This restaurant giant is going to keep benefiting from high inflation

High inflation is delaying expected rate cuts by the Fed, impacting consumer spending and posing challenges to price stability.

Restaurant Brands International (QSR), with a diversified food portfolio including Burger King and Tim Hortons, benefits from inflation through higher prices and increased store counts, maintaining strong sales amid cost pressures.

The company’s strategy of price increases and international expansion has led to significant growth in return on assets (“ROA”), with market expectations for continued high performance.

Investor Essentials Daily:

Tuesday News-based Update

Powered by Valens Research

Yesterday we talked about how inflation is still high, and that is likely to delay the much-expected rate cuts by the Fed.

The latest Consumer Price Index (“CPI”) data from the Bureau of Labor Statistics revealed core inflation rose 3.2% in February on a year-over-year basis, remaining above the Fed’s 2% target and reinforcing expectations for ongoing rate hikes.

Higher inflation erodes consumer purchasing power and spending. It also poses major challenges for the Fed in guiding price stability.

As a result, Fed officials have signaled that their commitment to fighting inflation is “unconditional” and rates will likely remain higher for longer.

We mentioned how insurance companies can benefit from the persistent high inflation. There is another winner that is going to benefit from high inflation…

Restaurant Brands International (QSR). It is the operator of Burger King, Popeyes, Tim Hortons, and Firehouse Subs brands, which gives the company a very diversified food portfolio.

Restaurant Brands is benefiting a lot from inflation (higher unit prices) and continues to grow its store count simultaneously.

Even though prices are increasing at Restaurant Brands and other restaurants, customers still don’t have a better option than these quick-service brands, as the more expensive food from full-service restaurants gets even more expensive.

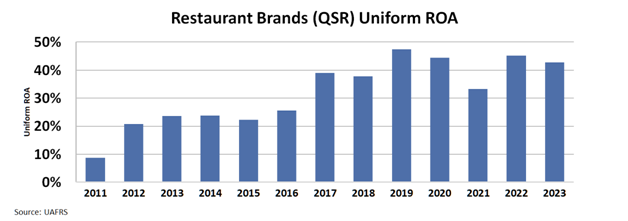

That is why 2022 and 2023 were great years for Restaurant Brands’s Uniform return on assets (‘‘ROA’’).

Take a look…

As inflation remains above historical numbers, Restaurant Brands can continue to record higher ROA.

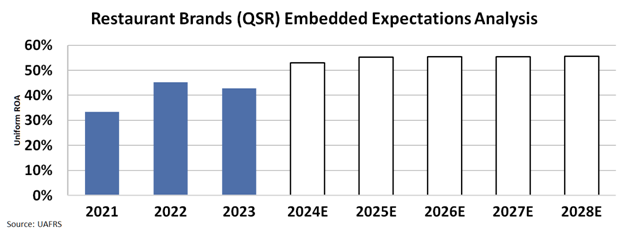

We can see what the market thinks through our Embedded Expectations Analysis (“EEA”) framework.

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

At the current stock price, the market expects the company’s ROA to rise to around 55%.

Restaurant Brands has effectively used pricing increases to pass on higher costs to customers while still maintaining strong sales volumes.

Between 2021-2023, the company implemented multiple rounds of modest price hikes across its brands. This allowed Restaurant Brands to grow its average unit volumes and net restaurant growth even in the face of inflation.

A big part of Restaurant Brands’s strategy involves expanding its global footprint, especially in emerging markets with large populations like Asia and Latin America.

The company’s international business has grown steadily in the last two years and partly offset cost pressures back home.

As long as inflation persists, quick-service restaurants like those owned and operated by Restaurant Brands look set to continue extracting higher prices from customers and growing their profits accordingly.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research