This company serves as a vital supplier to tech giants, but creditors see only danger ahead

Asset-light business models are all the rage to investors these days. They tend to generate higher ROAs and can scale faster. However, capital-intensive businesses are often safer with steadier cash flows.

Today’s company is one of the world’s largest electronics providers, but credit markets are concerned about its low returns.

Below, we show how Uniform Accounting clarifies the financials for a clear credit profile. We also provide the equity tearsheet showing Uniform Accounting-based Performance and Valuation analysis of the company.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

For almost ten years now, there has been an obsession with finding the “Uber of X”. Whether it be the “Uber of food delivery” or the “Uber of lodging” like the newly public companies DoorDash (DASH) and AirBnB (ABNB), investors are looking for the next platform business in every industry.

The appeal of this model is to be the solution to customers’ needs, without the capital intensity of owning the assets. While Uber (UBER) boasts a massive fleet of cars in its network, the company does not own any of them. This allows the firm to grow faster, as it does not need to make huge capital investments to expand.

One might argue before there was the “Uber” of anything, there were plenty of manufacturers following this model. A prime example was and still is Apple (AAPL).

Apple does not manufacture many of its own products, focusing instead on the design and marketing. Rather, Apple pays independent companies to produce them, with Foxconn (2354:TAI) being one of the biggest.

The companies that actually make electronics products are called “fabricators”. One other well-known fabricator is Sanmina Corporation (SANM).

Sanmina is an electronics manufacturing services provider and one of the largest independent producers of printed circuit boards and backplanes. Some of Sanmina’s customers include Viasat (VSAT), Arista Networks (ANET), and even Nokia (NOK).

Being an asset-intensive manufacturer to other firms rarely leads to high returns, but it does guarantee stability.

Sanmina is an essential part of the infrastructure for the mentioned firms, and it is unlikely to lose business with them. As such, the business risk is not exceptionally high.

Despite this, rating agencies see the company’s below average returns and are concerned for any potential headwinds. The firm has a high-yield Ba1 credit rating from Moody’s, implying a risk of default near 11% over the next five years.

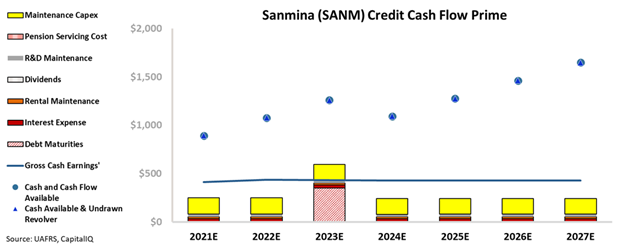

However, the company’s Credit Cash Flow Prime (CCFP) tells us a different story. The firm is actually a much stronger credit than rating agencies give it credit for.

Cash flows exceed all obligations through 2023. Sanmina’s comfortable $500 million cash on hand buffer covers this shortfall handily, exceeding obligations in every year after.

Thus, Valens rates the firm as a much safer investment grade IG3+ rating. This only implies a chance of default around 1% over the next five years. Thanks to Sanmina’s sizable cash buffer, investors should have little to fear.

Ultimately, even with a low ROA, the company’s steady cash flows, strong balance sheet, and limited debt mitigate credit risk. Only when looking at Sanmina under the Uniform Accounting framework can we see the true risk of this fabricator.

SUMMARY and Sanmina Corporation Tearsheet

As the Uniform Accounting tearsheet for Sanmina Corporation (SANM:USA) highlights, the company trades at a 15.2x Uniform P/E, which is below global corporate average valuation levels and its own historical average valuations.

Low P/Es require low EPS growth to sustain them. That said, in the case of Sanmina, the company has recently shown a 20% Uniform EPS contraction.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Sanmina’s Wall Street analyst-driven forecast projects 53% and 11% EPS growth in 2021 and 2022, respectively.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Sanmina’s $32 stock price. These are often referred to as market embedded expectations.

The company can have immaterial Uniform earnings growth each year over the next three years and still justify current prices. What Wall Street analysts expect for Sanmina’s earnings growth is well above what the current stock market valuation requires in 2021 and 2022.

However, the company’s earning power is below the corporate average. That said, the firm’s cash flows and cash on hand are 3x its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals moderate dividend and credit risk.

To conclude, Sanmina’s Uniform earnings growth is above its peer averages, but the company is trading below its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research