Headlines and incorrect data are turning investor opinion wrongly against this pickaxe seller

Today’s company is a pickaxe seller in the travel industry, a sector which is currently under significant pressure due to coronavirus.

Investors are writing off the firm due to its weak performance in a field that now faces new headwinds. However, as-reported accounting is leading investors to believe a story that doesn’t exist.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Investor Essentials Daily:

Tuesday Tearsheets

Powered by Valens Research

A story we have talked about often is the power of the pickaxe seller in a competitive market. When gold miners went west to pan the riverbeds for riches, it was never a sure thing if they’d strike rich, but no matter who found a valuable vein, the people selling pickaxes were guaranteed to make money, as long as someone was digging.

In this way, a firm who provides the necessary infrastructure for an industry is in a winning spot. In February, we talked about Applied Materials, a pickaxe seller in multiple markets.

By providing the fabrication equipment to create semiconductors, they aren’t impacted by short-term market swings in the industry, like demand for cryptocurrency mining.

However, we also talked about the danger of being a pickaxe seller in a dying industry with Tanger Factory Outlets. The retail market has been stagnating these past few years due to innovation in ecommerce. Tanger Factory Outlets is trapped in a market where no one wants to buy a pickaxe (open an outlet store) anymore.

If an industry is being disrupted, even if a firm is occupying a smart market position, then it too will face tough times.

Sabre Corporation is a travel technology company. It calls itself the largest global distribution systems provider for the travel industry. This means Sabre services searching, pricing, and booking for airlines and hotels worldwide.

Of course, in 2020, the entire travel industry has been, to put it delicately, annihilated. The airline industry at one point was under direct threat of bankruptcy.

Airlines are still only flying at 85% capacity for domestic flights. Actual capacity on planes is still very low.

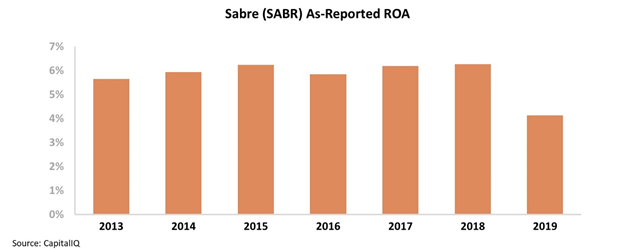

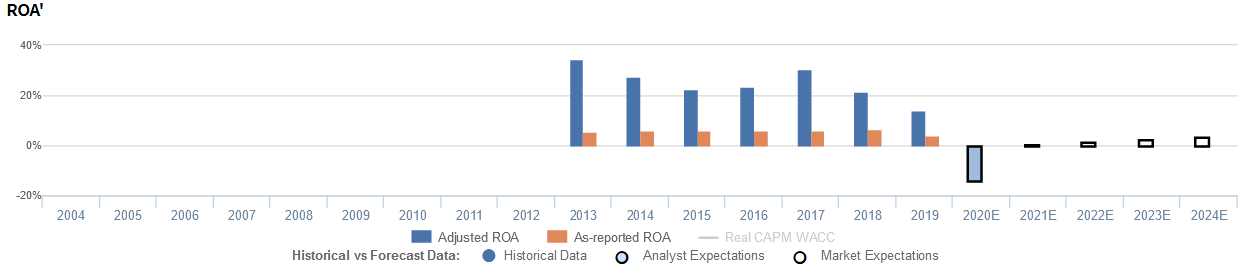

While Sabre provides an essential service to the travel industry, by looking at its as-reported return on assets (ROA), it would appear that Sabre has never been able to leverage its dominant market position, even when times were good.

Over the past seven years, Sabre’s ROA has been consistently below corporate averages near 6%, with a recent dip to 4% in 2019.

Wall Street sees Sabre as a poor pickaxe seller after the gold has dried up. Investors are expecting this short-term disruption to spell the end of Sabre, after operating on razor-thin margins for years.

However, calls for doom are driven only by a distorted picture of as-reported performance.

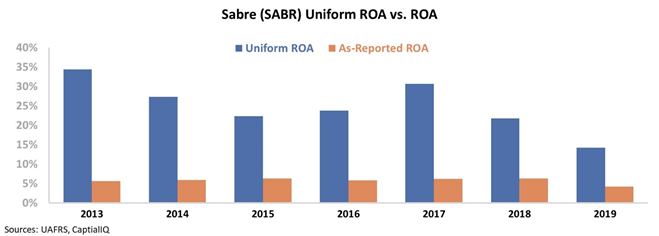

Once we remove the GAAP distortions around line items such as goodwill and interest expense, Sabre’s profitably takes on a different hue.

Rather than scraping by over the past seven years, Sabre has in fact realized considerable profitability due to its pickaxe strategy. Uniform ROA has been between 15% and 35%, well above corporate averages.

The market has been blinded by the dire straits of the airline industry alongside Sabre’s as-reported performance. This overt pessimism has pressured valuations of the firm to bankruptcy levels.

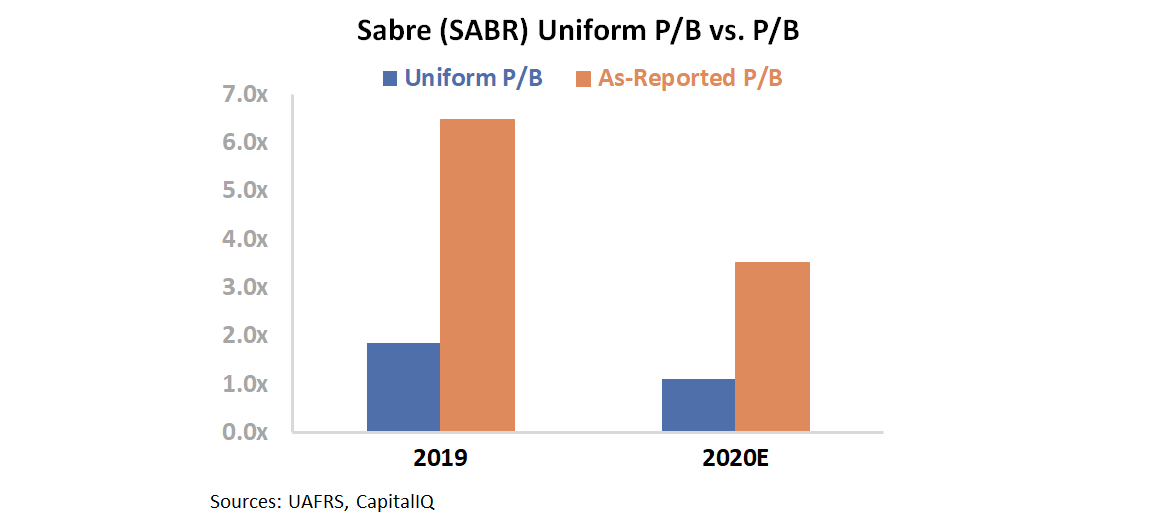

Using as-reported metrics, it appears that Sabre is trading at a 3.5x price to book (P/B) ratio, well above market averages. However, due to previously mentioned distortions to the firm’s asset base, the firm truly trades at a steep discount.

Currently, Sabre trades at a 1.1x price to book, which is near where firms that can’t generate returns above cost-of-capital trade. As you can see, the market clearly views Sabre as a firm whose days are numbered.

With the entire travel industry on the ropes, investors have taken one look at Sabre’s as-reported metrics and thrown the baby out with the bathwater. That means Sabre is currently priced as a low-quality pickaxe seller to a dying industry.

In reality, Sabre is a high-quality pickaxe seller to a market in a temporary freeze, and it has the earnings to survive it. This mismatch between the story the market believes and reality is wide enough to be an investment opportunity.

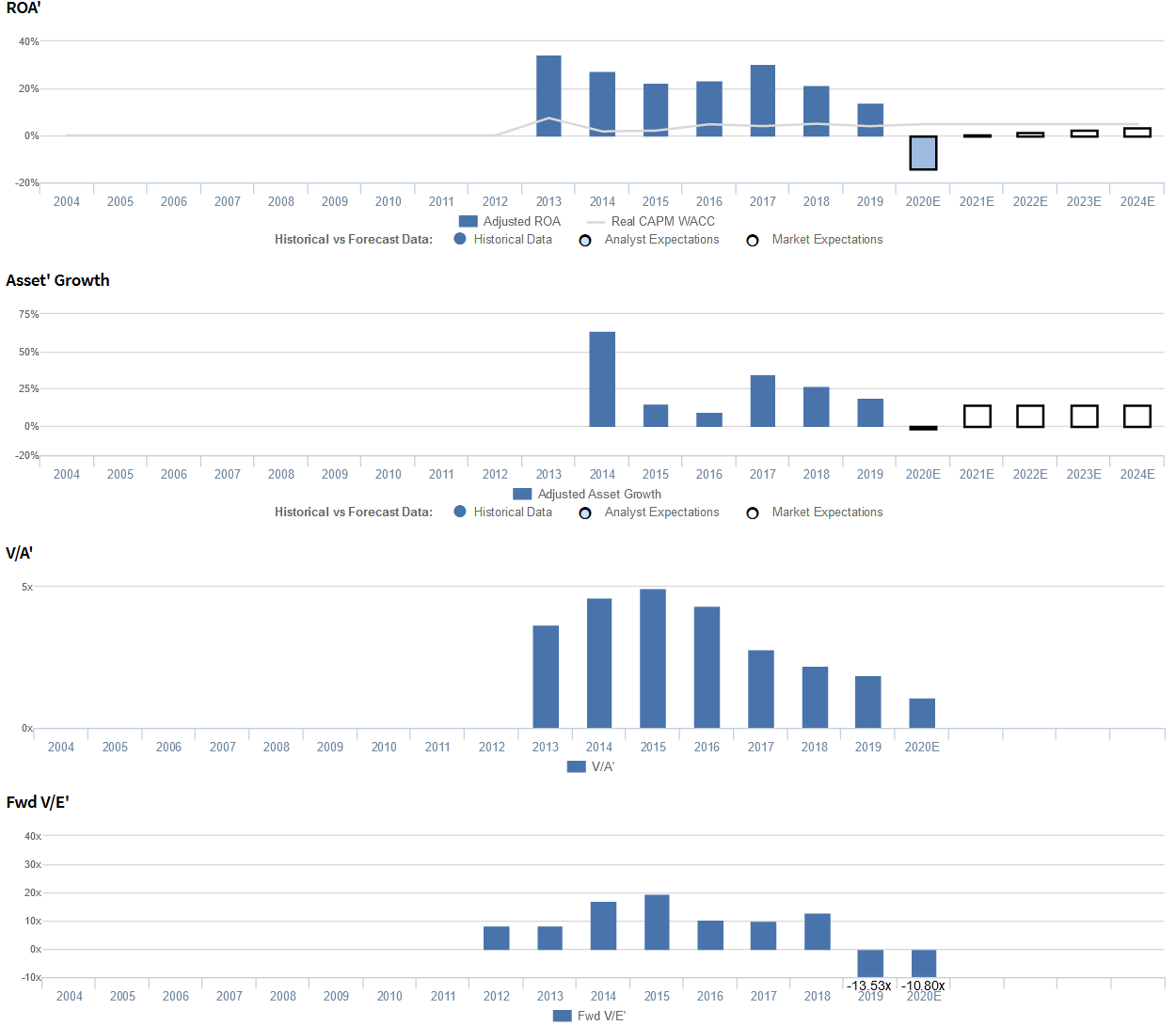

Sabre Corporation Embedded Expectations Analysis – Market expectations are for Uniform ROA to substantially decline, but management is confident about their cost initiatives, cloud migration, and strategy

SABR currently trades near Uniform asset values, with a 1.1x Uniform P/B (V/A′). At these levels, the market is pricing in expectations for Uniform ROA to decline from 14% in 2019 to 3% in 2024, accompanied by 14% Uniform asset growth.

Meanwhile, analysts have more bearish expectations, projecting Uniform ROA to fall to 1% by 2021, accompanied by 2% Uniform asset shrinkage.

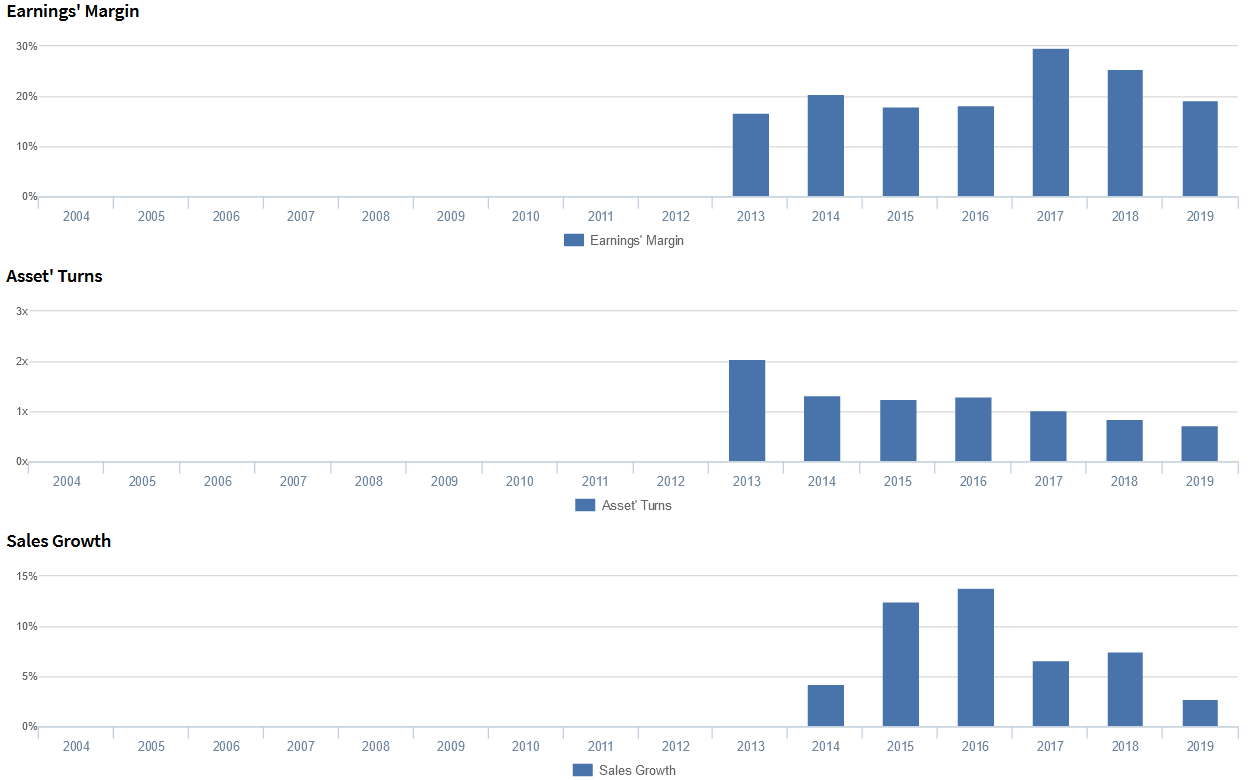

Historically, SABR has seen robust, yet generally declining profitability. Uniform ROA fell from a high of 34% in 2013 to 22% in 2015, before recovering to 31% in 2017 and subsequently compressing to a low of 14% in 2019.

Meanwhile, Uniform asset growth has historically been robust, positive in each of the past six years, while ranging from 9% to 64%.

Performance Drivers – Sales, Margins, and Turns

Declines in Uniform ROA have been driven by declining Uniform asset turns, slightly offset by improvements in Uniform earnings margin.

Uniform turns have steadily declined from a peak of 2.0x in 2013 to 0.7x in 2019. Meanwhile, after ranging from 17%-20% levels in 2013-2016, Uniform margins jumped to 30% in 2017 and declined back to 19% in 2019.

At current valuations, the market is pricing in expectations for both Uniform earnings margin and Uniform asset turns to compress to new lows.

Earnings Call Forensics

Valens’ qualitative analysis of the firm’s Q4 2019 earnings call highlights that management is confident about their long-term growth strategy, that they have navigated through a heavy renewal cycle over the past few years, and that they are collaborating with Accor to develop a full-service property management system.

In addition, they are confident about their focus on having a more efficient and cheaper technology footprint, that their passenger service system cloud migration will strengthen their competitive position, and that they are being careful about their migration to cloud-based platforms.

However, they are also confident they are seeing cancellations and booking slowdown in Europe.

Furthermore, management may have concerns about the impact of the coronavirus, declines in EPS from their reduced capitalization rate, and continued moderation in incentive fee per booking growth.

Additionally, they may lack confidence in their ability to sustain Hospitality Solutions revenue growth, innovate their distribution channels using technology investments, and offer modern and consumer-centric capabilities.

Also, they may be exaggerating the capabilities of their Sabresonic solutions and the strength of partnership with Google.

Finally, they may be downplaying concerns about Sabre air booking declines and political and economic pressures in Latin America and Asia Pacific.

UAFRS VS As-Reported

Uniform Accounting metrics also highlight a significantly different fundamental picture for SABR than as-reported metrics reflect.

As-reported metrics can lead investors to view a company to be dramatically stronger or weaker than real operating fundamentals highlight. Understanding where these distortions occur can help explain why market expectations for the company may be divergent.

As-reported metrics significantly understate SABR’s profitability. For example, as-reported ROA for SABR was 4% in 2019, substantially lower than Uniform ROA of 14%, making SABR appear to be a much weaker business than real economic metrics highlight.

Moreover, prior to 2019, as-reported ROA maintained 6% levels each year, while Uniform ROA ranged from 22%-34% levels over the same period, significantly distorting the market’s perception of the firm’s profitability ceiling.

SUMMARY and Sabre Corporation Tearsheet

As the Uniform Accounting tearsheet for Sabre Corporation (SABR) highlights, the Uniform P/E trades at -10.6x, which is below the corporate average valuation levels and its own recent history.

Negative P/Es require low EPS growth to sustain them. In the case of Sabre, the company has recently shown a 26% Uniform EPS shrinkage.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Sabre’s Wall Street analyst-driven forecast is a 253% shrinkage in 2020, followed by an 86% shrinkage in 2021.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Sabre’s $8 stock price. These are often referred to as market embedded expectations.

The company could have Uniform earnings shrink by 15% each year over the next three years to justify current prices. What Wall Street analysts expect for Sabre’s earnings growth is far below what the current stock market valuation requires in 2020 and 2021.

Furthermore, the company’s earning power is 2x the corporate average. However, the company’s cash flows and cash on hand will consistently fall short of debt headwalls for the next five years. This signals high credit and dividend risk.

To conclude, Sabre’s Uniform earnings growth is the lowest among peer averages, and the company is trading the lowest among average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research