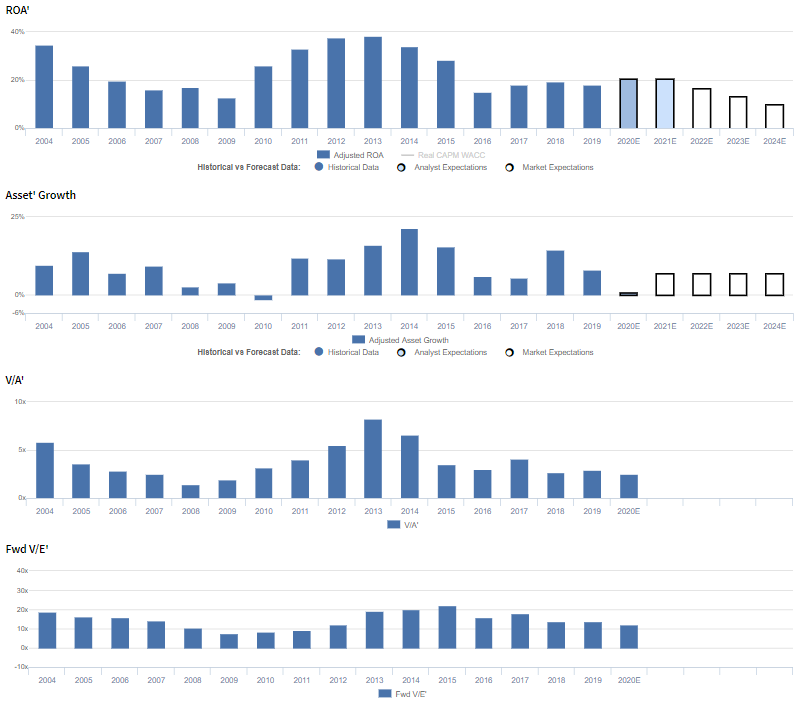

PII currently trades below recent averages relative to Uniform earnings, with a 9.2x Uniform P/E (Fwd V/E′).

At these levels, the market is pricing in expectations for Uniform ROA to decline from 18% in 2019 to 7% in 2024, accompanied by 7% Uniform asset growth.

However, analysts have less bearish expectations, projecting Uniform ROA to improve to 20% through 2021, accompanied by immaterial Uniform asset growth.

PII has historically seen cyclical profitability, with Uniform ROA fading from 35% in 2004 to a trough of 13% in 2009, before improving back to 38% in 2013.

Thereafter, Uniform ROA contracted to 15% in 2016 and expanded to 18%-19% levels in 2018-2019.

Meanwhile, Uniform asset growth has been strong, positive in fifteen of the past sixteen years, while ranging from -2% to 21%.

Performance Drivers – Sales, Margins, and Turns

Trends in Uniform ROA have been driven by compounding trends in Uniform earnings margin and Uniform asset turns.

After falling from 10% in 2004 to 7% levels in 2007-2009, Uniform earnings margins expanded to peak 13% levels to 2012-2013.

Subsequently, Uniform earnings margins fell sharply to 7%-8% levels in 2016 to 2019.

Meanwhile, Uniform asset turns, which remained stable at 3.1x-3.5x levels from 2004-2005, compressed to 1.8x in 2009 before improving to 2.9x in 2012-2013 and declining back to 2.5x in 2019.

At current valuations, markets are pricing in expectations for both Uniform earnings margins and asset turns to decline.

Earnings Call Forensics

Valens’ qualitative analysis of the firm’s Q3 2019 earnings call highlights that management is confident they have reduced the impact from tariffs by moving production out of China, and they are confident they are maintaining their position in the ATV market.

Furthermore, they are confident their operating Cash flow has improved 23% year-over-year.

However, management may lack confidence in their ability to improve their sales mix through promotions, and they may be concerned about motorcycle competition from European firms in North America.

Furthermore, they may be concerned about their ability to continue offsetting the impact of tariffs, and they may lack confidence in their ability to sustain recent growth through FTR sales.

UAFRS VS As-Reported.

Uniform Accounting metrics also highlight a significantly different fundamental picture for PII than as-reported metrics reflect..

As-reported metrics can lead investors to view a company to be dramatically stronger or weaker than real operating fundamentals highlight.

Understanding where these distortions occur can help explain why market expectations for the company may be divergent.

As-reported metrics significantly understate PII’s profitability.

For example, as-reported ROA for PII was near 7% levels in 2019, materially lower than Uniform ROA of 18%, making PII appear to be a weaker business than real economic metrics highlight.

Moreover, Uniform ROA rose from 15% in 2016 to 18% in 2019, while as-reported ROA has remained in the 7%-9% range over the same period, distorting investors’ perception of the firm’s recent profitability trends.

SUMMARY and Polaris Inc. Tearsheet

As the Uniform Accounting tearsheet for Polaris Inc. (PII) highlights, Uniform P/E trades at 9.2x, below corporate average valuation levels and its own recent history.

Low P/Es require low EPS growth to sustain them, and for Polaris, the company is required to shrink their EPS by 13% to support current multiples. Furthermore, the company has recently shown a 1% decline in Uniform EPS growth, which is above what is required.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Polaris’ Wall Street analyst-driven forecast is just 7% in 2020 and 11% 2021.

Based on current stock market valuations, we can back into the required earnings growth rate that would justify $49 per share. These are often referred to as market embedded expectations. In order to meet the current market valuation levels of Polaris, the company would have to have Uniform earnings shrink by 13% each year over the next three years.

However, what Wall Street analysts expect for Polaris’ earnings growth falls above what the current stock market valuation requires.

To conclude, Polaris’ Uniform earnings growth is above peer averages while only trading below peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research