Ryder Systems’ risks are being ignored by the rating agencies

The pandemic has undoubtedly turbocharged demand for e-commerce. But this pull forward in demand for online shopping also looks like it’s here to stay.

For logistics companies like Ryder Systems, one would assume this translates into sustained demand far into the future.

Yet, insourcing from powerful e-commerce players poses a threat to the business that Wall Street rating agencies seems to be casting aside. Today, we’ll use Uniform Accounting to get to the heart of Ryder’s true credit risk and decide whether Wall Street has gotten it wrong yet again.

Also below, a detailed Uniform Accounting tearsheet of the company.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

The At-Home Revolution has brought forward consumer demand shifts many experts didn’t believe would occur for another five or 10 years.

Lockdowns and other restrictions on economic activity early on in the pandemic practically forced consumers to adopt online shopping.

With retail shops closed, shoppers had few other options to buy the goods they needed to entertain themselves while couped up in their homes.

A consequence of this surge in e-commerce has been massive demand for logistics solutions in order to process and deliver all of these online orders.

This would appear to be a perfect environment for companies like Ryder Systems (R), one of the biggest suppliers of leased delivery vehicles in the U.S.

The company specializes in areas like fleet management and supply chain solutions, where it helps e-commerce providers get goods to customers quickly and efficiently.

However, Ryder is facing the difficult reality that many e-commerce companies like Amazon (AMZN) are bringing logistics services in-house.

Many one-time customers are now deciding they want to have more direct control over their supply chains, potentially leaving firms like Ryder out in the cold.

Despite this grim outlook, Wall Street rating agencies still view the company as a high-quality, investment grade credit.

We see things differently here at Valens.

Using our Credit Cash Flow Prime (“CCFP”) framework, we can get to the heart of Ryder’s true fundamental credit risk.

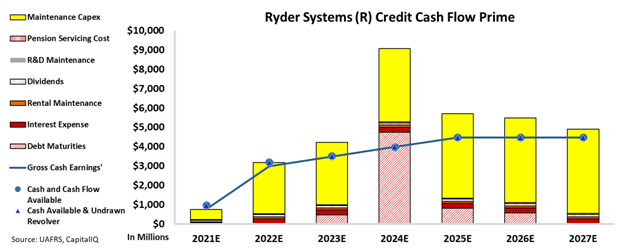

In the chart below, the stacked bars represent the firm’s obligations each year for the next seven years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand available at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

As you can see, Ryder has material debt maturities over the next several years, including $4.7 billion in 2024. More importantly, CCFP shows that the company also has significant maintenance capex spending needs as it has to consistently invest in new vehicles to sustain operations. These are obligations that cannot be cut or reduced.

Cash flows alone also don’t cover all of Ryder’s obligations unless the company can refinance its debt every year going forward. This means that if there is a liquidity event, Ryder may come under considerable pressure.

See for yourself.

Moody’s Baa2 investment grade rating for Ryder does not reflect reality. Instead it highlights Wall Street’s blindness to true credit risk.

That’s we rate the company as a much higher risk HY2 credit rating.

Using Uniform Accounting, we can see through the distortions of as-reported numbers to get to the true fundamental credit picture for risky companies like Ryder that are undergoing massive industry disruptions.

To see Credit Cash Flow Prime ratings for thousands of other companies we cover, click here to learn more about the various subscription options now available for the full Valens Database.

SUMMARY and Ryder System, Inc.Tearsheet

As the Uniform Accounting tearsheet for Ryder Systems, Inc. (R:USA) highlights, the Uniform P/E trades at 19.7x, which is below the global corporate average of 24.0x, but above its historical P/E of 17.5x.

Low P/Es require low EPS growth to sustain them. That said, in the case of Ryder, the company has recently shown a 6% Uniform EPS decline.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Ryder’s Wall Street analyst-driven forecast is for a 15% and 10% EPS shrinkage in 2021 and 2022, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Ryder’s $80 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink by 6% over the next three years. What Wall Street analysts expect for Ryder’s earnings growth is below what the current stock market valuation requires in 2021 and 2022.

Furthermore, the company’s earning power in 2020 is 1x the long-run corporate average. Moreover, cash flows and cash on hand are below its total obligations—including debt maturities, capex maintenance, and dividends. Additionally, intrinsic credit risk is 80bps above the risk-free rate. All in all, this signals a high credit and dividend risk.

Lastly, Ryder’s Uniform earnings growth is below peer averages, but the company is trading above average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research