Preventing losses is a key part of successful investing, and Uniform Accounting shows how this mutual fund does exactly that

The idea of margin of safety was popularized by value-investing legend, Benjamin Graham. Its application was further promoted by the famous investor, Warren Buffett, who stressed the importance of preventing losses.

Today’s fund has been around even before the idea of margin of safety was created and has been successful in applying these concepts to limit the fund’s losses.

In addition to examining the portfolio, we are including a deeper look into the fund’s largest current holding, providing you with the current Uniform Accounting Performance and Valuation Tearsheet for that company.

Investor Essentials Daily:

Friday Uniform Portfolio Analytics

Powered by Valens Research

Warren Buffett is arguably the most famous investor of all time. When Buffett speaks, people listen. He has simplified investing for many people through his easy to understand nuggets of wisdom.

One of his most famous phrases is his number one rule for investing. It is “The first rule of investing is never lose money. Rule number two is to never forget rule number one.” This statement is simple yet accurate.

Investors need to focus on the potential downside of a stock, not just on upside. If an investor buys a stock and it drops 50%, the investor doesn’t need to find a stock that will rise 50% to make back his money. He needs the stock to go up 100% just to recover the initial loss.

These 100% gains may be harder to find than the 50% downside companies.

This idea can be seen in the concept of “Margin of Safety,” a term coined by value investing grandfather Benjamin Graham in his 1934 book Security Analysis. The idea is to purchase companies whose price is below the “intrinsic value.” This creates a built-in cushion to protect against downside if the investor is wrong about the value of the stock.

The greater the margin of safety, the more room an investor has to be wrong and protect against downside risk. This concept ties back to Warren Buffett’s first rule of investing which is to never lose money.

One mutual fund that has been particularly successful in limiting downside is Dodge & Cox. The firm was founded in 1930 in the midst of the Great Depression. Dodge & Cox states it has a “razor sharp focus on capital preservation.” This likely stems from its inception during the worst financial crisis the United States has ever seen.

Dodge & Cox adheres to the ideas of value investing and buying companies with a margin of safety. It is particularly focused on Buffett’s first rule of investing, which is to never lose money.

Dodge & Cox’s Balanced Fund is one the most popular funds at the conservative asset manager, run by CEO Dana Emery. She has been at the helm for over 30 years, highlighting the firm’s commitment to a long-term outlook.

Dodge & Cox was able to avoid the worst of the dotcom bubble at the turn of the century due to its focus on capital preservation. While other funds rode the wave of new tech stocks, Dodge & Cox was content to limit its exposure to these trendy internet names. When the bubble burst, it was able to outperform the broader market due to its disciplined approach to limiting losses.

We wanted to take a look at the fund’s current holdings to see whether it is still investing in high quality company names with a healthy margin of safety.

Using as-reported metrics, it appears Dodge & Cox is investing in low-return businesses. Maybe investing in these safer companies means accepting names with reduced profitability.

However, using Uniform Accounting we can see the companies in the fund are actually much stronger after the accounting noise is removed.

See for yourself below.

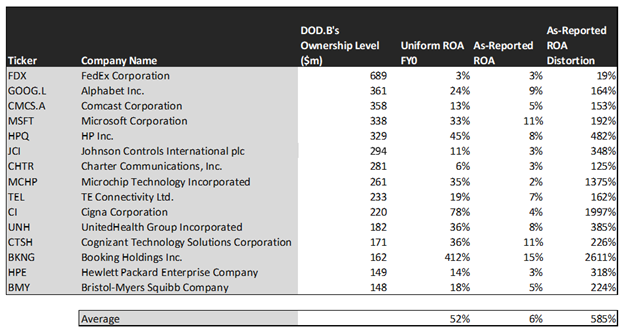

Looking at as-reported accounting, investors would think buying into Dodge & Cox Balanced Fund would lead to losing out on investment potential.

On an as-reported basis, many of these companies are below average performers with returns at 10% or below, with the average as-reported return on assets (ROA) right around 6%.

In reality, the average company in the index displays an impressive average Uniform ROA of 52%.

Once we make Uniform Accounting (UAFRS) adjustments to accurately calculate earning power, we can see the underlying strength of companies in the mutual fund.

Once the distortions from as-reported accounting are removed, we can see Microchip Technology (MCHP) does not have a return of 2%, but a sizable ROA of 35%.

Similarly, Booking Holding’s (BKNG) ROA is really 412%, not at 15%. While as-reported metrics are portraying the company as having average returns, Uniform Accounting shows the company’s truly robust operations.

The list goes on from there, for names ranging from Hewlett Packard (HPE) and United Health (UNH), to Cigna (CI) and Microsoft (MSFT).

If investors were to only look at as-reported metrics, they would assume limiting downside risk means exposure to low return businesses. In reality, these companies have huge returns.

Dodge & Cox isn’t just trying to buy high quality companies though. It’s trying to buy companies with a Margin of Safety, where the companies trade below their intrinsic value. Let’s see if it’s also buying companies where market expectations look too pessimistic.

This chart shows three interesting data points:

- The 2-year Uniform EPS growth represents what Uniform earnings growth is forecast to be over the next two years. The EPS number used is the value of when we take consensus Wall Street estimates and we convert them to the Uniform Accounting framework.

- The market expected Uniform EPS growth is what the market thinks Uniform earnings growth is going to be for the next two years. Here, we show by how much the company needs to grow Uniform earnings in the next 2 years to justify the current stock price of the company. If you’ve been reading our daily analyses and reports for a while, you’ll be familiar with the term embedded expectations. This is the market’s embedded expectations for Uniform earnings growth.

- The Uniform EPS growth spread is the spread between how much the company’s Uniform earnings could grow if the Uniform earnings estimates are right, and what the market expects Uniform earnings growth to be.

The average company in the U.S. is forecast to have 5% annual Uniform Accounting earnings growth over the next 2 years. These stocks are forecast by analysts to have no growth.

The market is slightly less optimistic, pricing these companies for a 1% shrinkage.

One example of a company with high growth potential is Johnson Controls (JCI). While the market expects Johnson to grow 4% over the next two years, analysts forecast the firm to see 46% growth over the same period.

Another company with similar dislocations is Charter Communications (CHTR). The company is forecast for Uniform EPS to grow by 42% a year, and the market is expecting the company to grow at just 9%.

That being said, there are some companies forecasted to have earnings growth less than market expectations. For these companies, like Comcast (CMCS.A), Booking Holdings, and Hewlett Packard, the market has growth expectations in excess of analysts’ predictions.

While some of the companies look mispriced, overall it doesn’t look like Dodge & Cox is buying mispriced companies, so much as companies with low market expectations, as seen by the low EPS growth expectations. Companies with low market expectations, if they also have low potential for growth, aren’t intrinsically undervalued, they’re just inexpensive.

Uniform Accounting appears to show that Dodge & Cox’s real success is identifying high quality, low risk businesses, as opposed to finding companies with a margin of safety of being intrinsically undervalued.

SUMMARY and FedEx Corporation Tearsheet

As one of Dodge & Cox Balanced Fund’s largest individual stock holding, we’re highlighting the tearsheet of FedEx Corporation (FDX) today.

As the Uniform Accounting tearsheet for FedEx highlights, the Uniform P/E trades at 26.9x, which is above global average valuation levels, but around its own historical average valuations.

High P/Es require high EPS growth to sustain them. In the case of FedEx, the company has recently shown a 60% Uniform EPS shrinkage.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, FedEx’s Wall Street analyst-driven forecast is a 128% and 6% Uniform EPS growth in 2021 and 2022, respectively.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify FedEx’s $284 stock price. These are often referred to as market embedded expectations.

The company needs Uniform earnings to grow by 19% each year over the next three years to justify current prices. What Wall Street analysts expect for FedEx’s earnings growth is above what the current stock market valuation requires in 2021, but below that requirement in 2022.

Furthermore, the company’s earning power is below the corporate average. However, cash flows and cash on hand are nearly 2x their total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals low credit and dividend risk.

To conclude, FedEx’s Uniform earnings growth is well above peer averages in 2021, and the company is trading above average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research