The veil of GAAP accounting has real consequences for Qurate

Qurate may appear to be a sleepy, low-profitability retail business running the QGV retail channel. But in reality, it is an economic powerhouse that is concealed by bad GAAP accounting standards.

The consequence of this GAAP distortion is a strangely pessimistic Moody’s credit rating. Let’s use Uniform Accounting to put the company’s real profitability up against its obligations, and decide for ourselves if it is safe credit.

Also below, a detailed Uniform Accounting tearsheet of the company.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

Companies are constantly taking on debt to finance their operations. There are those that can take on debt sustainably, and those that wind up in bankruptcy proceedings.

There are fundamentally three reasons a leveraged company can sustain its load without going bankrupt.

First, the company has such strong cash flows relative to obligations (including debt maturities) that it will never realistically see a liquidity crunch.

Second, the company has such strong asset backing that creditors realize they will have no issues getting their money back by selling its assets in a default event. Hence, they are willing to let the company refinance debt over and over again.

Finally, the company has such a strong and steady return on assets (“ROA”) that creditors understand that it can lean on the profitability of its core business model even if it is constantly re-investing or pursuing aggressive growth strategies. So as long as the company’s operations cover its non-debt maturities, it should be able to allocate cash to repay its debts without issue.

The first feature is the holy grail that pretty much guarantees a company to be investment grade all of the time. The second and third features are also sturdy pillars to stand on, but credit rating agencies frequently don’t recognize it.

That is what separates the Valens credit analysis process from that of the major credit rating agencies. Our analysts use real data to soberly evaluate the most likely outcome for a company, and to then assign a rules-based grade.

When our team looked at Qurate (QRTE.A), we saw a surprisingly pessimistic Moody’s outlook.

Qurate operates QVC, the leader in televised home shopping, along with other shopping platforms like Zulilly and HSN. It has maintained robust 40% Uniform ROAs for years, and analysts don’t predict profitability to drop off in the near future.

But under GAAP accounting, Qurate seems like a fledgling business, with ROA’s hovering near the cost of capital. This just speaks to the importance of Uniform Accounting and the quality of input data before calculating financial ratios.

Moody’s, which relies on GAAP accounting, is rating the firm as a BB- credit, implying an 11% chance of default in the next five years.

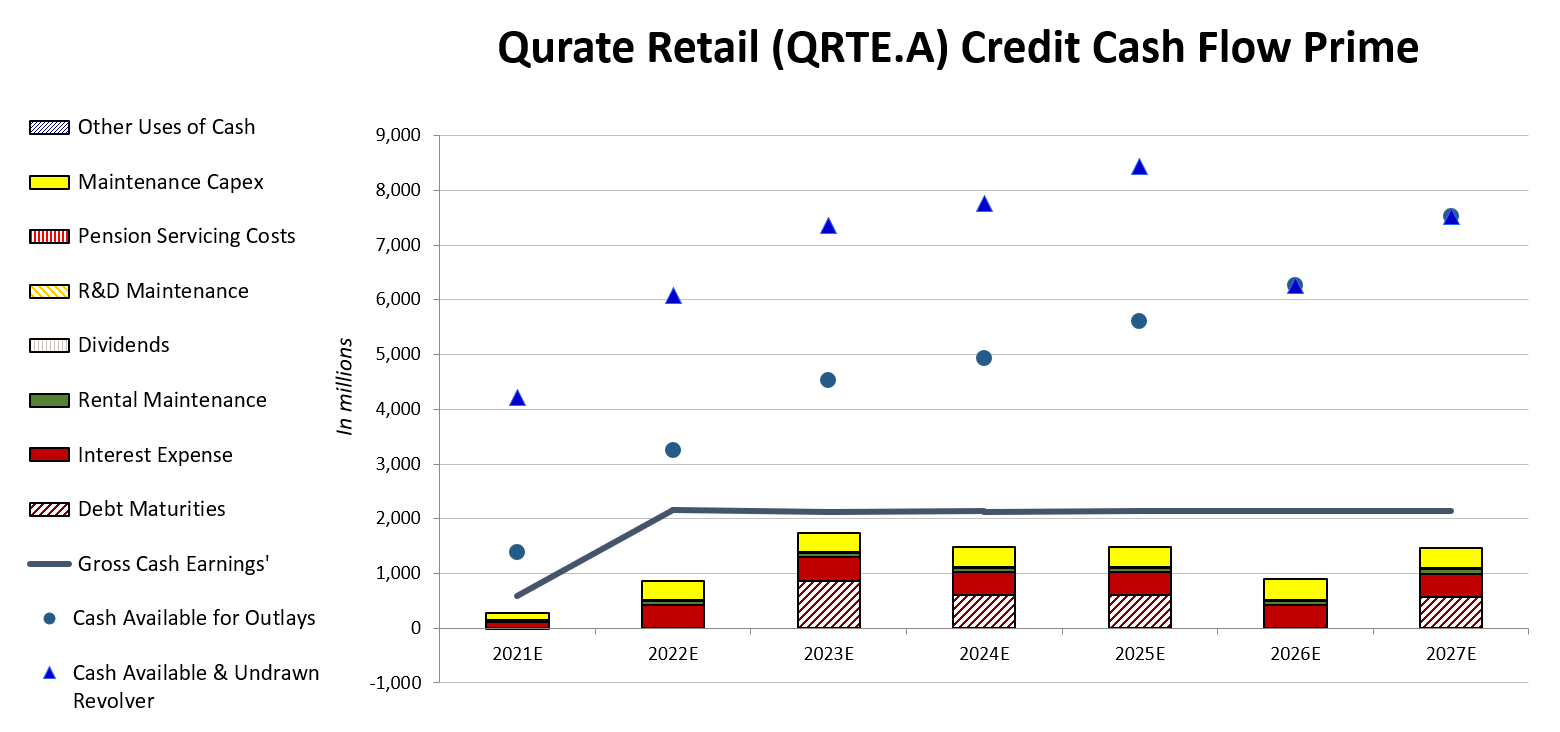

Let’s put the company to the test by examining it through the lens of Credit Cash Flow Prime.

In the chart below, the stacked bars represent the firm’s obligations each year for the next seven years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand available at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

Not only does Qurate have massive cash balances, but also cash flows that exceed operating obligations and debt maturities every year in the foreseeable future. Even when the firm will be repaying over a half billion in debt per year during 2023, 2024, and 2025, it may not need to touch its cash reserves due to its robust year-to-year profitability.

See for yourself:

Moody’s BB- credit rating isn’t reflective of Qurate’s credit worthiness, but the rating agencies’ blindness.

That’s why we rate Qurate as a much safer IG4+ investment grade credit.

Qurate is yet another company punished by an overly pessimistic credit rating. While we at Valens recognize the flaws with traditional credit ratings, many creditors do not. The BB- credit rating unfairly tarnishes Qurate’s public credit-worthiness, potentially making it harder for the firm to secure funding.

It is our goal to bring forward the real credit worthiness of companies, built on the back of better Uniform Accounting.

To see Credit Cash Flow Prime ratings for thousands of companies, click here to learn more about the various subscription options now available for the full Valens Database.

SUMMARY and Qurate Retail Inc. Tearsheet

As the Uniform Accounting tearsheet for Qurate Retail, Inc. (QRTE.A:USA) highlights, the Uniform P/E trades at 7.1x, which is below the global corporate average of 24.0x, but around its historical P/E of 7.7x.

Low P/Es require low EPS growth to sustain them. That said, in the case of Qurate, the company has recently shown a 3% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Qurate’s Wall Street analyst-driven forecast is for a 1% and a 3% EPS decline through 2022.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Qurate’s $8 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink by 21% over the next three years. What Wall Street analysts expect for Qurate’s earnings growth is above what the current stock market valuation requires through 2022.

Furthermore, the company’s earning power in 2020 is 7x the long-run corporate average. Moreover, cash flows and cash on hand are more than 2x its total obligations—including debt maturities, capex maintenance, and dividends. Additionally, intrinsic credit risk is 160bps above the risk-free rate. All in all, this signals a moderate credit risk.

Lastly, Qurate Retail’s Uniform earnings growth is in line with peer averages, and the company is also trading in line with its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research