This server manufacturer could deliver upside as data center expenditure shows no signs of slowing down

Hyperscalers such as Microsoft (MSFT) and Amazon (AMZN) have spent billions of dollars this year on data center infrastructure.

Even though the market is concerned about the sustainability of this buildout, tech companies have shown no indication of slowing down spending anytime soon, putting data center equipment manufacturers in a position to capitalize.

Super Micro Computer (SMCI), one of the largest manufacturers of high-performance server and storage systems, is among the firms who are positioned to take advantage of soaring demand arising from AI-driven expansion.

Yet despite posting strong returns in the past couple of years and generating an eye-popping 127% Uniform asset growth last year, the company trades at just a 17.3x Uniform P/E, well below corporate averages.

Investor Essentials Daily:

Tuesday News-based Update

Powered by Valens Research

The artificial intelligence (“AI”) boom has massively accelerated the buildout of data centers as hyperscalers compete amongst each other in the development and delivery of advanced AI models.

As a result, spending on data center infrastructure is expected to amount to trillions in the next five years.

Just last week, it was reported that the capital expenditure of Meta (META), Microsoft (MSFT), Alphabet (GOOG), and (AMZN) for 2025 was around $370 billion this year, with that figure expected to rise further in 2026 as the AI arms race continues to intensify.

Simply said, data center buildout has intensified and will continue to do so for the foreseeable future. And with that, companies that provide the equipment needed to keep these data centers functioning will be well-positioned to capitalize.

And one of those companies is Super Micro Computer (SMCI).

Founded in 1993 and based in California, the firm has built its reputation as one of the largest manufacturers of high-performance data servers.

Currently, the company offers a wide array of hardware and software solutions.

On the hardware side, Super Micro designs and manufactures servers, server racks, GPU systems, data storage, server and workstation boards, cooling solutions, networking equipment, and other related hardware.

Meanwhile, software offerings include cloud services, virtualization, 5G network, IT-related services and other cloud-related solutions.

Super Micro has positioned itself well to thrive in the age of AI, as it has designed software and hardware offerings tailored specifically to AI workloads.

It has also partnered with Nvidia (NVDA), AMD (AMD), and Intel (INTC) to supply the hardware needed for all of its server-related offerings.

By positioning itself as a valuable supplier of data center equipment, the company has steadily grown its revenues from $6.6 billion in 2022 to $20 billion in 2024.

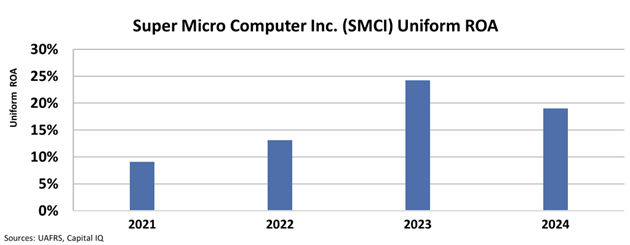

Super Micro’s Uniform return on assets (“ROA”) have likewise improved, rising from 9% in 2021 to 24% in 2023. Last year, ROA declined slightly to 19% but the company posted an eye-popping Uniform asset growth of 127%.

Yet despite being a strong performer the company currently trades at a Uniform P/E of 17.3x, well below corporate averages.

This valuation suggests that the market is doubting the sustainability of today’s AI-driven expansion and demand for data center infrastructure and equipment.

Despite these concerns, hyperscalers show no signs of slowing down their AI infrastructure buildout, as a result, Super Micro is positioned to benefit from this continued spending.

If Super Micro can continue to scale production of its GPU-optimized servers while managing its supply chain execution, it could be poised to warrant significant upside in the AI infrastructure race.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research