Pressure continues to mount for this embattled EV maker

Over a month ago, shares of luxury EV maker Lucid Group (LCID) plunged after failing to meet expectations despite reporting revenue growth.

Unfortunately, Lucid’s situation has gone from bad to worse as it recently announced workforce reduction measures which also included the removal of its COO.

Since its public debut in 2021, the company has failed to deliver positive returns. However, investors expect returns to inflect positively in the next few years.

Investor Essentials Daily:

Wednesday News-based Update

Powered by Valens Research

Over the past few years, the electric vehicle (“EV”) industry has experienced rapid growth due to technological advancements and a favorable regulatory environment.

As technology advanced, carmakers and investors poured billions of dollars into car manufacturers and pure-play EV firms in the hopes of capitalizing on the transition from internal combustion engines to EVs and hybrids.

This belief was further enforced by Biden-era regulatory mandates which incentivized the adoption of clean and low-carbon technologies. Unfortunately for the industry, the Trump administration did away with many Biden-era EV adoption mandates and subsidies last year.

And to make things worse, economic pressures have shrunk demand further. Data from Cox Automotive shows EV sales fell to 216,000 during the first quarter of 2026, a 27% year-over-year decline.

Said another way, EV sales are plummeting, putting tremendous pressure on EV makers like Lucid Group (LCID).

More than a month ago, the EV maker’s stock plunged after reporting its latest quarterly results.

While the company posted a 20% year-over-year increase in its revenue, the $282 million it posted fell far below the consensus estimates of $358 million. Moreover, the firm reported an operating loss of $989 million, far worse than Wall Street expectations of $864 million.

Management also announced the suspension of its production guidance for the year, citing the need for lowering its inventory of vehicles.

Since then, Lucid’s situation has only gone from bad to worse.

The EV maker recently announced that it would trim 18% of its U.S.-based workforce. In addition, the company removed the second shift of production at its flagship AMP-1 factory.

The headcount reduction is expected to be completed by the end of the third quarter.

But that’s not all. Marc Winterhoff, Lucid’s chief operating officer, also departed the company after the elimination of the COO role. According to company estimates, these job cuts could bring down costs by roughly $158 million annually.

Lucid’s shares are down by nearly 4% since its June 22 announcement.

Prior to the news of layoffs, Lucid had announced cuts to its production guidance for 2026.

Since going public in 2021 through a merger with a publicly traded special purpose acquisition company (“SPAC”), Lucid has consistently failed to deliver positive returns.

Lucid’s shares have fallen around 7% since releasing earnings on May 5.

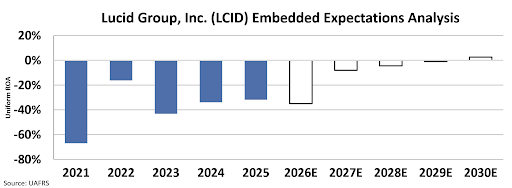

Since going public in 2021, Lucid has yet to generate positive returns. In 2025, the company’s Uniform return on assets (“ROA”) stood at -32%.

Tariff pressures and the expiration of Biden-era subsidies have continued to pressure this EV maker, making its already-expensive products even pricier.

Now, with inflation at 4% and consumer credit at nearly $19 trillion, Lucid’s luxury positioning is becoming increasingly unattractive to would-be buyers forced to cut spending to stay afloat.

Despite Lucid’s continued underperformance and inability to break through in the EV market, the market expects its returns to inflect positively in the next few years.

We can see this through Valens’ Embedded Expectations Analysis (“EEA”) framework.

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In other words, the EEA shows how well a company has to perform in the future to be worth what the market is paying for it today.

At current valuations, investors expect Lucid’s returns to inflect positively by 2030, reaching a Uniform ROA of 3%.

These expectations indicate the market expects Lucid to hit profitability within a few years.

However, given the current economic situation, industry headwinds, and the company’s failure to deliver positive returns thus far, that timeline could be far longer than anticipated.

Just like we said over a month ago, investors shouldn’t hold their breath for this stock.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research