Rating agencies miss the mark again by pegging this door maker as a risky homebuilder

The fortunes of the real estate industry have significantly improved since the Great Recession. Firms related to home renovations have fared especially well.

Today’s firm is a door maker that has credit markets concerned, despite having stronger operations than most investors realize.

Below, we show how Uniform Accounting restates financials for a clear credit profile. We also provide the equity tearsheet showing Uniform Accounting-based Performance and Valuation analysis of the company.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

When the housing market collapsed in 2008 and 2009, homebuilders struggled to stay afloat, with numerous bankruptcies rocking the industry. In the wake of the financial crisis, homebuilders and home suppliers started down the path of a long and tenuous recovery.

The real estate market came to a halt with monthly sales reaching a multi-decade low in 2009.

As a result, many people started to remodel and renovate their existing homes instead. During the Great Recession, many homes depreciated in value. Investments in homes were one way for people to rebuild equity.

The increased number of renovations provided a great boost for companies like Home Depot (HD) and Sherwin-Williams (SHW). Both companies had their stocks rise over 650% between 2010 and 2019.

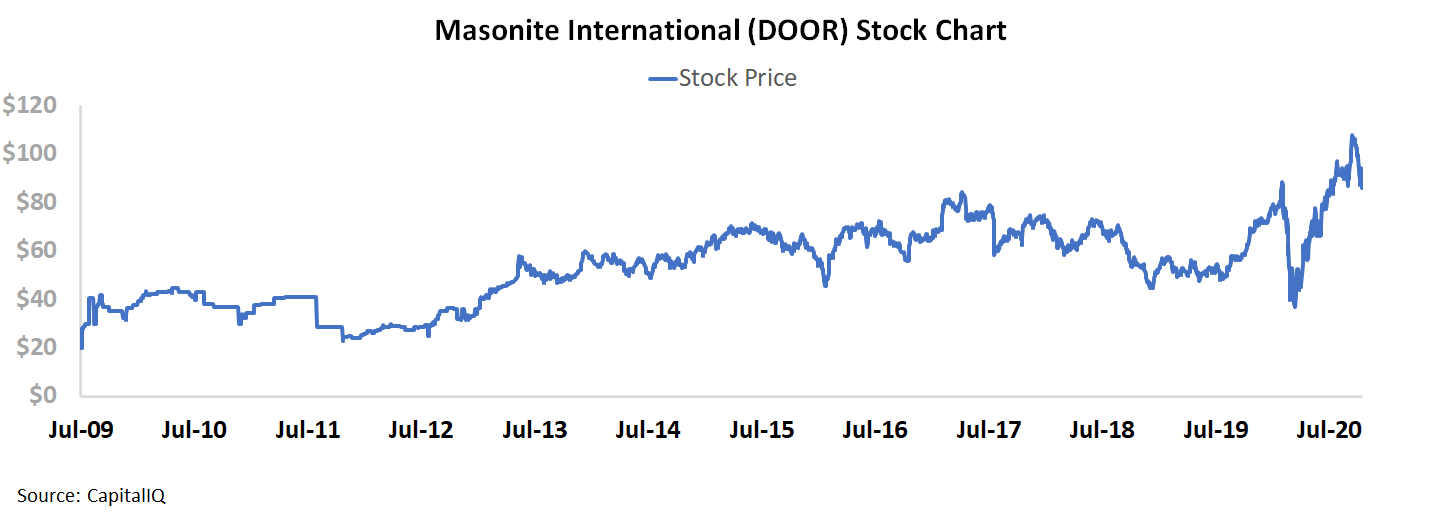

Another company aided by the trend was Masonite International (DOOR). Masonite builds interior and exterior doors across multiple brands including Premdor, Mohawk, Nicedor, and Graham-Maiman.

The majority of Masonite’s sales come from residential sales in the U.S. As a leader in the door industry, the company has always enjoyed healthy returns. Its Uniform ROA has consistently stayed above 10% and reached a high of 20% in 2017.

Equity markets noticed the firm’s profitability on the back of more home renovations. Since the firm initially went public in late 2009, the stock is up by more than 300%.

That said, credit rating agencies seem to be telling a different story. Moody’s has consistently rated Masonite as a high credit risk name.

This makes little sense, as Masonite has seen consistent cash flow through the post-recession environment. Now, the company should see business accelerate from the “At-Home Revolution”.

Looking at the firm’s Credit Cash Flow Prime (CCFP) highlights the safety of the firm’s credit.

Masonite does not have a debt maturity until 2026. Additionally, cash flows easily surpass obligations in every year until 2026. By that point, Masonite will have a sizable cash build, allowing the firm to meet all of its obligations.

Moody’s rates the firm as a speculative Ba2 investment. This implies the firm is at an elevated risk of bankruptcy, despite its minimal obligations, projected cash build, and stable cash flows.

Looking at the firm’s real obligations, Valens rates Masonite as a much safer IG3+ (A1) credit.

Masonite has the cash to meet all obligations through 2026 and will likely benefit from people renovating their homes as lockdowns continue.

Ultimately, Moody’s has been slow to react to Masonite. Consistent underperformance of the homebuilder market does not mean every firm in the industry is struggling. Looking at Masonite’s CCFP from a Uniform Accounting perspective shows the firm is actually at little risk of bankruptcy.

Ratings Agencies Materially Overstate DOOR’s Credit Risk Despite Healthy Cash Flows

Bond markets are slightly overstating credit risk, with a YTW of 2.952% relative to an Intrinsic YTW of 2.362% and an Intrinsic CDS of 199bps. Meanwhile, Moody’s is materially overstating the firm’s fundamental credit risk, with its Ba2 rating seven notches lower than Valens’ IG3+ (A1) rating.

Fundamental analysis highlights that DOOR’s cash flows alone should exceed operating obligations in each year going forward, and the firm has no material debt maturities until 2026, which the firm should be able to service with a significant expected cash build.

In addition, DOOR’s robust 100% recovery rate on unsecured debt should provide access to credit markets with favorable terms if it needs to refinance, despite its small market capitalization.

Incentives Dictate Behavior™ analysis highlights mixed signals for credit holders. DOOR’s management compensation framework should drive management to focus on margin expansion and top-line growth.

Moreover, management members do not have high change-in-control compensation, indicating they may not be incentivized to pursue a sale or accept a takeover of the firm, limiting event risk.

However, the lack of leverage and asset efficiency metrics in the framework may bias management to lever up or dramatically grow the asset base, which may limit Uniform ROA expansion and result in reduced cash flows.

Additionally, most NEOs are not material owners of DOOR equity relative to their average annual compensation, indicating management may not be well-aligned with shareholders for long-term value creation.

Earnings Call Forensics™ of the firm’s Q2 2020 earnings call (8/6) highlights that management is confident volume headwinds more than outweighed the positive impacts of pricing. Additionally, they appear concerned about their purchase of Lowe’s door fabrication assets and about their decision to resume investing in the business.

Furthermore, management may lack confidence in their ability to reverse recent revenue declines and they may be concerned about uncertainty in their end markets. Finally, they may be concerned about facility disruptions and the potential lag effect of weak housing starts.

Given the firm’s healthy cash flows relative to operating obligations and robust recovery rate, bond markets and Moody’s are overstating the firm’s fundamental credit risk. As such, both a ratings improvement and a tightening of bond spreads are likely going forward.

SUMMARY and Masonite International Corporation Tearsheet

As the Uniform Accounting tearsheet for Masonite International Corporation (DOOR) highlights, the company trades at a 13.5x Uniform P/E, which is below global corporate average valuations, but around its own historical average valuations.

Low P/Es require low EPS growth to sustain them. In the case of Masonite, the company has recently shown 5% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Masonite’s Wall Street analyst-driven forecast projects immaterial EPS decline in 2020 and 79% EPS growth in 2021.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Masonite’s $88.48 stock price. These are often referred to as market embedded expectations.

The company can have immaterial Uniform earnings shrinkage each year over the next three years and still justify current prices. What Wall Street analysts expect for Masonite’s earnings growth is in line with what the current stock market valuation requires in 2020, but above its requirement in 2021.

Furthermore, the company’s earning power is 2x the corporate average, while intrinsic credit risk is 260bps above the risk-free rate. Together, this signals moderate credit risk.

To conclude, Masonite’s Uniform earnings growth is well below peer averages, and the company is trading well below its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research