The British East India Company changed Chinese culture forever in order to reap major rewards, and now a new firm is attempting to do the same

The British East India Company helped open the door to global trade with China, producing tremendous profits while dramatically changing Chinese culture and its perception of outsiders.

More than 150 years later, another Western firm is trying to spur an equally ambitious culture change in the country, to try to tap into the high-potential market. However, as-reported metrics are inaccurately making it seem that the firm’s expansion strategy hasn’t been paying off.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Investor Essentials Daily:

Tuesday Tearsheets

Powered by Valens Research

In the 1700’s, the British East India company opened the door to a dramatic change in Chinese culture.

What had started as a pursuit for sought-after assets such as tea, silk, and porcelain from China evolved into a booming trade for the British, as merchants offset the cost of exported goods with imports of silver, Bengal cotton, and the most profitable of all, opium.

Over the years, Chinese leadership became increasingly fed up with the importation of the powerful opiate, as its primary use transitioned from medicinal to recreational. In 1800, the import of opium was banned, which only caused long-lasting tensions to intensify.

Opium was too profitable and the British weren’t about to give up their cash cow.

Through bribery and laundering, the firm smuggled the product en masse through the port of Canton, which eventually became modern Hong Kong. Ultimately, China resisted the dumping of the drug on its markets more forcefully. The terms of trade were no longer in its hands.

The subsequent Opium Wars ravaged the nation for decades, but ultimately, China was unable to defeat the British East India company, backed by the full naval strength of the British Empire. As a result, the Treaty of Nanking was signed, and China was fundamentally changed.

The once closed-off civilization was opened up for global trade, a trade which disproportionately benefited Western nations. Meanwhile, its people grew increasingly wary of Western civilizations and many, to this day, harbor a deep distrust of outsiders.

The saga was a powerful example of how companies can transform a country’s culture, albeit in this case, with the support of one of the most dominant military powers at its time.

It took another 150 years after the end of the last Opium war for another Western company to try to similarly change Chinese culture, by getting a tea-drinking society to adopt coffee.

In 1999, Starbucks (SBUX) entered China.

Although the transition was slow at first, Starbucks has had incredible success in China, with the country now sitting firmly as its second largest market by store count and sales. More broadly, China’s coffee consumption has skyrocketed, increasing by an estimated 1,032% from 2008 to 2018.

In the past two years, Starbucks has continued to ramp-up rapidly in China and internationally. It also has expanded its e-commerce operations. It seems that the firm’s goal is to be the next British East India Company—that is, to disrupt the status quo in China and open it up to a whole new market.

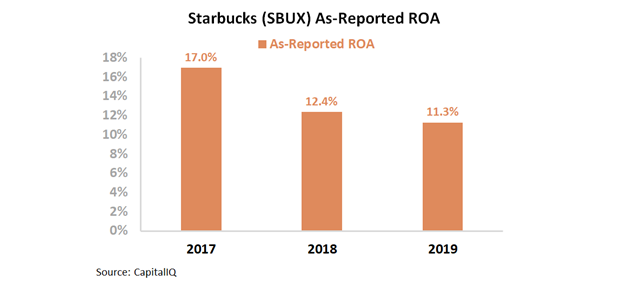

All these initiatives seem to have led to the company plowing too much money into growing the business, as its as-reported ROA has faded significantly in recent years.

The firm’s dramatic drop from a robust 17% ROA in 2017 to more moderate 11%-12% levels in 2018-2019 calls into question the firm’s international strategy. Perhaps the firm is stretching itself too thin and extending itself into unchartered territory that it is ill-equipped to navigate.

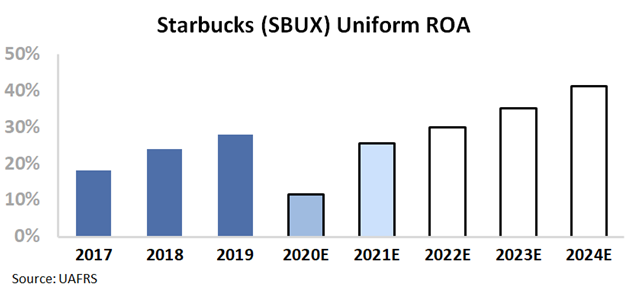

However, once we remove as-reported distortions we can see just how accretive this focus on a new market has been for the firm.

The firm hasn’t seen a compression in profitability in recent years. In fact, the firm’s profitability has greatly expanded, with Uniform ROA improving from already robust 18% levels in 2017 to an even stronger 28% in 2019.

While this is forecast to be disrupted by the coronavirus pandemic in 2020, expectations are for this to rebound immediately in 2021.

Starbucks’s expansion in China has been extremely beneficial for the firm, and even though the country has already seen a rapid acceleration of coffee consumption, China, on average, still consumes only a fraction of the coffee Western countries such as the United States do.

As such, the market still has plenty of untapped potential. This, coupled with the struggles of its chief competitor in China, Luckin Coffee, which is embroiled in a fraud investigation, gives many positive tailwinds for the name.

Therefore, the market expects Starbucks to be able to rebound strongly following the coronavirus-driven slowdown, with Uniform ROA projected to continue to climb to new peaks.

Starbucks Embedded Expectations Analysis – Market expectations are for improvements in Uniform ROA, but management may be concerned about revenue, China, and customers

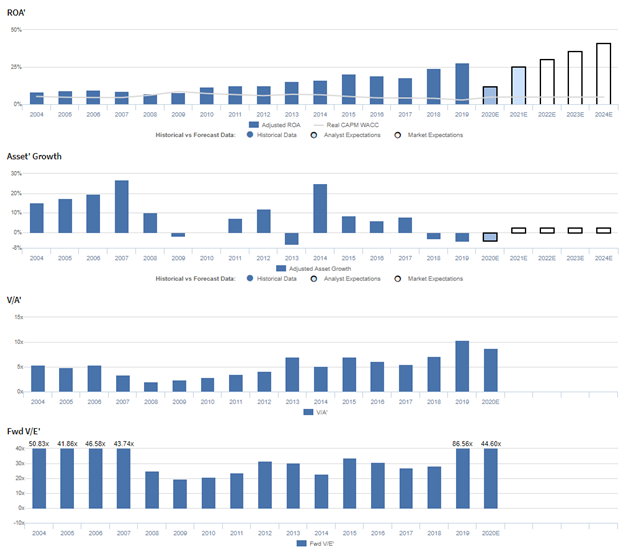

SBUX currently trades near historical highs relative to Uniform earnings, with a 44.9x Uniform P/E (Fwd V/E′). At these levels, the market is pricing in expectations for Uniform ROA to expand from 28% in 2019 to 41% in 2024, accompanied by 2% Uniform asset growth going forward.

However, analysts have muted expectations, projecting Uniform ROA to fade to 26% in 2021, accompanied by 4% Uniform asset shrinkage.

Historically, SBUX has seen robust, improving profitability. Uniform ROA expanded from 7%-9% levels in 2004-2009 to 20% in 2015, before declining to 18% in 2017 and subsequently jumping to 28% in 2019.

Meanwhile, Uniform asset growth has been volatile, positive in eleven of the past sixteen years, while ranging from -6% to 27%.

Performance Drivers – Sales, Margins, and Turns

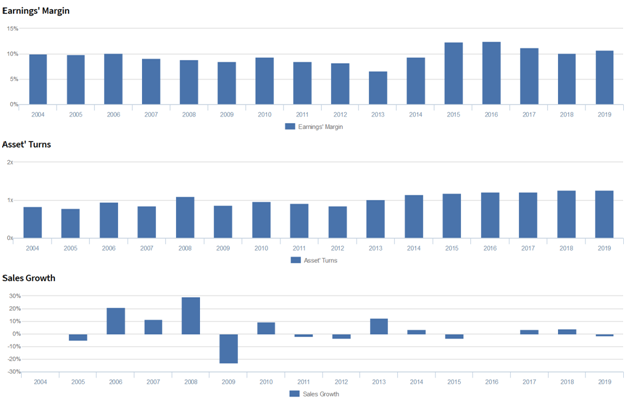

Improvements in Uniform ROA have been largely driven by trends in Uniform earnings margins and to a lesser extent, Uniform asset turns.

Uniform earnings margins ranged from 5%-7% from 2004-2009 before expanding to 9%-10% levels in 2010-2013 and climbing further to a peak of 14% in 2015. Since then, Uniform earnings margins have maintained 13% levels through 2019.

Meanwhile, Uniform asset turns ranged at 1.2x-1.4x from 2004-2012 before jumping to 1.7x in 2013 and fading to 1.4x in 2017. Thereafter, Uniform asset turns climbed to a peak of 2.2x in 2019.

At current valuations, markets are pricing in expectations for both Uniform earnings margins and Uniform asset turns to climb to new peaks.

Earnings Call Forensics

Valens’ qualitative analysis of the firm’s Q1 2020 earnings call highlights that management generated an excitement marker when discussing their store environment.

In addition, they are confident that they are looking to deepen their relationship with customers, and they will use AI-enabled machines to deliver coffee better, faster, and with more variety.

However, management may lack confidence in their ability to sustain US revenue and comp sales growth, continue leading consumer perception of specialty coffee retail concepts, and increase their Mobile Order and Pay transaction mix.

In addition, they may have concerns about the impact of COVID-19 on near-term traffic results and store closures and sales slowdown at open stores.

Moreover, they may lack confidence in their ability to sustain sales growth in China from continued expansion and mobile ordering and improve digital customer engagement.

Furthermore, they may have concerns about the performance of their hot drinks business and the success of their sustainability initiatives with third-party advocacy groups and industry partnerships.

Finally, they may be exaggerating the strength of their brand.

UAFRS VS As-Reported

Uniform Accounting metrics also highlight a significantly different fundamental picture for SBUX than as-reported metrics reflect.

As-reported metrics can lead investors to view a company to be dramatically stronger or weaker than real operating fundamentals highlight.

Understanding where these distortions occur can help explain why market expectations for the company may be divergent.

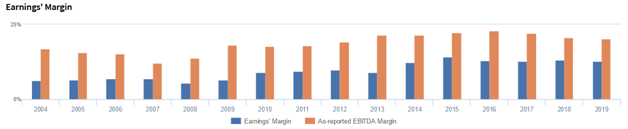

As-reported metrics significantly overstate SBUX’s margins, one of the primary drivers of profitability.

For example, as-reported EBITDA margin for SBUX was 20% in 2019, materially higher than Uniform earnings margins of 13% in the same year, making SBUX appear to be a much stronger business than real economic metrics highlight.

Moreover, as-reported margins have been at least 1.5x greater than Uniform earnings margins in each year since 2004, significantly distorting the market’s perception of the firm’s historical performance.

SUMMARY and Starbucks Corporation Tearsheet

As the Uniform Accounting tearsheet for Starbucks Corporation (SBUX) highlights, it trades at a 44.9x Uniform P/E, which is above corporate average valuations but below the company’s historical average valuations.

High P/Es require high EPS growth to sustain them. In the case of Starbucks, the company has recently shown a robust Uniform EPS growth of 12%.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Starbucks’ Wall Street analyst-driven forecast is for Uniform EPS shrinkage of 63% in 2020, followed by 174% growth in 2021.

Based on current stock market valuations, we can back into the required earnings growth rate that would justify $74 per share. These are often referred to as market embedded expectations.

In order to meet current market valuation levels, Starbucks would have to have Uniform earnings grow 7% each year over the next three years.

What Wall Street analysts expect for Starbucks’ earnings growth is lower than what the current stock market valuation requires.

Meanwhile, the company’s earnings power is 5x corporate averages, and their robust cash flows and cash on hand signal that there is low risk to the company’s operations and credit profile.

To conclude, Starbucks’ Uniform earnings power is lower than peer averages, but its high valuations require high EPS growth that analysts do not expect the firm to be able to achieve.

Best regards,

Joel Litman

Chief Investment Strategist

at Valens Research