When real estate is knocked down, this company will have ground to stand on

In the current challenging real estate environment marked by rising interest rates and declining demand, Safehold (SAFE) stands out as a defensive option.

As a ground lease REIT with 99-year leases and built-in annual rent escalators, Safehold offers stable cash flows, recession-proof income, and a unique reversionary interest in buildings after the lease duration, making it less susceptible to market cycles than traditional REITs.

Despite its advantageous position, the market has undervalued Safehold, presenting a potential opportunity for long-term investors seeking a lower-risk entry into the real estate space.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

Real estate is facing significant headwinds in the current macroeconomic environment.

With the Fed aggressively raising interest rates to combat high inflation, mortgage rates have more than doubled over the past year.

This has caused housing demand to plummet as financing new home purchases has become much more expensive for consumers. Existing homeowners are also hesitant to trade up due to higher borrowing costs.

As a result, many publicly traded real estate companies that focus on residential and commercial properties are struggling. Demand for new office and retail space has weakened as a recession looms.

Real estate investment trusts (REITs) that hold large property portfolios are seeing occupancy rates decline and rents stagnate in this challenging environment. With property values coming under pressure, concerns around debt levels and potential bankruptcies are rising for leveraged real estate players.

However, one real estate company stands out for its defensive positioning – Safehold (SAFE).

As the first and only pure-play publicly traded ground lease REIT, Safehold has a low-risk business model that provides strong insulation from the current real estate downturn. It gets into ground lease agreements.

A ground lease is a type of lease agreement in which a tenant is given the right to use and develop a piece of land for a specified period, typically long-term. However, the ownership of the land remains with the landlord or ground lessor.

The key aspect is that Safehold’s ground leases are typically 99 years in duration, with built-in annual rent escalators. This provides incredibly stable cash flows that are immune to short-term fluctuations in property values or tenant health.

Even better, at the end of the 99-year period, Safehold takes full ownership of any buildings or improvements on the land. This reversionary interest acts as a call option on future property value appreciation.

As the ground leases are essentially triple net leases, tenants are also responsible for maintenance, insurance, and property taxes – further reducing risk to Safehold.

The long-dated ground leases have allowed Safehold to grow its portfolio to over $6.5 billion without taking on leveraged debt like its peers.

However, the market has so far priced Safehold as any other REIT.

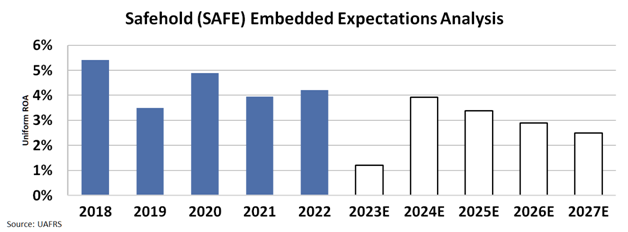

We can see what the market thinks through our Embedded Expectations Analysis (“EEA”) framework.

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

At the current stock price, the market expects the company’s ROA to fall to below 3%.

Despite being in a favorable position, Safehold is currently undervalued by the market.

As fears of a drawn-out downturn persist, Safehold’s defensive attributes make it a compelling way to gain exposure to real estate without the same risks as conventional REITs.

While the stock could see short-term weakness along with the sector, those with a long-term view may find Safehold’s stable cash flows and recession protection make it a lower-risk way to bottom-tick an investment in the real estate space.

SUMMARY and Safehold Inc Tearsheet

As the Uniform Accounting tearsheet for Safehold Inc (SAFE:USA) highlights, the Uniform P/E trades at 23.4x, which is above its global corporate average of 18.4x but below its historical P/E of 27.6x.

High P/Es require high EPS growth to sustain them. In the case of Safehold, the company has recently shown a 3% shrinkage in Uniform EPS.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Safehold’s Wall Street analyst-driven forecast is a 168% and 282% EPS shrinkage in 2023 and 2024, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Safehold’s $19.69 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow 3% annually over the next three years. What Wall Street analysts expect for Safehold’s earnings growth is below what the current stock market valuation requires through 2024.

Furthermore, the company’s earning power is 0.04x its long-run corporate average. Moreover, cash flows and cash on hand are below its total obligations—including debt maturities, capex maintenance, and dividends. Also, the company’s intrinsic credit risk is 370bps above the risk-free rate.

All in all, this signals average credit risk.

Lastly, Safehold’s Uniform earnings growth is below its peer averages but in line with its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research