The market is devastated after OPEC’s production cuts on oil and fails to see the value of this oil giant

OPEC announced in early October that it would cut back on production going forward to keep oil prices around $90, where oil players make a lot of money.

U.S. Shale Renaissance names will see huge profits, but so will the largest oil company in the world, Saudi Aramco (SASE:2222).

With its massive low-cost assets and professional management team, it will benefit from a floor price to oil, and start printing money.

However, our Embedded Expectations Analysis (“EEA”) shows that the market doesn’t recognize this value, which creates an opportunity for investors.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

The Organization of the Petroleum Exporting Countries (“OPEC”) was on the headlines again early this month with an unexpected announcement.

The organization drew the ire of Biden and the West saying it would cut back on production going forward. It seeks to preserve prices above $90 a barrel, where every oil company makes lots of money.

While this is devastating news for consumers who drive to work daily, it benefits the U.S. “Shale Renaissance”. With Russia’s supply out of the market, these companies will thrive when the oil price is high.

Oil exploration and production (“E&P”) players have been waiting on the sides to invest more in capex. They will have more confidence in growing their businesses if there is a floor on the price of oil.

However, U.S. shale will not be the only winner in this commitment to prices in the high double digits. The largest oil company in the world is also getting ready to print money.

Saudi Arabian Oil Company (SASE:2222), also known as Saudi Aramco, is sitting on 254 billion barrels of oil equivalent of reserves, which it can extract at a lower cost than its competitors.

The cost of producing a barrel of oil and gas was much lower in Saudi Arabia compared to countries like the U.K., Canada, U.S., and Russia.

This means a huge opportunity for the company if the oil price stays high. It already recognized increasing profitability with the latest jump in prices.

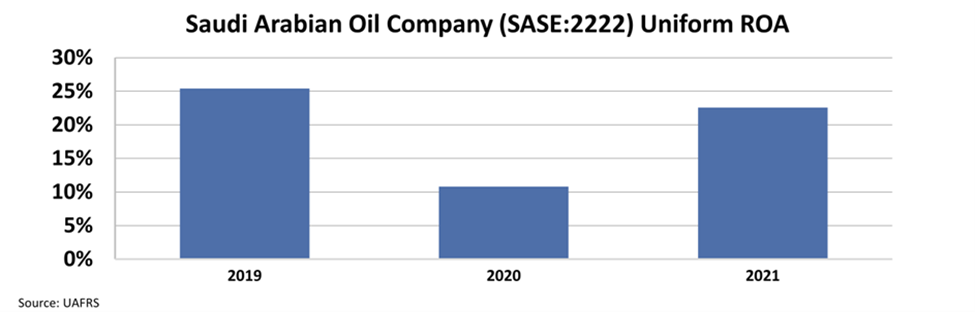

The demand shock at the beginning of the pandemic drove prices down, and Saudi Aramco’s Uniform return on assets (“ROA”) crashed from 25% in 2019 to 11% in 2020. However, it quickly recovered thanks to the rising prices and reached a Uniform ROA of 23% in 2021.

The company’s exposure to oil prices is undeniable, and prices around $90 will drive profitability upwards. Therefore, this company may seem like a good investment opportunity. However, if the market is already pricing in these developments, there would be no additional value.

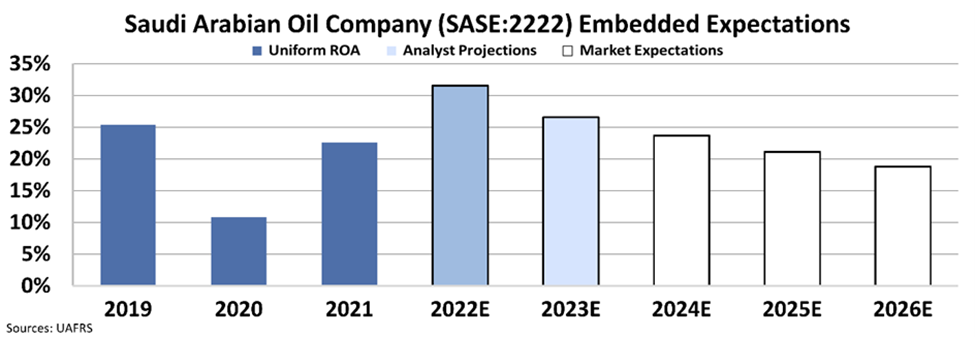

By utilizing our Embedded Expectations Analysis (“EEA”) framework, we can see what investors expect these companies to do at the current stock price.

Stock valuations are typically determined using a discounted cash flow (“DCF”) model, which makes assumptions about the future and produces the “intrinsic value” of the stock.

We know models with garbage-in assumptions based on distorted GAAP metrics only come out as garbage. Therefore, we use the current stock price with our Embedded Expectations Analysis to determine what returns the market expects.

At around 36 Saudi Arabian Riyal (SAR) price levels, the market expects the company to have a slightly lower Uniform ROA of 19%. However, analysts actually expect the company to have higher profitability, reaching 28%.

Our Embedded Expectations Analysis clearly shows that the market fails to recognize the sustainability of Saudi Aramco’s profitability and its competitive advantages thanks to low cost assets and a professional management team.

If oil prices stay around $90, this company is going to see huge benefits and possibly increase its profitability higher than the levels the market expects.

SUMMARY and Saudi Arabian Oil Company Tearsheet

As the Uniform Accounting tearsheet for Saudi Arabian Oil Company (SASE:2222) highlights, the Uniform P/E trades at 15.0x, which is below the global corporate average of 18.9x and its own historical P/E of 24.0x.

Low P/Es require low EPS growth to sustain them. In the case of Saudi Arabian Oil Company, the company has recently shown a 119% increase in Uniform EPS.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Saudi Arabian Oil Company’s Wall Street analyst-driven forecast is a 54% growth and -16% EPS shrinkage in 2022 and 2023, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Saudi Arabian Oil Company’s SAR 36 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow by 1% annually over the next three years. What Wall Street analysts expect for Saudi Arabian Oil Company’s earnings growth is above what the current stock market valuation requires in 2022 but below in 2023.

Furthermore, the company’s earning power in 2021 is 4x the long-run corporate average. Moreover, cash flows and cash on hand are 3x its total obligations—including debt maturities, capex maintenance, and dividends. Also, the company’s intrinsic credit risk is 20bps above the risk-free rate.

All in all, this signals low dividend risk.

Lastly, Saudi Arabian Oil Company’s Uniform earnings growth is in line with its peer averages, but below its peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research