Poor accounting data and smart digging spelled a 250% gain on this company for our readers

After spotting material distortions in GAAP accounting, we were able to recommend a trade based on real Uniform returns for the business. This recommendation turned into a 250% gain for our readers.

By viewing better accounting data, investors are able to make smarter investment decisions before the market catches on.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

Under Biden’s current administration, the discussion around clean energy solutions has seen renewed interest in Washington. As a result, the demand for products and companies that are helping make for a cleaner future in our world is soaring.

Even though there is still debate around the topic, infrastructure planners and investors are seeing more use for clean energy solutions such as wind turbines, solar panels, and other renewable energy sources.

In fact, Biden has set ambitious goals for the U.S., including looking into a bill banning gas cars by a certain date. This is why for many investors, the industry at the front and center of this push to go green is electric vehicles (EVs).

While names like Tesla (TSLA) are breaking barriers, legacy car names such as Ford (F), BMW, and Volkswagen are developing EVs of their own.

However, the automotive industry is not the only space that investors should keep a close eye on. Investors should also have other industries on their investing radar for making a greener future.

This is where clean energy solutions, like solar energy, come into play. This industry is likely to see booming demand as people continue to go green. With many of these strong macroeconomic tailwinds in place, the solar industry is an interesting space to dig deeper into.

One of our favorite picks in the space for some time was SolarEdge Technologies (SEDG). We even put this name on our Conviction Long List.

However, after realizing a 252% gain since we recommended the stock, we decided to remove the name from our list back in December.

We still believe the company is a strong performer, but after valuations surged, it was no longer trading at an attractive price.

The reason we originally thought SolarEdge Technologies was so compelling at the time we recommended it was because as-reported return on assets (ROA) were significantly understating how profitable the company actually was.

Investors only looking at the as-reported metrics were pricing in the company for stagnancy instead of success.

The company’s systems are essential in converting solar power into usable energy for homes and offices.

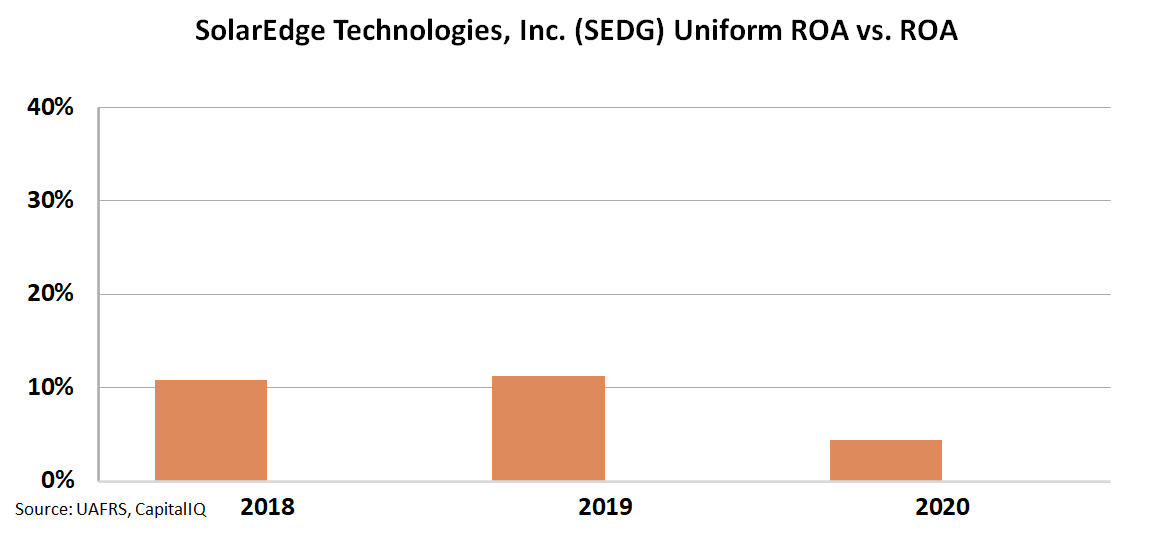

However, the company’s as-reported return on asset (ROA) was hovering around 11% levels in 2018 and 2019, before collapsing to 4% levels in 2020.

For context, the U.S. corporate average for returns is currently around 12%. So, the company appeared to be generating returns below the average.

See for yourself below.

In reality, this is not an accurate picture of SolarEdge Technologies’ profitability.

The company is not generating returns below the U.S. corporate average. In reality, SolarEdge Technologies is posting robust returns.

For example, the company’s returns in 2018 were at 33% levels, back when we recommended it. In 2020 when spending was constricted, the company’s returns were still at 21% levels, well above the average.

See for yourself below.

When the market finally caught on to the distortions in as-reported accounting, the stock surged.

While we ended up closing our position on the name, SolarEdge highlights how looking at better accounting leads to more timely investment decisions.

SUMMARY and SolarEdge Technologies, Inc. Tearsheet

As the Uniform Accounting tearsheet for SolarEdge Technologies, Inc. (SEDG:USA) highlights, the Uniform P/E trades at 42.2x, which is above the global corporate average of 23.7x and its own historical average of 32.5x.

High P/Es require high EPS growth to sustain them. That said, in the case of SolarEdge, the company has recently shown a 16% Uniform EPS contraction.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, SolarEdge’s Wall Street analyst-driven forecast is a 17% and 38% EPS growth in 2021 and 2022, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify SolarEdge’s $243 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow by 24% annually over the next three years. What Wall Street analysts expect for SolarEdge’s earnings growth is below what the current stock market valuation requires in 2021 but above that requirement in 2022.

Furthermore, the company’s earning power is 3x above the long-run corporate average. Also, cash flows and cash on hand are at 7x its total obligations—including debt maturities, capex maintenance, and dividends. Meanwhile, intrinsic credit risk is 40bps above the risk-free rate. All in all, this signals a low dividend and credit risk.

To conclude, SolarEdge Technologies’ Uniform earnings growth is well below its peer averages, and the company is trading significantly above its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research