Uniform Accounting shows the reason why Amazon went after Whole Foods in 2017

One of the most talked about acquisitions of recent history has been Amazon (AMZN) purchasing Whole Foods back in 2017. Investors were speculating why Jeff Bezos had gone so far outside Amazon’s purview.

Meanwhile, the entire healthy eating market is not created equal. Other companies in the space, including today’s focus, would have provided less value to Amazon. The reason why Amazon went after Whole Foods can be seen using Uniform Accounting.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

For over twenty years, Amazon (AMZN) has grown tremendously from an online book retailer to an internet marketplace juggernaut. The firm has also branched out into hardware sales such as the Kindle and Echo, and now hosts an industry-leading web services business.

While the company has branched out to different markets, few would argue its core competency in 2017 wasn’t in grocery shopping. However, Amazon made the move to acquire Whole Foods in 2017 for $13.7 billion.

After the initial reaction of confusion, investors began to see the sense in this move by Amazon. The company has consistently moved into different businesses, and using its high speed, low drag business model, priced out the competition.

With Amazon Fresh on the horizon, management was looking for an “in” to the healthy grocer market. Furthermore, Whole Foods could serve as a testbed for the still experimental Amazon Go grocery stores that had no checkout lines.

Whole Foods also complimented Amazon’s existing expertise, making it the ideal partner for this move.

As the leading premium healthy food distributor, Whole Foods always had higher margins than other grocery stores. However, the business suffered from poor asset efficiency. Other grocery stores were much better at selling a larger volume of product from existing locations.

Meanwhile, Amazon has historically operated as a low margin, high turns business. With expertise in selling a large number of products at razor thin margins, Amazon can bring this knowledge to help Whole Foods boost returns. Amazon’s asset efficiency combined with Whole Foods’ healthy margins promised to unlock significant synergy.

This means a less well known name like Sprouts Farmers Market (SFM), despite being in the same business as Whole Foods, might not have been as good a deal for Amazon.

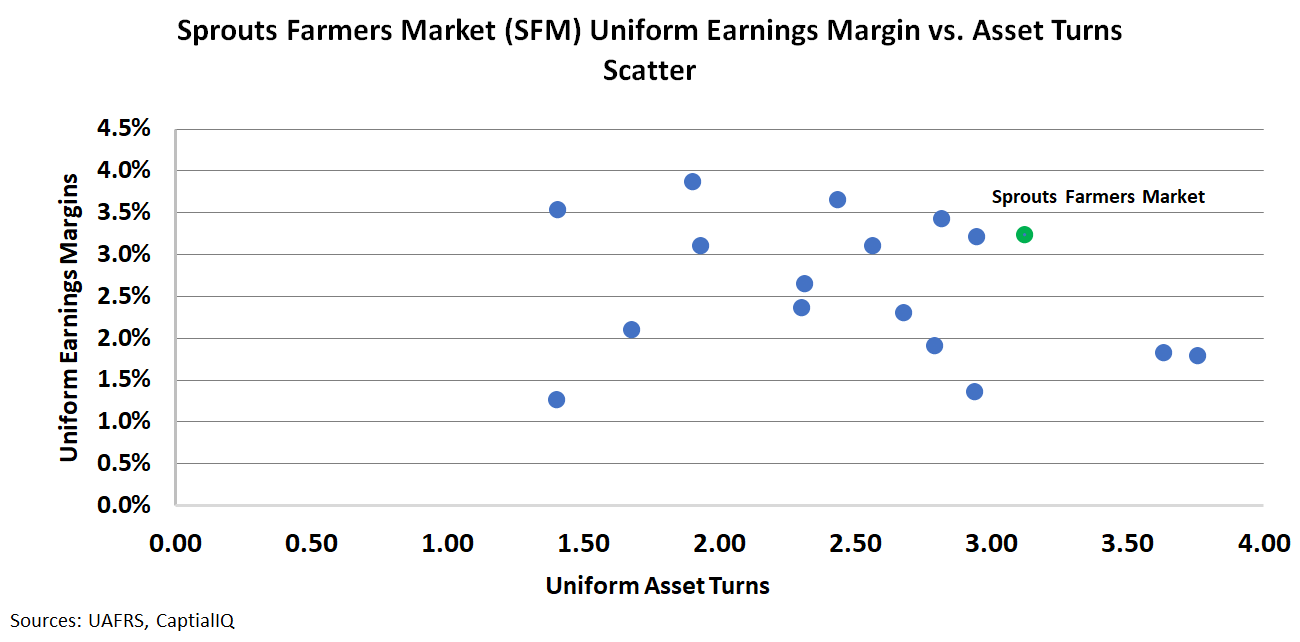

While Whole Foods had strong margins, but weak asset turns, Sprouts Farmers Market has seen strong turns at over 3x over the past three years. Furthermore, these high turns are matched by margins over 3%, which are strong in the grocery space.

To get a better understanding of how Sprouts Farmers Market compares to the entire industry, we can map the company in a scatter chart against its peers. As you can see below, Sprouts Farmers Market is in the top right of the chart, leading peers in both earnings margins and asset turns.

If Amazon was interested in buying a firm like Sprouts, it most likely would have needed to pay a sizable premium for performance. Sprouts has all of the benefits of a premium food distributor, but none of the asset inefficiencies of Whole Foods in 2017.

Furthermore, were an investor to use as-reported metrics, they would never be able to quickly spot Sprouts Farmers Market’s outperformance, as it is completely skewed by as-reported metrics.

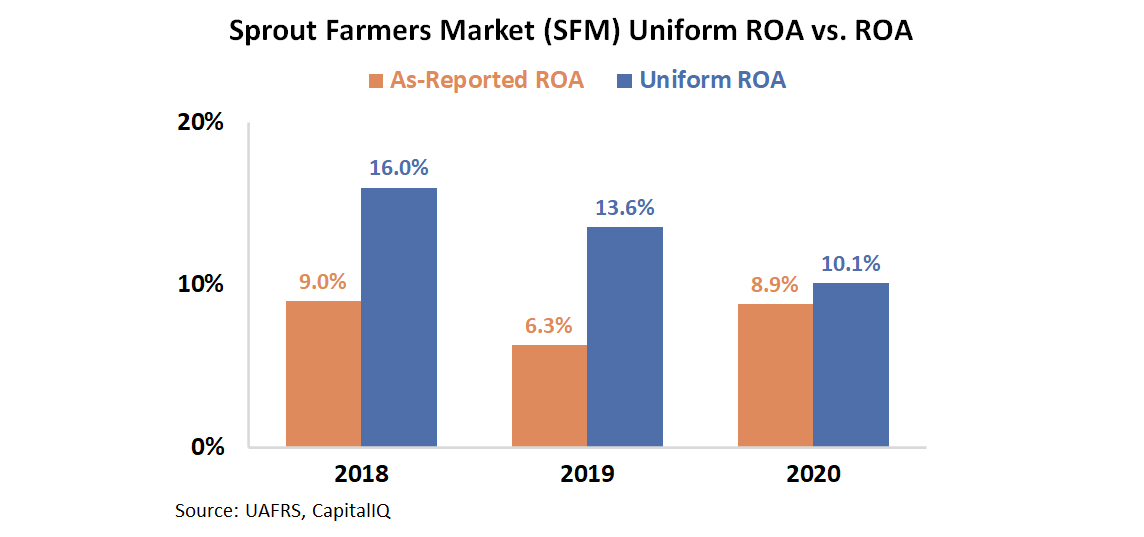

In the past three years, the company has seen Uniform ROA well above the corporate average, excluding 2020 when all physical retailers were impacted by the pandemic.

The power of Uniform Accounting gives investors and management teams actionable insights to a company’s real performance.

Had Amazon used adjusted metrics, it would’ve been unsure of which healthy grocer to buy. Meanwhile, investors can use this same data to quickly find the strongest performer as well.

SUMMARY and Sprouts Farmers Market, Inc. Tearsheet

As the Uniform Accounting tearsheet for Sprouts Farmers Market, Inc. (SFM:USA) highlights, the Uniform P/E trades at 15.8x, which is below the global corporate average of 25.2x and its own historical average of 18.1x.

Low P/Es require low EPS growth to sustain them. In the case of Sprouts Farmers Market, the company has recently shown a 6% Uniform EPS shrinkage.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Sprouts Farmers Market’s Wall Street analyst-driven forecast is a 78% EPS growth in 2020 and a 21% EPS decline in 2021.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Sprouts Farmers Market’s $22 stock price. These are often referred to as market embedded expectations.

Sprouts Farmers Market is currently being valued as if Uniform earnings were to grow 3% annually over the next three years. What Wall Street analysts expect for Sprouts Farmers Market’s earnings growth is above what the current stock market valuation requires in 2020, but below that requirement in 2021.

Furthermore, the company’s earning power is 2x the long-run corporate average. However, intrinsic credit risk is 180bps above the risk-free rate and cash flows and cash on hand are just slightly above its total obligations—including debt maturities, capex maintenance, and dividends. All in all, this signals a moderate credit risk.

To conclude, Sprouts Farmers Market’s Uniform earnings growth is above its peer averages but the company is trading below its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research