This company is a one-stop shop for the Supply Chain Super Cycle

We’re in the early innings of the supply-chain supercycle. When companies and the government have spare cash, they’re finally starting to invest in our supply chains and infrastructure after a decade of underinvestment.

This means we are building bridges, roads, and facilities all around the U.S. and bringing electricity and internet to underserved areas.

All these investments need various metals, which is what Ryerson Holding (RYI) provides. The company has already benefited from increased demand and is poised to ride the wave as investments ramp up.

However, the market is overly pessimistic about the future of the business, causing mispricing in the market.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

COVID-19 opened our eyes to how inadequate our supply chains and infrastructure are.

Because of the decade-plus of underinvestment in these spaces, a disruption like the pandemic caused lead times to get extended, some orders to get canceled, and manufacturers to have difficulties reaching raw materials.

Now though, the U.S. government and companies are working together to improve the situation. We are finally investing in our infrastructure.

We call this the supply-chain supercycle…

This means we are building bridges, repairing roads and rails, renewing facilities, and bringing services like electricity and internet to underserved areas.

The Bipartisan Infrastructure Law that came into effect in late 2021 helped fund nearly $185 billion worth of projects in its first year.

While the government works on implementing bills, companies are determined to bring their manufacturing facilities home and “reshore”.

They are foregoing low operational costs they could achieve in their facilities in Asia to be closer to the customer and improve supply chains.

All these investments require certain supplies. We talked about how one needs cranes to build. The other, and maybe more, needed things are various metals.

This is where Ryerson Holding (RYI) comes into the picture. The company supplies both steel that is used in all kinds of facilities, and aluminum which is an essential commodity for making wires.

We talked about how important, but underappreciated, aluminum is in a recent article, especially for green projects. We need a lot of wires to connect places that consume energy like the Northeastern part of the U.S., to places that actually produce it.

Northeastern part of the U.S., to places that actually produce it. Electrical wiring makes up 10% to 15% of total aluminum use globally. Ryerson is likely to see a surge in demand for aluminum from green projects like it has already seen for steel from facilities.

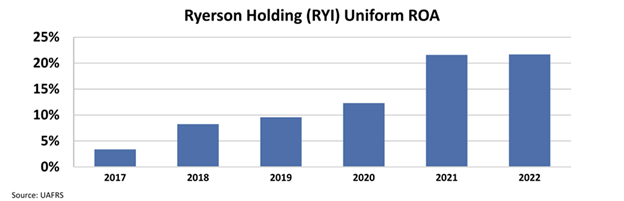

This increased demand meant higher profitability for the company. Its Uniform return on assets (“ROA”) surged from below 4% in 2017 to 22% in 2022.

This story sounds like a compelling investment opportunity. However, we need to understand what the market thinks before coming to a conclusion.

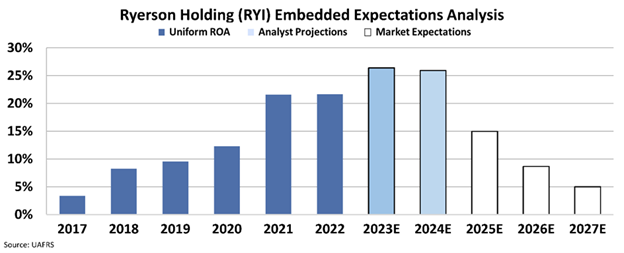

We can see this through our Embedded Expectations Analysis (“EEA”) framework.

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

At the current stock price, the market expects ROA to crash to levels last seen before 2018, while analysts expect even higher than current returns.

The supply-chain supercycle is only beginning, and we are likely to see more investments in infrastructure and green projects in the next decade.

Considering Ryerson’s essential position in these investments, we can expect it to realize higher demand for its products. The market is incredibly pessimistic about the future of this business.

Even if the company cannot reach above 25% that is expected by the analysts and just sustains current levels, there is a huge upside potential.

SUMMARY and Ryerson Holding Corporation Tearsheet

As the Uniform Accounting tearsheet for Ryerson Holding Corporation (RYI:USA) highlights, the Uniform P/E trades at 4.1x, which is below the corporate average of 18.4x but around its historical P/E of 5.0x.

Low P/Es require low EPS growth to sustain them. In the case of Ryerson Holding, the company has recently shown a 7% growth in Uniform EPS.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Ryerson Holding’s Wall Street analyst-driven forecast is a 13% EPS growth in 2023 and an immaterial EPS growth in 2024.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Ryerson Holding Corporation’s $37.32 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink by 25% annually over the next three years. What Wall Street analysts expect for Ryerson Holding’s earnings growth is above what the current stock market valuation requires in 2023 but immaterial in 2024.

Furthermore, the company’s earning power is 4x its long-run corporate average. Moreover, cash flows and cash on hand are 3x its total obligations—including debt maturities, capex maintenance, and dividends. Also, the company’s intrinsic credit risk is 410bps above the risk-free rate.

All in all, this signals low dividend risk.

Lastly, Ryerson Holding’s Uniform earnings growth is above its peer averages but below its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research