This pure play company is looking to keep on growing

Until the end of 2021, Vector Group (VGR) was a difficult company to understand with its tobacco and real estate business.

The two businesses lacked clear synergies. Seemingly recognizing this, the company divested its real estate division to focus exclusively on its tobacco operations. As a result, the company’s profitability skyrocketed in 2021.

The tobacco industry remains robust, largely unaffected by macro elements like interest rates, unlike the real estate sector. And Vector is growing within the tobacco industry, taking up market share day by day from the bigger players.

These support the idea that the high profitability we see is going to be sustained. However, the market thinks Vector’s returns will go down to what it was when the company had the real estate business, causing a mispricing.

Thus, Vector Group showed up on our screen. The company makes a great FA Alpha 50 name due to its potential for high returns and low expectations from the market.

Investor Essentials Daily:

Tuesday FA Alpha 50

Powered by Valens Research

One of the first things one learns in investing is that you should not bet on companies you don’t understand. And it is not easy to understand businesses.

Sometimes, businesses are as easy as purchasing raw materials, manufacturing a product, and selling. In other cases, it may get quite niche and technological, which is much more difficult.

And then there are those companies that have several different businesses. What they are doing is understandable, but why they are together is not. There are no clear synergies between them.

Vector Group (VGR) was such a company until the end of 2021. It had two businesses, one in real estate and the other in tobacco. And no, the real estate businesses did not own fields you can grow tobacco on. It was doing residential real estate brokerage.

The “group” was basically two independent companies. But this changed two years ago… The company sold its real estate business and is now all in on tobacco.

This made the business better in different ways. First of all, tobacco is a much more profitable business. The real estate business had many more assets dedicated to it and was barely generating operating profits.

Secondly, real estate is easily affected by macroeconomic factors such as interest rates. On the other hand, tobacco is less cyclical. Given the addictive nature of nicotine, consumers keep on purchasing tobacco products even during economic downturns.

This is what Vector Groups is now. It’s a pure-play, higher profitability tobacco company. It’s already the U.S.’ fourth largest cigarette producer, boasting a range of value brands like “Montego”, “Eagle 20’s”, and “Liggett”. And it’s still growing.

The company has witnessed consistent growth in its market share, hitting 5.6% nationally, a rise from 5.4% as of 2022’s end.

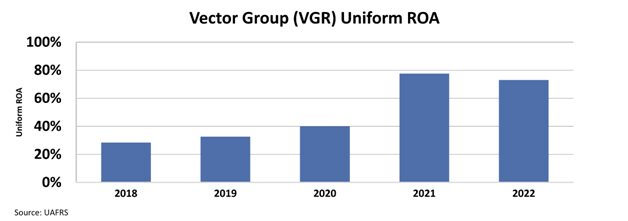

This transformation is clearly visible when you look at how the company’s Uniform return on assets (ROA) changed over the last few years.

It jumped from 40% in 2020 to 78% in 2021 and is now stable at around 73%. These are the highest profitability times the company has seen in the last 15 years.

The chart shows that the company performed incredibly well since it has become a pure-play tobacco company. As it continues to focus on Tobacco and grow its presence in the market, Vector should continue performing well.

And yet, the market fails to recognize this opportunity.

We can see this through our Embedded Expectations Analysis (“EEA”) framework.

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

At the current stock price, the market expects the company’s ROA to fall below 30%, thinking it is still the old company with real estate as its second business.

Given the company’s growing position in the stable tobacco industry and its exodus from real estate, these expectations seem overly pessimistic.

Vector has substantial potential to scale its operations and continue growing its market share in tobacco.

That is why Vector Group showed up on our screen. The company makes a great FA Alpha 50 name due to its potential for high returns and low expectations from the market.

Throughout financial market history, many of the world’s most successful investors have been candid in their belief that Generally Accepted Accounting Principles (“GAAP”) distort economic reality.

Warren Buffett, for example, once said investors should “concentrate on the world of companies, not arcane accounting mathematics.”

Investors who neglect the very real issues with as-reported accounting can find themselves caught up in investing with the crowd, blindly following hot “themes” without a thorough grasp of how to understand the businesses in question.

The only true way to focus on the “world of companies,” as Buffett suggests investors do, is to present a clear picture of how a business operates, something that can only be done by adjusting financial statements to reflect the arbitrary nature of certain accounting rules that leave much to discretion.

The world’s best investors understand the need to make these adjustments, which allows them to focus not on picking out the most popular companies but rather on looking for great names in sleepy areas that the market isn’t paying much attention to. From there, the goal is to then identify quality companies with significant growth potential at reasonable prices.

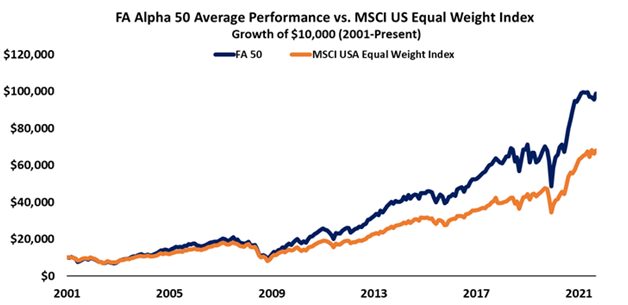

That’s exactly what we’ve set out to do with the FA Alpha, our monthly list of 50 companies that rank at the top for quality, high growth, and low valuations.

This list has outperformed the market by 300 basis points per year for over 20 years now, effectively doubling the performance of the market by focusing on the real fundamentals and valuations of companies with our proprietary Uniform Accounting framework.

See for yourself below.

To see the other 49 names on the list, click here.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research