PayPal may want to reconsider passing on this rumored acquisition target

Potential M&A rumors always make for great fanfare on Wall Street.

To get a sense of what a potential deal might actually look like, and whether the acquiring company is paying a fair price, investors need to understand the expectations the market is pricing in for the target.

Today, we’ll highlight one such rumor that has made its way around the street over the past few weeks. It’s a wrap-up that has the potential to reshape the e-commerce landscape and compete with some of the industry’s biggest players.

We’ll take a look at the target company through the lens of Uniform Accounting to see its real profitability, then apply our Embedded Expectations framework to get a better sense of what the market expects for the name going forward, and what that means for its potential acquirer.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

Late last month, rumors started to swirl around Wall Street that fintech giant PayPal (PYPL) was looking to acquire Pinterest (PINS), a $29 billion imagine-sharing and social media company.

The idea of acquiring Pinterest makes sense for PayPal from an operational perspective.

Many have often talked about how Pinterest, known for its idea sharing platform where people can find inspiration for anything from weeknight dinner ideas to home decor styles, can do a lot more to monetize its business.

For example, combining its trend-setting digital pin boards with a link to actual products, along with a way to conveniently pay for them through PayPal, could provide a fully integrated tool that could rival the likes of Etsy (ETSY), Amazon (AMZN), or even eBay (EBAY).

With the power of growing demand for trends as the catalyst, a Pinterst and PayPal combination could potentially unlock a new powerhouse in the e-commerce space.

While PayPal has since pushed back against rumors surrounding any potential deal, looking at what that acquisition would have meant, it is easy to see why many were so excited about the opportunity…and why PayPal may want to rethink its decision to pull back.

Thanks to the At-Home Revolution, which supercharged the use of Pinterest’s idea-sharing platforms as consumers sought to take up cooking or remodel their homes, the company saw a major inflection in profitability.

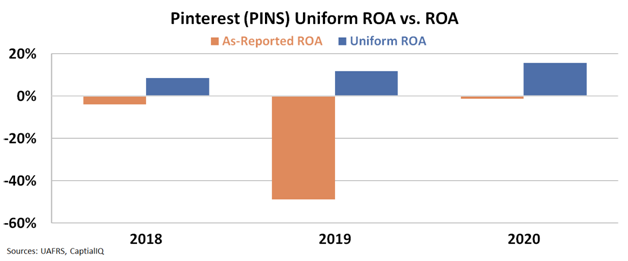

Contrary to as-reported metrics, which suggest Pinterest is still operating at a loss in 2020, Uniform Accounting highlights how its Uniform return on assets (“ROA”) actually jumped from 12% in 2019 to 16% in 2020.

See for yourself below.

At an estimated price tag of $45 billion, PayPal would have essentially been paying $70 a share for Pinterest. Even though substantially higher than its current stock price of $45, the purported deal appeared to understate the value of any potential synergies between the two companies.

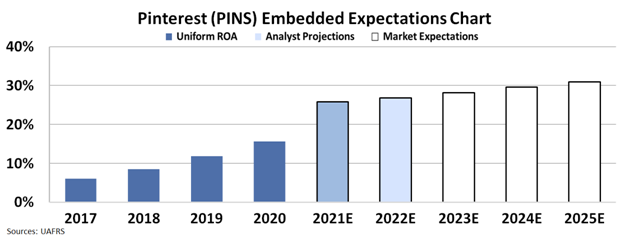

A quick look at our Embedded Expectations Analysis (“EEA”) highlights that going forward, Wall Street analysts are forecasting Uniform ROA to rise further to 26% this year. More importantly, the company has regularly grown more than 35% annually throughout its history.

At a stock price of $70, PayPal’s management team would essentially be betting that Pinterest’s Uniform ROA could rise modestly to 31%, accompanied by growth that would slow to only 25% a year going forward.

In the chart below, the dark blue bars represent Pinterest’s historical corporate performance levels in terms of ROA. The light blue bars are Wall Street analysts’ expectations for the next two years. Finally, the white bars are the “baked in” returns for Pinterest to be worth $70 a share.

All considered, this looks like a reasonable growth scenario for Pinterest even if it’s never integrated with PayPal’s payment processing systems.

This means that if PayPal does pursue a deal at some point in the future and can extract significant value from the business, there would be massive incremental synergy opportunities.

Using Uniform Accounting metrics and our Embedded Expectations framework to obtain insight into how the deal would play out, it becomes clear that PayPal may be missing out on an opportunity here.

SUMMARY and Pinterest, Inc.Tearsheet

As the Uniform Accounting tearsheet for Pinterest, Inc. (PINS:USA) highlights, the Uniform P/E trades at 36.0x, which is above the global corporate average of 24.3x and its own historical P/E of 31.2x.

High P/Es require high EPS growth to sustain them. In the case of Pinterest, the company has recently shown a 37% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Pinterest’s Wall Street analyst-driven forecast is a 97% and 42% EPS growth in 2021 and 2022, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Pinterest’s $46 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow by 38% annually over the next three years. What Wall Street analysts expect for Pinterest’s earnings growth is above what the current stock market valuation requires through 2022.

Furthermore, the company’s earning power in 2020 is 3x above the long-run corporate average. Moreover, cash flows and cash on hand are almost 7x its total obligations, signaling low credit risk.

Lastly, Pinterest’s Uniform earnings growth is above peer averages, while the company is trading below its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research