The Valspar acquisition looks like Sherwin-Williams’ biggest mistake

Mergers and acquisitions (“M&A”) are a routine part of life in Corporate America.

Companies frequently acquire smaller industry peers or even main rivals to expand their market share and improve their businesses.

The issue for investors is that as-reported accounting metrics often fail to capture the true economic reality of companies undergoing an M&A transaction.

Today, we’ll recap the failures of Wall Street accounting standards to deal with M&A activity and highlight one name in particular whose true corporate performance has been masked by arbitrary accounting practices.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

Each month, we publish a missive about the distortions inherent to the Generally Accepted Accounting Principles (“GAAP”) used in the U.S. and the International Financial Reporting Standards (“IFRS”) used by companies around the rest of the world.

The report comes from the Uniform Adjusted Financial Reporting Standards (“UAFRS”) Council.

The mission of this organization is to continually identify accounting inconsistencies and improve the ways in which Uniform Accounting can help resolve these issues for investors.

Recently, our focus has been on issues regarding mergers and acquisitions (“M&A”) accounting and the problems they create for investors.

We specifically highlight how distortions surrounding a company’s true asset base and real earning power can materially upend corporate performance and prevent investors from understanding the economic reality of a business.

M&A accounting issues on the financial statements are caused by everything from miscaptured property, plant and equipment (“PP&E”) to research and development (“R&D”) expenses that can drastically understate or overstate assets and earnings.

A great example of this failure of as-reported accounting to deal with M&A issues can be found by looking at a dominant name in the paint industry, The Sherwin-Williams Company (SHW).

The company’s acquisition of Valspar, a fellow paint producer, in 2017 transformed the business by combining two of the largest players in the industry.

This transformative acquisition enabled a series of cross-selling opportunities and a reduction of cost redundancies that significantly benefited Sherwin-Williams.

One would rightly expect that as the integration of the two leading paint businesses developed, Sherwin-Williams would see a strong boost to its profitability.

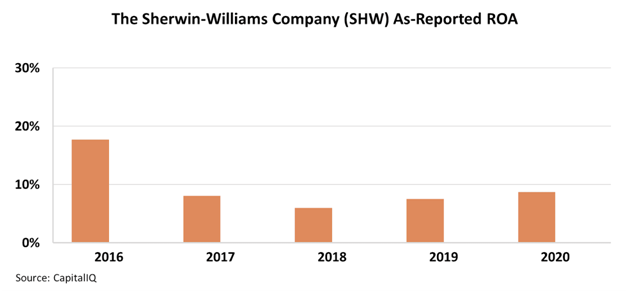

Yet, on an as-reported basis, the combined company’s return on assets (“ROA”) fell by more than half after the deal had closed, from 18% in 2016 to only 8% in 2017.

It gets even more bewildering. The as-reported numbers suggest that returns not only fell off a cliff but that they also never recovered to the levels they maintained before the merger.

See for yourself below.

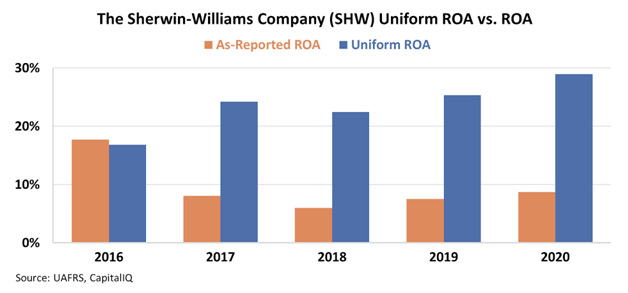

In reality, Uniform Accounting metrics clearly highlight that combining the paint industry’s two largest players has unlocked massive value for Sherwin-Williams’ business.

After adjusting for the massive increase in arbitrary M&A accounting items like goodwill and intangibles, which distort the company’s asset base, we can see that Sherwin-Williams’ Uniform ROA has rapidly expanded since the deal closed, jumping from 17% in 2016 to an impressive 29% by 2020.

By adjusting the financial statements to account for GAAP distortions, we can see that Sherwin-Williams’ acquisition of Valspar in 2017 has created tremendous value.

A deal that on paper makes perfect sense can easily be misconstrued by investors relying on as-reported metrics, proving once again the importance of the Uniform Accounting framework.

SUMMARY and The Sherwin-Williams Company Tearsheet

As the Uniform Accounting tearsheet for The Sherwin-Williams Company (SHW:USA) highlights, the Uniform P/E trades at 35.5x, which is above the global corporate average of 24.3x and its own historical P/E of 27.5x.

High P/Es require high EPS growth to sustain them. In the case of Sherwin-Williams, the company has recently shown a 22% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Sherwin-Williams’ Wall Street analyst-driven forecast is a 69% EPS shrinkage in 2021, followed by a 25% EPS growth in 2022.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Sherwin-Williams’ $326 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow by 12% annually over the next three years. What Wall Street analysts expect for Sherwin-Williams’ earnings growth is below what the current stock market valuation requires in 2021, but above the requirement in 2022.

Furthermore, the company’s earning power in 2020 is 5x above the long-run corporate average. Moreover, cash flows and cash on hand are over 1x its total obligations, signaling low credit and dividend risk.

Lastly, Sherwin-Williams’ Uniform earnings growth is below peer averages, while the company is trading above its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research